KiwiSaver 2026: Which Fund is Actually Winning the Performance Race?

If you're tracking your KiwiSaver fund performance in 2026, you might be surprised to learn that the winners aren't always the biggest banks – and the rankings keep shifting. The latest investment sur...

The Lifetimes NZ editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes NZ readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

If you're tracking your KiwiSaver fund performance in 2026, you might be surprised to learn that the winners aren't always the biggest banks – and the rankings keep shifting. The latest investment surveys show some compelling shifts at the top, with smaller, focused providers punching well above their weight and delivering returns that rival (or beat) the major players. Let's break down which funds are actually winning the performance race and what that means for your retirement savings.

The 2026 KiwiSaver Performance Landscape

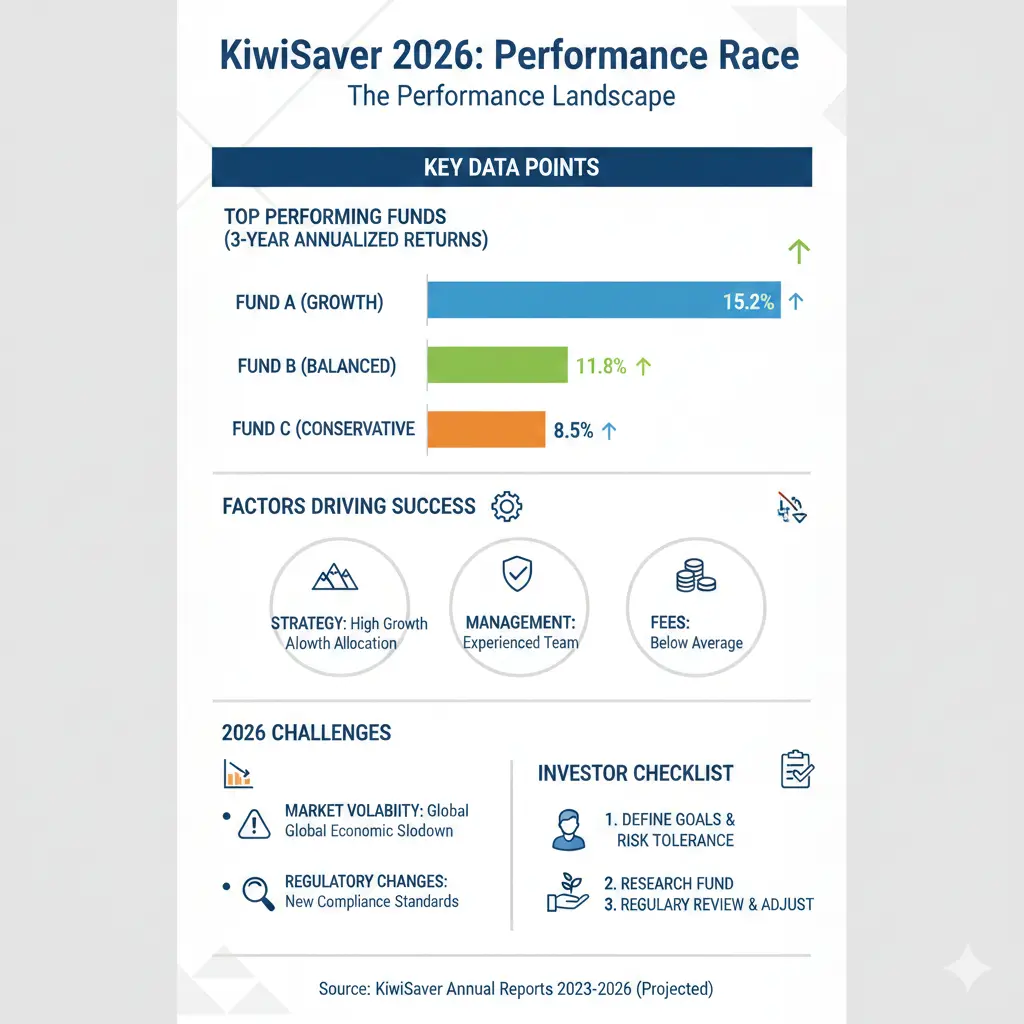

The most recent data from the Melville Jessup Weaver (MJW) Investment Survey (December 2025) reveals a competitive market where size doesn't guarantee success. The survey assessed New Zealand's 17 largest KiwiSaver schemes by assets under management, and the results paint an interesting picture of who's delivering the best returns across different risk categories.

Over the past three years, KiwiSaver investors have enjoyed particularly healthy returns. The median growth fund returned 13.3 percent per annum, balanced funds returned 10.9 percent, and conservative funds returned 7.4 percent – all after costs and before tax. But these are medians; the top performers are delivering significantly higher.

Growth Funds: The High-Risk Winners

If you're a younger Kiwi with a longer investment timeline, growth funds are where the action is. Simplicity leads the growth category over three years with returns of 15.7 percent annually, making it the standout performer for aggressive investors. Over one year, Westpac took the top spot with 12.8 percent returns.

For the 10-year perspective – which many financial advisers consider the gold standard for long-term investing – Milford leads growth funds with 10.2 percent annual returns. This consistency over a decade suggests that Milford's investment approach has weathered multiple market cycles effectively.

It's worth noting that MAS, a smaller provider managing around $3.3 billion in funds under management, ranked in the top five for growth funds over the 10-year period. This demonstrates that you don't need a major bank's scale to deliver competitive returns.

