ACC and Pre-Existing Conditions: What's Actually Covered

If you've got a pre-existing health condition, you might wonder whether ACC—New Zealand's no-fault injury insurance scheme—will cover it. The short answer is: ACC doesn't cover pre-existing conditions...

Sarah covers personal finance, tax, and KiwiSaver topics for Lifetimes NZ. She focuses on making money management straightforward and practical for everyday Kiwis.

If you've got a pre-existing health condition, you might wonder whether ACC—New Zealand's no-fault injury insurance scheme—will cover it. The short answer is: ACC doesn't cover pre-existing conditions, because ACC only covers personal injuries from accidents, not illnesses or medical conditions you already have. Understanding this distinction is crucial for protecting your health and finances, especially if you're managing an ongoing condition.

Many Kiwis assume ACC is a catch-all safety net, but it's actually quite specific in what it covers. If you rely on ACC to help with a pre-existing condition like diabetes, asthma, or heart disease, you'll be disappointed. That's where private health insurance comes in—and knowing the difference between the two can save you thousands of dollars in unexpected medical costs.

What ACC Actually Covers

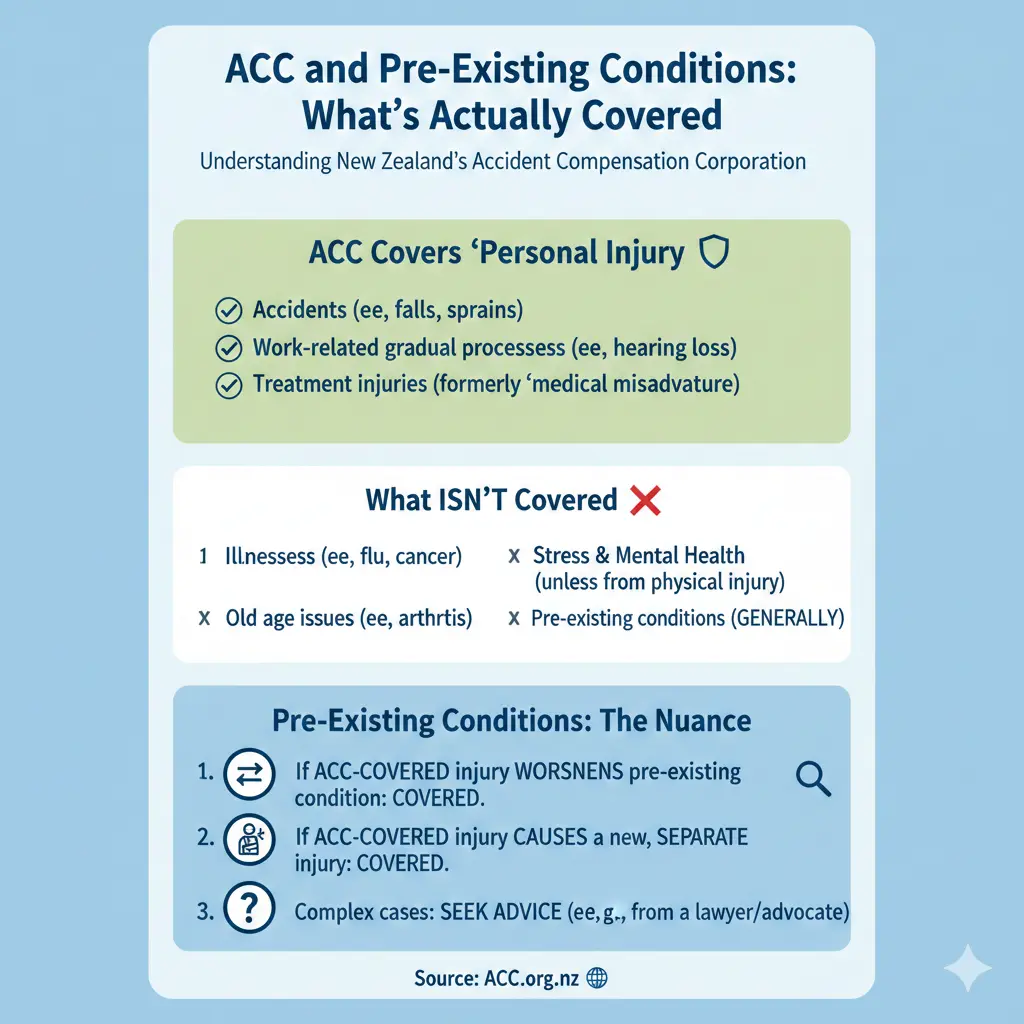

ACC (Accident Compensation Corporation) is a unique part of New Zealand's social safety net. It's a no-fault system, meaning you're covered for injuries caused by accidents regardless of who's responsible. This is genuinely valuable protection, but it's strictly limited to accidents and personal injuries, not illness.

Here's what ACC covers:

- Medical treatment costs: Hospital stays, surgery, GP visits, physiotherapy, and specialist treatment for accident-related injuries

- Rehabilitation: Ongoing support to help you recover and return to normal activities or work

- Income compensation: Weekly payments (up to 80% of your earnings) if you can't work because of accident injuries

- Lump sum payments: For permanent injuries causing ongoing impairment

The key word here is "accident." Whether you're a resident or visitor, you're covered from day one in New Zealand if you're injured in an accident—even if you caused it yourself. Slip on a wet floor at the supermarket? That's covered. Get injured in a car crash? That's covered. Injure yourself while hiking in the Marlborough Sounds? Covered.

What ACC Doesn't Cover (And This Is Important)

ACC specifically does not cover:

- Medical conditions and diseases

- Illness

- Mental health issues (unless they're directly caused by an accident)

- Gradual process injuries (except specific work-related conditions)

- Congenital conditions

- Pre-existing conditions

