Life Insurance for Families: How Much Coverage Do You Need?

As Kiwi parents, we all want to ensure our families are protected if the worst happens. Imagine your partner facing not just grief, but the stress of a mortgage, school fees, and daily bills without y...

The Lifetimes NZ editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes NZ readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

As Kiwi parents, we all want to ensure our families are protected if the worst happens. Imagine your partner facing not just grief, but the stress of a mortgage, school fees, and daily bills without your income—life insurance can provide that essential safety net, tailored to New Zealand families.

Why Life Insurance Matters for NZ Families

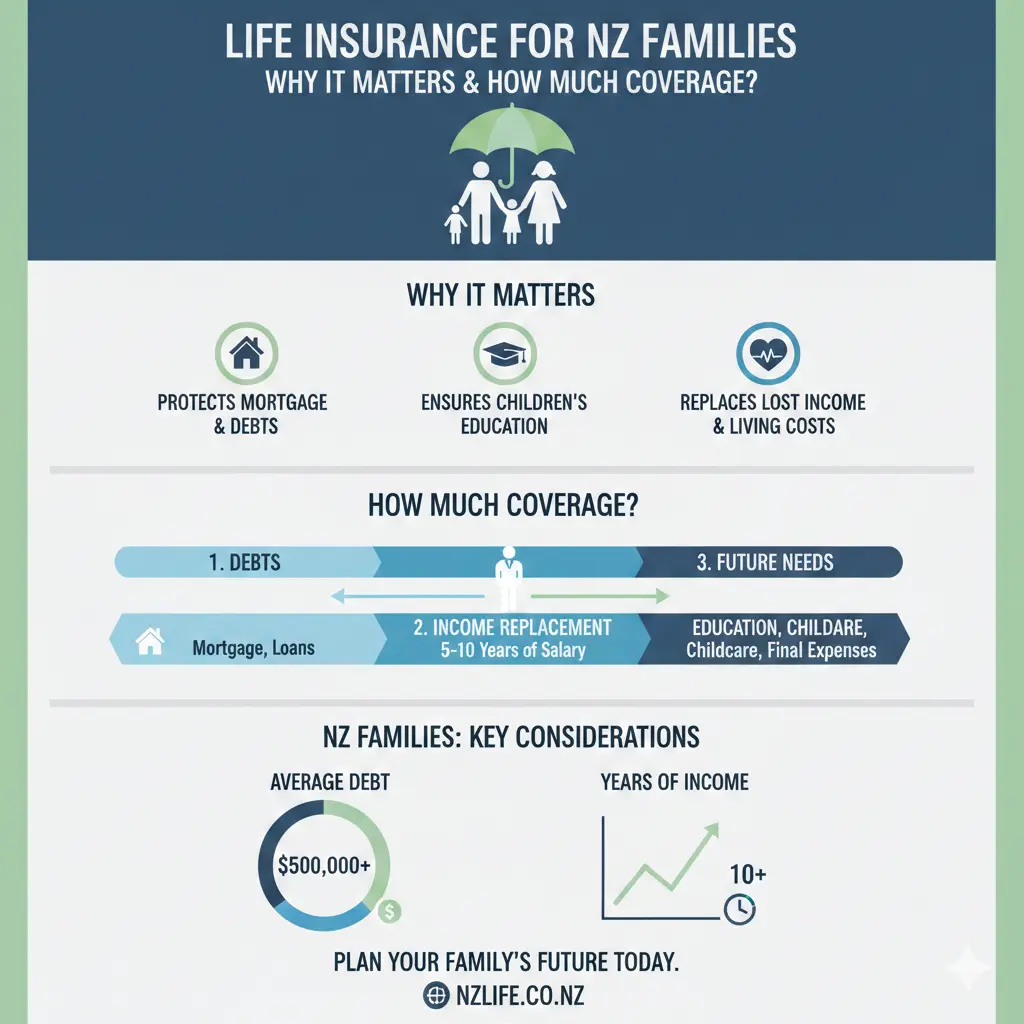

With rising living costs in 2026, many New Zealand households rely on dual incomes or a single breadwinner to cover everything from Auckland mortgages to rural school runs. Life insurance pays a tax-free lump sum (or monthly payments in some cases) to your family if you pass away or are diagnosed with a terminal illness, helping them maintain their lifestyle without forced changes like selling the family home. It's not just for the wealthy—over 70% of Kiwi families with kids under 18 have some form of cover, but many are underinsured.

For families, this means covering immediate needs like funerals (averaging $10,000 in NZ) and longer-term ones like tertiary education. Unlike KiwiSaver, which is for retirement, life insurance steps in during tragedy to replace lost income.

