ACC vs Private Insurance: What's the Difference?

Imagine slipping on a wet floor at work and breaking your arm—that's when ACC steps in seamlessly, covering your treatment and lost wages. But what if a cancer diagnosis sidelines you for months? ACC...

Emma writes about health, wellbeing, and ACC topics for Lifetimes NZ. She translates complex health information into clear, actionable advice for New Zealand readers.

Imagine slipping on a wet floor at work and breaking your arm—that's when ACC steps in seamlessly, covering your treatment and lost wages. But what if a cancer diagnosis sidelines you for months? ACC won't help, leaving your family scrambling to pay the bills. This stark contrast is why understanding ACC vs private insurance is crucial for every Kiwi household in 2026.

We've got New Zealand's unique no-fault accident scheme to thank for protecting us from injury costs, but it leaves big gaps for illnesses that cause most long-term income loss. Private insurance steps in to fill those voids, offering income replacement, lump-sum payouts, and faster treatment. In this guide, we'll break down the differences, highlight real NZ scenarios, and show you how to build comprehensive cover that works alongside ACC.

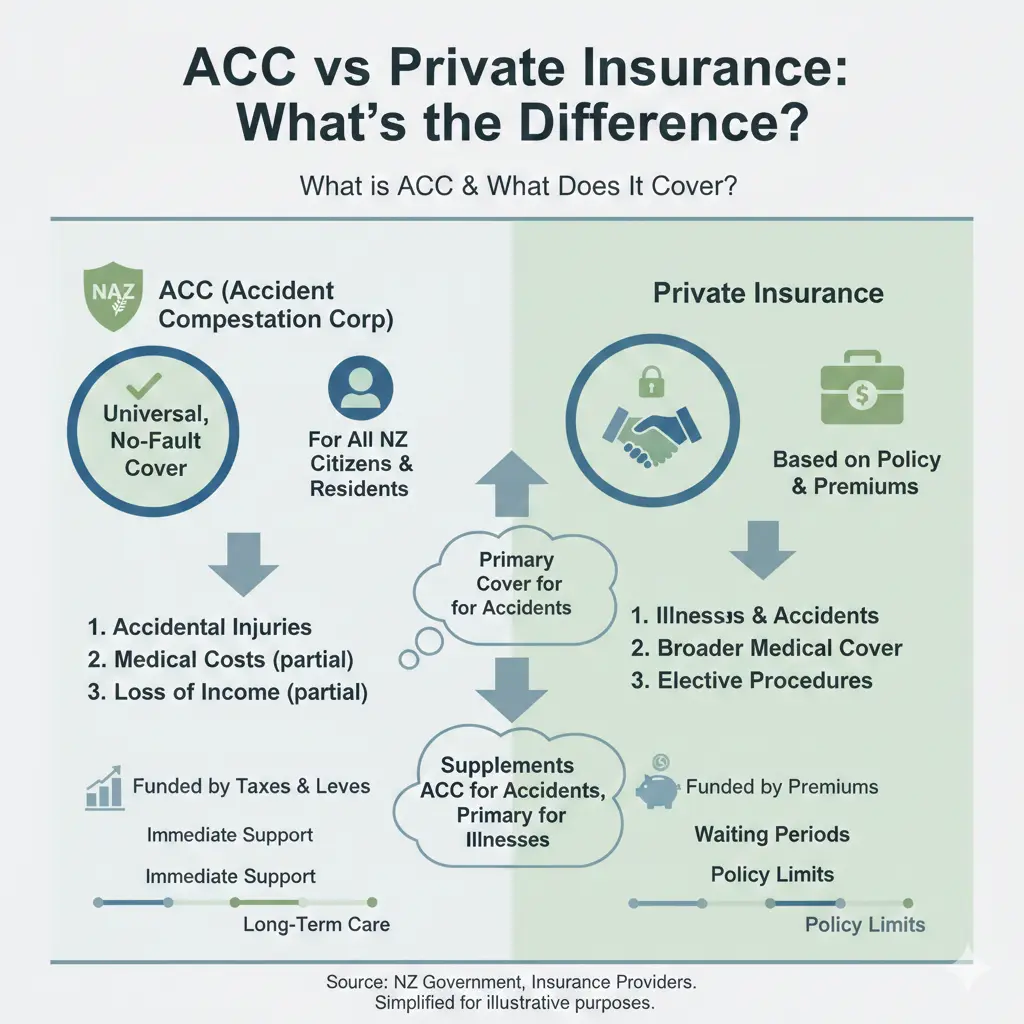

What is ACC and What Does It Cover?

ACC, or the Accident Compensation Corporation, is our government's no-fault scheme that covers personal injuries from accidents for everyone legally in New Zealand—whether you're employed, self-employed, or a visitor. Funded through levies on wages, employers, and vehicle registrations, it ensures no one sues for accident-related damages.

Key ACC Coverages

- Treatment costs: Doctor visits, surgery, rehab, and home help for accidents like car crashes, workplace slips, sports injuries, or falls.

- Income loss: Up to 80% of your pre-injury earnings (capped weekly amounts apply in 2026), but only if you're unable to work due to a covered injury.

- Other supports: Childcare, transport to appointments, and even funeral grants in fatal cases.

For example, if you're a tradie in Auckland who twists an ankle on-site, ACC covers physio and pays weekly compensation while you recover. Self-employed Kiwis can opt for CoverPlus Extra (CPX), letting you lock in a fixed income amount for claims—handy if your earnings fluctuate post-COVID. You'll pay an adjusted levy based on your chosen cover level.