This is a critical gap for many Kiwis. If you've been diagnosed with type 2 diabetes, high blood pressure, or asthma before your accident, ACC won't cover treatment for those conditions—even if the accident makes them worse. Mental health claims are particularly strict; if ACC believes your mental injury is caused by stress, pre-existing conditions, or other non-covered factors, your claim is likely to be declined.

Why the Distinction Matters

The difference between "accident" and "illness" might seem obvious, but it's where many Kiwis get caught out. Imagine you have arthritis and slip on ice, injuring your knee. ACC will cover the acute injury from the fall, but not the underlying arthritis condition. Or consider this scenario: you have a pre-existing heart condition and have a heart attack while at work. ACC won't cover it because the heart attack is a medical event, not an accident-caused injury.

This is why income protection insurance exists—to cover your inability to work due to illness, which ACC doesn't address.

Pre-Existing Conditions and Private Health Insurance

Since ACC won't help with pre-existing conditions, private health insurance becomes essential if you want coverage for ongoing medical issues. However, private insurers in New Zealand also typically exclude or restrict coverage for pre-existing conditions.

How Private Insurers Handle Pre-Existing Conditions

When you apply for private health insurance, insurers will assess your application based on your medical history. Pre-existing conditions may be handled in several ways:

- Permanent exclusion: The condition is never covered under your policy

- Waiting periods or stand-down periods: The condition is covered only after you've held the policy for a set period (typically three years) with no further symptoms or treatment

- Group scheme coverage: If you're covered through your workplace, some group schemes can offer coverage for pre-existing conditions that wouldn't be available to individuals

- Special promotions: From time to time, health insurers run promotions that include coverage for pre-existing conditions after a waiting period

When an insurer excludes a condition, it means any healthcare costs arising from that condition won't be reimbursed by your insurer. Your policy document will clearly state which conditions are excluded.

Group Schemes: A Better Option?

If your employer offers health insurance through a group scheme, you may have better luck getting coverage for pre-existing conditions. Group schemes often have more flexible underwriting than individual policies. If you're self-employed or your employer doesn't offer health insurance, you'll need to explore individual policies or speak with an insurance broker who can help you find options that suit your circumstances.

How ACC and Private Insurance Work Together

In New Zealand, ACC and private health insurance serve different purposes and work alongside each other.