Common Family Scenarios in New Zealand

- Families with young kids: One parent's death could mean childcare gaps or reduced work hours for the survivor.

- Mortgage-heavy households: The average NZ home loan is around $400,000—enough to wipe out stability without cover.

- Single-income setups: Common in regional areas or with stay-at-home parents, where 10x the earner's salary is a starting point.

- Blended families: Ensuring step-kids' futures are protected too.

How Much Coverage Do New Zealand Families Really Need?

There's no one-size-fits-all, but experts recommend a needs-based calculation over vague rules. Start with 10 times your annual pre-tax income as a baseline—for a $80,000 earner, that's $800,000. Adjust based on your situation using this step-by-step NZ-focused guide.

Step-by-Step Calculator for Kiwi Families

- Add up debts: Full mortgage balance, car loans, credit cards. Aim to clear them outright.

- Factor in living costs: 5–10 years of expenses (rent/mortgage, groceries, utilities). For a family of four, that's often $500,000+.

- Include education: School fees, uniforms, or uni costs—$20,000–$50,000 per child.

- Funeral and extras: $10,000–$15,000 for a standard NZ funeral, plus estate fees.

- Future-proof: Add for dependents like elderly parents or business owners.

- Subtract assets: Savings, KiwiSaver death benefits, or existing cover.

Example for an Auckland family: Earning $120,000 combined, $500,000 mortgage, two kids under 10, $50,000 savings. Total need: $500k (debts) + $400k (5 years living) + $100k (education/funeral) - $50k (assets) = $950,000. Opt for policies up to $1 million if aged 18–54.

| Age Group | Max Cover (e.g., Platinum Life) |

|---|---|

| 18–54 | $1,000,000 |

| 55–60 | $750,000 |

| 61–65 | $500,000 |

Many insurers like AIA offer unlimited cover for comprehensive plans, while starters cap at $300,000. Review every 2–5 years or after life events like births or home buys—your mortgage shrinks, so can your premium.

Types of Life Insurance for NZ Families

New Zealand offers flexible options. Choose based on whether you want a lump sum or income stream.

Lump Sum Life Insurance

Pays once upon death or terminal illness (under 12 months to live). Ideal for clearing debts. Providers like Momentum's Platinum offer $50k–$1m, no medicals for most under 65, with 3% annual increases for inflation. Chubb and AIA provide similar, often with funeral advances.

Family Protection (Income-Based)

Monthly payouts (e.g., $5,000/month for 10 years) for living costs. Can be cheaper than lump sum for high needs, but pick one over the other to avoid overlap. KiwiCover offers child extensions up to $2,000 funeral cover for under-10s.

Extras to Consider

- Terminal illness benefit: Early payout.

- Children's cover: Accidental death or illness.

- No pandemic exclusions: COVID claims covered if eligible.

Costs and Getting Covered in 2026

Premiums start low: $20–$50/month for $250k cover (30-year-old non-smoker). Pay fortnightly to match NZ wages—no extra fees. Factors raising costs: Age over 50, smoking, pre-existing conditions (disclose fully to avoid claim denials).

Shop via advisers authorised by the Financial Markets Authority (FMA)—they access all providers. No medicals for many policies if healthy.

Practical Tips for NZ Families

- Use online calculators from MoneyHub or insurers.

- Joint policies for couples save money (max two lives).

- Guaranteed acceptance if under 65, resident.

- Review post-2026 budget changes or rate hikes.

- Speak to an independent adviser, not just bank reps.

Next Steps to Protect Your Family Today

Grab a coffee, list your debts and expenses, then get free quotes from three providers. Chat with an FMA-registered adviser via fma.govt.nz. Don't delay—peace of mind for your whānau is priceless, and locking in cover now beats waiting. Your family's future thanks you.

Frequently Asked Questions

Sources & References

-

1

Platinum Life Insurance Cover for NZ Residents — www.momentumlife.co.nz

-

2

Best Life Insurance Companies in NZ (2026 Guide) — www.nzinsurances.co.nz

-

3

Compare Life Insurance NZ 2025: Best Policies, Quotes & ... — www.moneyhub.co.nz

-

4

Life Insurance - Compare and get a quote — www.aia.co.nz

-

5

How much Life Insurance do I need? — www.chubb.com

-

6

Life Insurance and what you need to know — healthcareplus.org.nz

-

7

Life Insurance | Chubb Life New Zealand — www.chubb.com

-

8

A financial safety net for single income families — www.fidelitylife.co.nz

-

9

Family Protection Insurance | Compare Quotes Online — www.kiwicover.co.nz

-

10

How Much Life Insurance Do I Really Need in New Zealand? — www.policywise.co.nz