KiwiSaver Withdrawal Strategy: Should You Access Your Money Early?

Imagine staring down a stack of overdue bills or dreaming of that first home deposit, with your KiwiSaver balance looking like a lifeline. But is dipping into it early really the smart move, or does i...

The Lifetimes NZ editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes NZ readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Imagine staring down a stack of overdue bills or dreaming of that first home deposit, with your KiwiSaver balance looking like a lifeline. But is dipping into it early really the smart move, or does it risk your retirement dreams? For Kiwis facing tough choices, understanding KiwiSaver early withdrawal rules is crucial—let's break it down so you can decide wisely.

Understanding KiwiSaver Early Withdrawal Rules

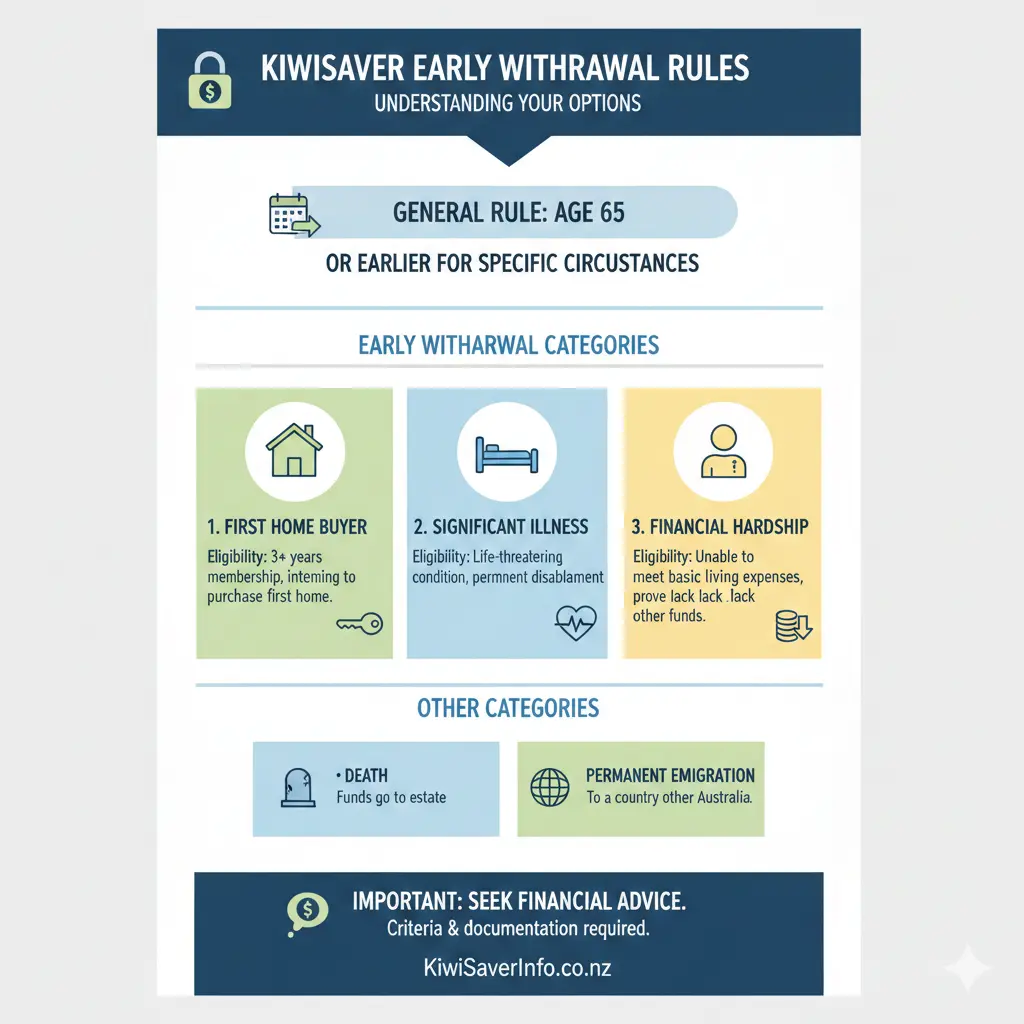

KiwiSaver is designed for our retirement, locking away savings until age 65 when you qualify for New Zealand Superannuation. But life happens, and the law allows early access in specific cases. These aren't loopholes—they're tightly regulated by Inland Revenue (IRD) and the Financial Markets Authority (FMA) to protect your long-term nest egg.

In 2026, the rules remain strict: you can't withdraw just because markets dip or cash is tight. Your provider and an independent supervisor must approve applications, ensuring only genuine needs qualify. Withdrawals are tax-free, but they come at a cost to compound growth.

Key Eligibility Criteria for Early Access

- Minimum membership: Most withdrawals require at least three years in KiwiSaver, except serious illness or hardship cases.

- Minimum balance: Leave at least $1,000 in your account (plus any Australian super transfers).

- Exclusions: No government contributions or Member Tax Credits (formerly kick-start, ended 2015).

