PIR Rates Explained: Are You Paying Too Much Tax on Your KiwiSaver?

Ever checked your KiwiSaver statement and wondered why the tax on your returns seems off? You're not alone—many Kiwis are paying too much (or too little) on their KiwiSaver earnings because of an inco...

The Lifetimes NZ editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes NZ readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Ever checked your KiwiSaver statement and wondered why the tax on your returns seems off? You're not alone—many Kiwis are paying too much (or too little) on their KiwiSaver earnings because of an incorrect PIR rate, potentially costing you hundreds in overpaid tax each year.

With KiwiSaver contribution rates rising to 3.5% from 1 April 2026, now's the perfect time to get your PIR sorted. This guide breaks down PIR rates explained simply, shows you how to check if you're overpaying tax on your KiwiSaver, and walks you through actionable steps to fix it—all tailored for New Zealanders in 2026.

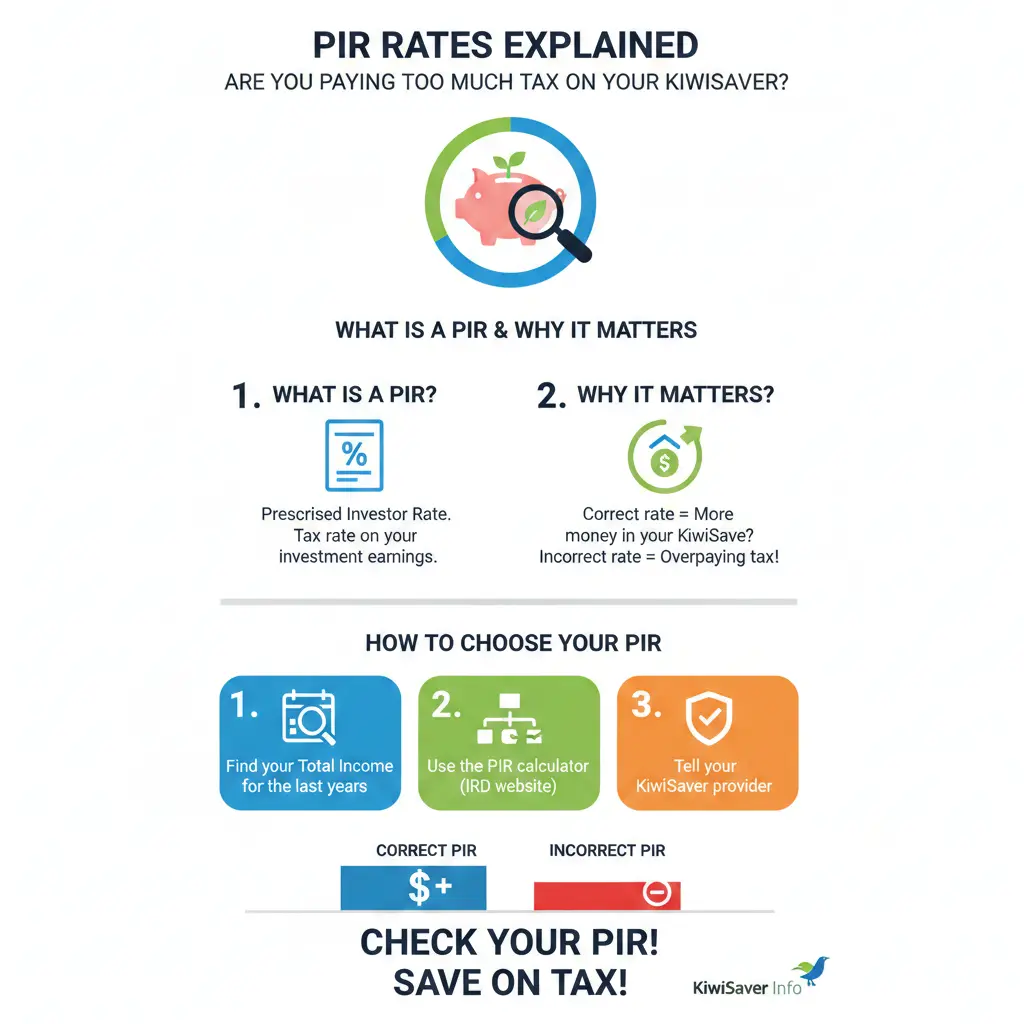

What is a PIR and Why Does it Matter for Your KiwiSaver?

PIE stands for Portfolio Investment Entity, and KiwiSaver funds are typically PIEs. Your Prescribed Investor Rate (PIR) is the tax rate your KiwiSaver provider uses to tax the earnings (like interest, dividends, and growth) inside your fund. It's not your regular income tax rate—it's a special rate designed to simplify taxing investments.

Getting your PIR wrong means either overpaying tax (which you might get refunded later) or underpaying (which IRD will chase you for). From the 2021 tax year, IRD automatically checks and adjusts your PIR based on their records, refunding overpayments or billing shortfalls. In 2026, with income thresholds updated, it's easier than ever to confirm your rate—but many still don't.