ACC helps with accidents (injury). If you're injured in an accident, ACC covers your treatment and rehabilitation costs.

Private medical insurance helps with eligible private care, especially around illness, diagnostics, and elective treatment pathways. This is where coverage for pre-existing conditions matters most.

Here's a practical example: You have diabetes (pre-existing condition) and need specialist care. Your GP refers you to an endocrinologist, but there's a six-month wait in the public system. If you have private health insurance that covers your diabetes, you could be covered for a specialist consultation and potentially arrange faster treatment through a private provider. Without that insurance, you'd either wait or pay out of pocket.

Extra Drug Cover and Non-PHARMAC Medications

One additional consideration: some private health insurance policies offer "extra drug cover" or "non-PHARMAC cover," which means coverage for medications not funded by PHARMAC (Pharmaceutical Management Agency). This can be particularly relevant if you have a pre-existing condition requiring newer or less common medications. However, this cover isn't automatic and always comes with conditions and limits.

Practical Steps for Kiwis with Pre-Existing Conditions

If you're managing a pre-existing condition, here's what you should do:

- Know your ACC coverage: Understand that ACC covers accidents only, not your underlying condition. If you're injured in an accident, file a claim promptly.

- Review your medical records: Before applying for private health insurance, check your medical records with your GP. There could be notes or conditions you're unaware of, and knowing your full history will help you complete insurance applications accurately.

- Be honest on applications: Disclose all pre-existing conditions when applying for health insurance. Non-disclosure can delay your application or affect your ability to make claims later.

- Compare policies carefully: Look at waiting periods, exclusions, and benefit limits. Some policies offer better coverage for pre-existing conditions than others.

- Consider group schemes: If your employer offers health insurance, explore whether it covers pre-existing conditions—it often does.

- Work with a broker: An insurance broker can help you navigate complex policy wording and find coverage tailored to your needs.

Moving Forward: Protecting Your Health and Your Wallet

Understanding the difference between ACC and private health insurance is essential for every Kiwi, especially those managing pre-existing conditions. ACC is a valuable safety net for accidents, but it won't help if you're dealing with an ongoing medical condition. That's where private health insurance comes in—and while it may not cover everything immediately, it's often the only way to access faster specialist care and reduce your out-of-pocket costs.

If you have a pre-existing condition, don't assume you're locked out of health insurance. Explore your options: check whether your employer offers group cover, look into individual policies with waiting periods, and consider working with an insurance broker who understands the nuances of New Zealand's health insurance market. Your health is too important to leave to chance.

Start by reviewing your current coverage and identifying any gaps. If you're uninsured and have a pre-existing condition, get quotes from multiple insurers and speak with a broker. The investment in private health insurance could save you thousands in the long run—and more importantly, it could get you the care you need when you need it most.

Frequently Asked Questions

Sources & References

-

1

Can You Get Health Insurance with a Pre-Existing Condition in NZ? — Buffer Insurance — www.bufferinsurance.co.nz

-

2

What NZ Health Insurance Doesn't Cover — LifeDirect — www.lifedirect.co.nz

- 3

-

4

Insurance in New Zealand: Complete Guide for Migrants (2026) — The Migrate Hub — www.themigratehub.com

- 5

Related Articles

Industry Bodies and Professional Associations NZ

Whether you're launching a business, advancing your career, or navigating financial regulations, industry bodies and professional associations in New Zealand offer invaluable support. These organisati...

Emergency Benefit NZ: When You Have No Other Options

When you're struggling financially and don't qualify for other benefits, the Emergency Benefit might be your lifeline. It's a discretionary payment designed for Kiwis in genuine hardship who've exhaus...

Unpaid Internships NZ: Are They Legal?

Unpaid internships are a common pathway for students and graduates to gain work experience in New Zealand, but there's often confusion about whether they're actually legal. The short answer is: unpaid...

Estate Administration NZ: Managing Someone's Affairs After Death

Losing a loved one is one of life's toughest challenges, and stepping in to manage their estate can feel overwhelming. In New Zealand, estate administration—the process of handling someone's affairs a...