First Home Withdrawal: The Most Common Early Access Option

Buying your first home? KiwiSaver can boost your deposit if you've been a member for three years—the famous '3-year rule'. This lets you withdraw your contributions, employer matches, returns, and Member Tax Credits (minus $1,000 minimum).

Who Qualifies as a First Home Buyer?

You must not own a home anywhere in the world, and the property must be in New Zealand. Previous owners might qualify if Housing New Zealand (Kāinga Ora) approves—no more than 20% of the regional house price cap in realisable assets. Get a first home eligibility letter from your provider for loan pre-approvals.

Step-by-Step Process

- Get an estimate: Log into your provider's portal or contact them for a withdrawal amount letter.

- Secure your offer: Once you have a conditional sale and purchase agreement, apply formally—witnessed by a JP or solicitor.

- Timing is key: Apply weeks before settlement; providers like Kiwibank warn it can take time. Miss it, and you can't withdraw post-purchase.

- Combine with schemes: Pair with Kāinga Ora's First Home Grant or Welcome Home Loans for extra help.

Example: Sarah, a 28-year-old from Auckland, joined KiwiSaver at 25. After three years, her $50,000 balance (minus $1,000) covers a crucial deposit chunk amid rising house prices.

Financial Hardship Withdrawals: When Life Gets Tough

Can't cover essentials like rent, power, or unexpected repairs? Significant financial hardship withdrawals are possible without the three-year wait, but prove it with evidence like debt statements or benefit letters. Your provider assesses, and approval isn't guaranteed.

Common Hardship Scenarios

- Unable to pay mortgage/rent after job loss.

- Utility bills threatening disconnection.

- Unexpected costs like car repairs for work travel.

- Serious illness costs not covered elsewhere.

You can access personal and employer contributions plus returns—not government ones. Consider suspending contributions first: it pauses yours, employer matches, and government top-ups without raiding the pot.

"Financial hardship withdrawals are allowed only in serious circumstances... Both options can significantly affect long-term retirement savings." – Simplicity KiwiSaver

Serious Illness and Life-Shortening Conditions

If facing a terminal diagnosis or life-shortening congenital condition, withdraw fully regardless of age. Since 2021 amendments, automatic approval applies to conditions like Down syndrome, cerebral palsy, Huntington’s disease, or fetal alcohol spectrum disorder—with medical certification. Others need evidence life expectancy is under 65.

This ensures you enjoy retirement-quality living sooner. Contact IRD or your provider for forms.

Moving Overseas: KiwiSaver Exit Strategy

Heading offshore permanently (not Australia)? After one year abroad, withdraw most funds: contributions, employer matches, returns, and old kick-starts—but Member Tax Credits return to the government. Notify your provider with proof of residency.

Auckland expat Mike withdrew $80,000 after moving to the UK, leaving his account open for future top-ups.

Pros and Cons of KiwiSaver Early Withdrawal

| Pros | Cons |

|---|---|

| Immediate cash for home, hardship, or health. | Loses compound growth—$10k withdrawn at 30 could be $100k+ by 65. |

| Tax-free access to eligible portions. | Misses future employer/government contributions on withdrawn amount. |

| Keeps account active with $1,000 minimum. | Opportunity cost: better alternatives like budgeting or loans often exist. |

Run a compound calculator on IRD's KiwiSaver site to see the impact.

Alternatives to Early Withdrawal

Before applying, explore these:

- Budget tweaks: Use MoneySmart tools from Commission for Financial Capability.

- Emergency funds: Build 3-6 months' expenses separately.

- Loans: Low-interest community finance or family.

- Suspension: Pause contributions temporarily.

- Provider advice: Free guidance from your scheme.

Plan Smart: Next Steps for Your KiwiSaver

Early withdrawal can save the day but often at retirement's expense. Chat with your provider, use IRD's online tools, or see a financial adviser via FMA's register. Track your balance on myIR, maximise contributions now, and diversify emergencies. Your future self will thank you—kiwi strong!

Frequently Asked Questions

Useful Tools

Related Articles

KiwiSaver 2026: Which Fund is Actually Winning the Performance Race?

If you're tracking your KiwiSaver fund performance in 2026, you might be surprised to learn that the winners aren't always the biggest banks – and the rankings keep shifting. The latest investment sur...

PIR Rates Explained: Are You Paying Too Much Tax on Your KiwiSaver?

Ever checked your KiwiSaver statement and wondered why the tax on your returns seems off? You're not alone—many Kiwis are paying too much (or too little) on their KiwiSaver earnings because of an inco...

KiwiSaver vs Other Investments: Where Should Your Money Go?

Ever wondered if your hard-earned cash is working as hard as it could in KiwiSaver, or if there's a better spot for it elsewhere? With house prices cooling and shares hitting new highs, many Kiwis are...

Best KiwiSaver Providers in NZ 2025: Complete Comparison

Choosing the right KiwiSaver provider can supercharge your retirement savings or first home deposit, especially with government contributions and employer matches adding free money to your account. In...