How PIR Tax Works in KiwiSaver

- Your provider calculates taxable income from your share of the fund's earnings.

- They withhold tax at your PIR and pay it to IRD on your behalf.

- If your PIR is too high, IRD refunds the difference directly to your KiwiSaver.

- If too low, you'll owe IRD the shortfall via your tax return.

Pro tip: Always provide your correct IRD number and PIR to your provider—without it, you're defaulted to 28%.

2026 PIR Rates Explained: Which One Applies to You?

PIR rates are 10.5%, 17.5%, or 28% for most Kiwis (0% for some non-profits or trusts). They're based on your taxable income in the last two income years (1 April to 31 March). Use the year that gives your lowest (best) rate.

From 1 April 2025, updated thresholds apply for the 2026 tax year:

| Taxable Income (Last Two Years) | Total Taxable + PIE Income (Last Two Years) | Your PIR |

|---|---|---|

| $15,600 or less | $53,500 or less | 10.5% |

| More than $15,600 but $53,500 or less | More than $53,500 but $78,100 or less | 17.5% |

| $53,501 and over | $78,101 and over | 28% |

Example: If you earned $45,000 in 2024/25 and $50,000 in 2025/26, your PIR stays at 17.5% for 2026/27 because it's based on the lower year. Overseas tax residents or high earners over $78,101 in both years get 28%.

Special Cases for PIR in 2026

- Children: Almost always 10.5%—they rarely earn over $15,600.

- Trustees: Can choose 28%, 17.5%, 10.5% (testamentary), or 0%, with reporting rules.

- No IRD number pre-2018: Default 28% on earnings.

Check your rate at IRD's PIR tool.

Are You Paying Too Much Tax on Your KiwiSaver? Signs and Examples

Yes, if your PIR doesn't match your income history. IRD will refund overpayments, but why wait? Here's how to spot it.

Real Kiwi Examples

- Low earner (e.g., apprentice, $40,000/year): Qualifies for 10.5% or 17.5%. If set at 28%, you're overpaying—could be $100s refunded annually on 5-7% fund returns.

- Mid-income (e.g., teacher, $70,000/year): Likely 17.5%. 28% PIR means overtaxed by ~10% on earnings.

- High earner (e.g., exec, $90,000/year both years): 28% is correct—no issue.

On a $100,000 KiwiSaver balance growing at 6% ($6,000 earnings), the tax difference:

- 10.5% PIR: $630 tax

- 17.5% PIR: $1,050 tax

- 28% PIR: $1,680 tax

2026 KiwiSaver Changes Impacting Your PIR

Contribution rates jump to 3.5% minimum from 1 April 2026 (up from 3%), matching employer contributions. On $70,000 salary, that's $2,450/year from you (vs $2,100), plus matching from employer—total ~$700 extra annually.

Govt contributions dropped to 25c/$1 (max $260.72/year) from 1 July 2025—still worth $20/week minimum to max it. Higher contributions mean more earnings, amplifying PIR tax impacts.

How to Check and Update Your PIR Rate

It's quick and free. Follow these steps:

- Review income: Grab your last two IR3 returns or myIR income summary.

- Use IRD tool: Visit ird.govt.nz/pir—enter details for instant result.

- Notify provider: Log into your KiwiSaver dashboard (e.g., Westpac, SuperLife) and update PIR + IRD number.

- Monitor: IRD auto-adjusts from 1 April 2020 if wrong, but confirm manually.

Takes 5 minutes—do it before 30 June 2026 to align with tax year-end.

Practical Tips to Minimise KiwiSaver Tax in 2026

- Opt for lower PIR if eligible—saves upfront and compounds growth.

- Contribute extra to hit govt top-up ($1,042.86/year min).

- If rates rise hurts cashflow, apply for temporary 3% reduction from 1 Feb 2026.

- Review annually—income changes (raise, job loss) affect PIR.

- High earners: Consider 28% early to avoid shortfalls.

Frequently Asked Questions

Related Articles

KiwiSaver 2026: Which Fund is Actually Winning the Performance Race?

If you're tracking your KiwiSaver fund performance in 2026, you might be surprised to learn that the winners aren't always the biggest banks – and the rankings keep shifting. The latest investment sur...

KiwiSaver vs Other Investments: Where Should Your Money Go?

Ever wondered if your hard-earned cash is working as hard as it could in KiwiSaver, or if there's a better spot for it elsewhere? With house prices cooling and shares hitting new highs, many Kiwis are...

Best KiwiSaver Providers in NZ 2025: Complete Comparison

Choosing the right KiwiSaver provider can supercharge your retirement savings or first home deposit, especially with government contributions and employer matches adding free money to your account. In...

How to Choose the Right KiwiSaver Fund for Your Age

Choosing the right KiwiSaver fund is one of the most important financial decisions you'll make for your retirement. Your age, time horizon, and risk tolerance should guide your choice, but with 370 fu...