Balanced Funds: The Goldilocks Zone

For those seeking a middle ground between growth and security, balanced funds offer an appealing mix. The performance leaders vary depending on the timeframe you're looking at:

- Over three years: ASB leads with 12.6 percent annual returns

- Over one year: Westpac tops the list with 11 percent

- Over 10 years: Milford delivers 8.1 percent annually

If you're mid-career and want steady growth without keeping you awake at night, balanced funds from these providers offer proven track records.

Moderate Funds: The Steady Performers

Moderate funds sit between balanced and conservative, appealing to those approaching retirement or with a moderate risk tolerance. The current leaders are:

- Over three years: AMP delivers 10.9 percent annually

- Over one year: AMP leads again with 9.5 percent

- Over 10 years: AMP comes out on top with 5.8 percent

AMP's consistency across multiple timeframes makes it a reliable choice if you're looking for moderate risk exposure.

Conservative Funds: Capital Preservation with Growth

If you're close to retirement or simply prefer to sleep well at night, conservative funds prioritise capital preservation while still aiming for growth. The performance rankings show:

- Over three years: ASB leads with 8 percent annual returns

- Over one year: ASB again tops the list with 7.6 percent

- Over 10 years: Milford delivers 5.1 percent annually

These returns are solid for a conservative fund, demonstrating that you don't have to sacrifice growth entirely to reduce volatility.

The MAS Story: Proving Size Isn't Everything

One of the most encouraging stories in the 2026 KiwiSaver market is MAS's consistent top-five performance across all fund categories – growth, balanced, moderate, and conservative – over the past three years. This is particularly impressive given that MAS manages around $3.3 billion compared to major banks managing up to ten times that amount.

"These results confirm that scale alone doesn't determine outcomes," says Jo McCauley, Chief Executive of MAS. "The MJW rankings show that a focused, disciplined investment approach can deliver consistently strong performance – even when competing with much larger providers."

This is valuable context for Kiwis who might assume that choosing a major bank's KiwiSaver scheme is the safest option. The data suggests that a focused investment strategy can outperform larger, more bureaucratic competitors.

What These Rankings Actually Mean for You

Before you rush to switch your KiwiSaver to whichever fund topped last quarter's rankings, it's important to understand what these numbers represent:

Past Performance Isn't Guaranteed

Every fund disclosure includes this disclaimer for a reason: past performance doesn't guarantee future results. A fund that led the rankings last year might underperform next year depending on market conditions, management changes, or strategic shifts.

Your Time Horizon Matters More Than Rankings

If you're 25 years old, a growth fund's 15.7 percent three-year return is more relevant than its 10-year performance. If you're 55, the opposite is true. Choose your fund based on your age, risk tolerance, and when you'll need the money – not just on who won last quarter.

Fees Make a Difference

The returns quoted in surveys are after fees, so you're already seeing the real impact. However, different providers charge different fees, and over 40+ years of KiwiSaver contributions, even a 0.5 percent difference in fees can add up to tens of thousands of dollars.

Consider Your Full Financial Picture

KiwiSaver is just one part of your retirement savings. Your employer contribution, your own contributions, and the government's annual contribution of up to $521.43 (depending on your contributions) all matter. Some providers offer better customer service, easier interfaces, or additional features that might be worth more to you than chasing the top performer.

How to Choose Your KiwiSaver Fund in 2026

Rather than simply picking the fund with the best recent returns, consider this framework:

- Determine your risk profile: How many years until you retire? How comfortable are you with market volatility? Use your provider's risk assessment tools or speak with a financial adviser.

- Check the long-term track record: Look at 10-year performance if available, not just quarterly or annual returns. Consistency matters more than one brilliant year.

- Compare fees: Even small differences compound over decades. Check your provider's fee schedule and compare it with alternatives.

- Evaluate service quality: Can you easily access your account online? Is customer service responsive? Will you be able to make changes when you need to?

- Consider switching costs: If you're already in a KiwiSaver scheme, check whether switching involves any penalties or tax implications.

The Bottom Line

The 2026 KiwiSaver performance data shows a market where excellent returns are available across multiple providers – you don't have to stick with a major bank to get competitive performance. Simplicity, Westpac, ASB, AMP, and Milford are all delivering strong results, alongside smaller players like MAS that prove focused management beats scale.

Rather than obsessing over who won last quarter, focus on choosing a fund that matches your risk profile, offers reasonable fees, and provides the service level you need. Then let compound growth do the heavy lifting over the next 20, 30, or 40 years. That's where the real wealth-building happens in KiwiSaver.

Ready to review your KiwiSaver setup? Check your current fund's performance on your provider's website, compare it with the leaders in your risk category, and consider whether a change makes sense for your situation. If you're unsure, many KiwiSaver providers offer free financial guidance – it's worth using it.

Frequently Asked Questions

Sources & References

- 1

- 2

Related Articles

PIR Rates Explained: Are You Paying Too Much Tax on Your KiwiSaver?

Ever checked your KiwiSaver statement and wondered why the tax on your returns seems off? You're not alone—many Kiwis are paying too much (or too little) on their KiwiSaver earnings because of an inco...

KiwiSaver vs Other Investments: Where Should Your Money Go?

Ever wondered if your hard-earned cash is working as hard as it could in KiwiSaver, or if there's a better spot for it elsewhere? With house prices cooling and shares hitting new highs, many Kiwis are...

Best KiwiSaver Providers in NZ 2025: Complete Comparison

Choosing the right KiwiSaver provider can supercharge your retirement savings or first home deposit, especially with government contributions and employer matches adding free money to your account. In...

How to Choose the Right KiwiSaver Fund for Your Age

Choosing the right KiwiSaver fund is one of the most important financial decisions you'll make for your retirement. Your age, time horizon, and risk tolerance should guide your choice, but with 370 fu...