ACC Limitations: What It Doesn't Cover

Here's the catch—ACC is injury-only. It excludes illnesses, which cause 80% of long-term workplace absences according to government data. No cover for:

- Cancer, strokes, heart attacks, or mental health issues like depression.

- Degenerative conditions, surgeries unrelated to accidents, or pre-existing issues contributing to an injury.

- Full replacement if you're fit for any work, not just your usual job.

Claims can be denied if they don't meet strict criteria, leading to appeals—thousands yearly. Plus, ACC faces a projected $26.3 billion funding gap by 2030, prompting tighter claims management in 2026. It's a fantastic safety net, but not comprehensive protection.

Private Insurance Options: Filling the Gaps

Private insurance complements ACC by covering illnesses and offering more generous benefits. Unlike ACC's levy-funded model, these are policies you buy from providers like nib, Southern Cross, AIA, or Partners Life, with premiums based on age, health, and occupation. Here's how they stack up in the ACC vs private insurance debate.

Income Protection Insurance

This replaces up to 75% of your income if illness or injury stops you working—extending far beyond ACC's scope. Benefits include:

- Monthly payouts for years or until retirement, covering mortgages and bills.

- Top-up feature: If ACC pays first (e.g., $1,500/week on a $100k salary), insurance adds the difference to reach your policy limit (e.g., $2,000/week).

- Own occupation definition: Pays if you can't do your job, not just any job.

A Hamilton teacher with depression? ACC says no, but income protection kicks in. Premiums start around $50/month for young professionals, but shop around for 2026 quotes.

Trauma (Critical Illness) Insurance

Pays a tax-free lump sum on diagnosis of serious conditions like cancer or heart attack—use it for private treatment, lost income, or family support. Unlike ACC, no proof of financial loss needed. Ideal for one-off crises.

Health Insurance

Gets you specialist access in weeks, not months, via private hospitals—bypassing public waits. Covers surgeries, diagnostics, and day-to-day care. ACC handles accident treatment, but health insurance speeds up illness recovery. Note: Premiums rose sharply in recent years due to claims and costs.

| Feature | ACC | Private Income Protection | Health Insurance |

|---|---|---|---|

| Covers Illness? | No | Yes | Yes |

| Income Replacement | 80% (injury only, capped) | Up to 75% (any cause) | No (treatment focus) |

| Waiting Period | Immediate for treatment | Typically 4-13 weeks | Immediate post-wait |

| Cost | Levies (mandatory) | Premiums ($30-200/month) | Premiums ($100+/month) |

ACC vs Private Insurance: Real-Life NZ Scenarios

Consider Sarah, a self-employed Wellington graphic designer. A bike accident? ACC covers 80% via CPX. But flu turns to pneumonia, forcing six months off—private income protection pays out, saving her home.

Or Mike, a Christchurch builder with heart disease. ACC denies the claim; trauma insurance delivers $100,000 for surgery and rehab. Savings alone vanish fast on treatments, mortgages, and kids' costs—insurance preserves your nest egg.

Self-employed? ACC's standard cover bases payouts on two years' earnings, but CPX fixes that for injuries only. Private policies offer flexibility without earnings history hassles.

Why Relying on Savings Falls Short

Many Kiwis self-insure with bank accounts, but major illness drains them quick: treatments cost thousands, work stops, bills pile up. ACC plugs accident holes, but private insurance is your buffer against the 80% illness risk. Don't wait—get personalised advice from a broker (free service) to match policies to your life.

Practical Tips for Choosing Cover in 2026

- Assess gaps: List illnesses vs accidents in your family history.

- Compare quotes: Use tools from Accuro, nib, or Partners Life for ACC vs private insurance top-ups.

- Review annually: Update for salary rises or life changes like kids.

- Talk to experts: Brokers simplify claims and exclusions—no extra cost.

- Bundle smart: Income protection + health often saves on premiums.

Protect Your Future: Next Steps Today

ACC excels at accidents, but private insurance guards against life's bigger threats like illness. Combine them for full security—your whānau deserves it. Start by reviewing your levies on acc.co.nz, get free 2026 quotes from multiple insurers, and chat with a licensed broker. Tailored cover brings peace of mind, so act now before the unexpected hits.

Frequently Asked Questions

Sources & References

-

1

ACC vs Income Protection Insurance - MoneyHub NZ — www.moneyhub.co.nz

-

2

ACC vs Insurance in New Zealand: What You Need to Know — simplylife.nz

-

3

ACC Versus Income Protection Insurance | Become Wealth Blog — www.become.nz

-

4

Health Insurance New Zealand - sharenz — sharenz.com

-

5

Understanding Health Insurance in New Zealand: A Friendly Guide — www.stewartgroup.co.nz

-

6

What ACC Doesn't Cover (and What Most Kiwis Get Wrong) — www.bufferinsurance.co.nz

-

7

Best health insurance NZ 2026: Quotes + comparison chart — www.policywise.co.nz

- 8

Useful Tools

Related Articles

ACC Explained: What’s Covered if You Have an Accident in NZ?

Picture this: you're out for a weekend tramp in the Coromandel, slip on a wet rock, and end up with a twisted ankle and a sprained wrist. The pain hits hard, but so does the relief of knowing New Zeal...

ACC for Self-Employed: Understanding Your Levies

If you're a self-employed Kiwi juggling gigs, trades, or your own business, one bill that can catch you off guard is your ACC levy invoice. Understanding how these levies work ensures you're covered f...