The NZ Healthcare System: How Private Health Insurance Works

Imagine facing a diagnosis that requires surgery, only to learn you'll wait months in the public system. For many Kiwis, private health insurance turns that worry into swift action, offering faster ac...

Emma writes about health, wellbeing, and ACC topics for Lifetimes NZ. She translates complex health information into clear, actionable advice for New Zealand readers.

Imagine facing a diagnosis that requires surgery, only to learn you'll wait months in the public system. For many Kiwis, private health insurance turns that worry into swift action, offering faster access to specialists and private hospitals. In New Zealand's hybrid healthcare setup, understanding how private cover fits alongside our world-class public services can make all the difference.

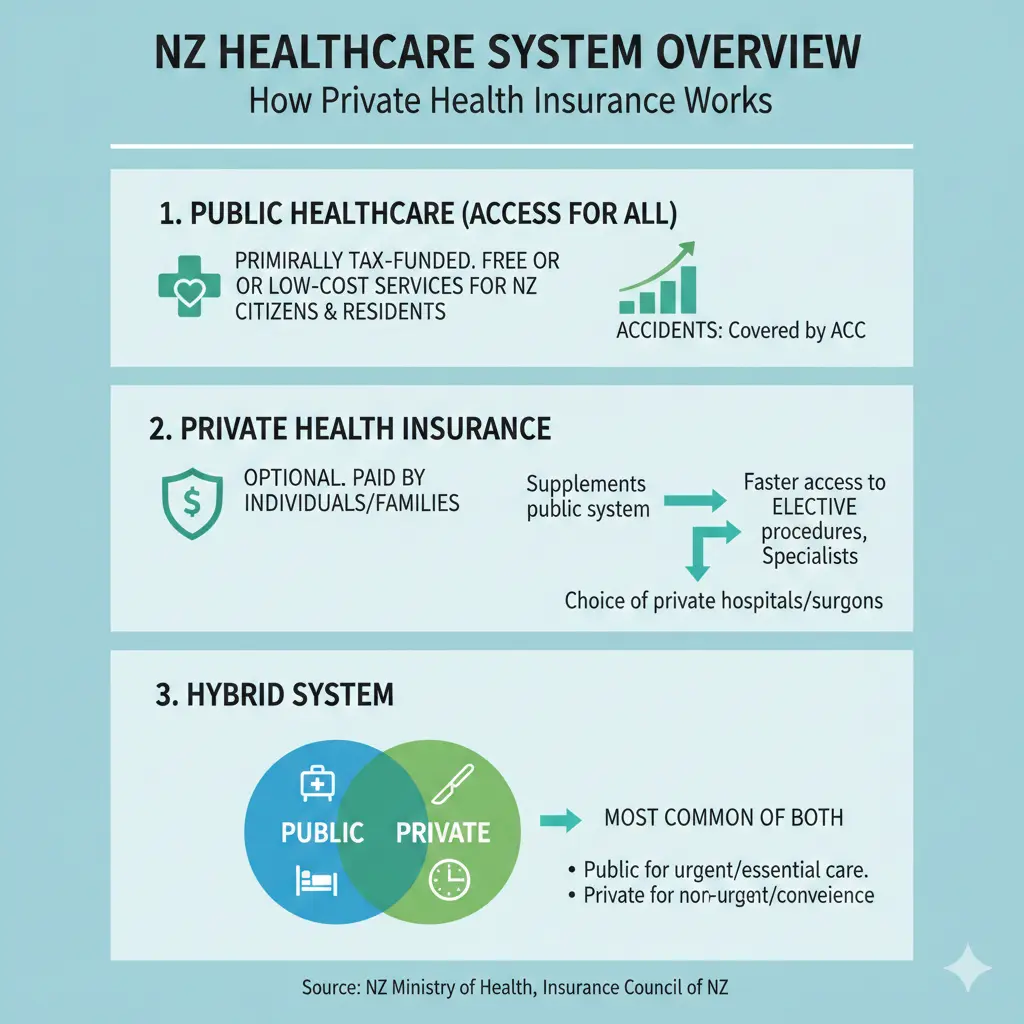

Overview of the NZ Healthcare System

New Zealand's healthcare is a blend of public and private options, ensuring universal access while allowing choice for those seeking speed and comfort. The government funds the public system through taxes and provides free or low-cost care to all residents, including hospital treatment, GP visits (with subsidies), maternity services, and mental health support. However, waiting times for non-urgent procedures—like joint replacements or cataracts—can stretch from weeks to months, pushing many towards private insurance.

Private health insurance complements this by covering elective surgeries, specialist consultations, and extras like dental or optical care not fully funded publicly. About one-third of Kiwis have some form of private cover, mainly held individually rather than through employers. Providers like Southern Cross, nib, AIA, Accuro, UniMed, and AA dominate the market, offering policies tailored to different needs and budgets.

Public vs Private: Key Differences

Here's a quick comparison to highlight why private insurance appeals:

- Access Speed: Public waits for electives can be 100+ days; private often means same-week treatment.

- Choice: Public limits specialist options; private lets you pick from networks of providers.

- Comfort: Private hospitals offer single rooms and hotel-like amenities.

- Coverage Gaps: Public skips most dental, optical, and physiotherapy; private often includes them.

Remember, ACC covers accidents for everyone, regardless of insurance—think broken bones or car crashes—but not illnesses.

Do You Need Private Health Insurance?

It's not essential—our public system ranks among the world's best, delivering comprehensive care free at the point of need. But with rising demand and staff shortages, waits are real. Private cover suits families, over-65s facing age-related ops, or those valuing choice. Expats and recent migrants often opt in for reassurance, especially pre-residency.

Costs are climbing: employee healthcare expenses are forecast to jump 18% in 2026, driven by medical inflation at 14.5%. Premiums vary by age, location, and cover level—expect $100-200/month for a healthy 40-something on a mid-tier plan. Weigh your health history, family risks (e.g., cancer), and finances before deciding.

How Private Health Insurance Works in NZ

Policies fall into tiers: basic (surgeries, tests), mid (adds non-surgical like physio), and comprehensive (everything plus overseas travel). You pay premiums monthly, then claim for approved treatments at private providers. Insurers negotiate rates with hospitals and specialists, but watch for gaps—providers set fees, and you might pay the difference if they exceed insurer caps.

Core Coverages Explained

- Surgical: Hip/knee replacements, cancer ops—often 100% covered up to limits.

- Non-Surgical: Specialist visits, diagnostics (MRIs, mammograms), allergy treatments.

- Pharmac Gaps: Unsubsidised meds for specialist conditions.

- Extras: Dental, optical, physio—check policy details, as these vary.

- Overseas: Rare, but covers treatment unavailable here.

Choose providers in your insurer's network for seamless billing—you pay only co-pays or excesses (typically $200-500). Pre-approval is key for big claims; call your insurer before surgery.

Exclusions and Fine Print

Pre-existing conditions often have moratoriums (6-24 months wait), and lifestyle exclusions apply—no cover for smoking-related ills if undisclosed. Mental health and private psychiatry are limited, as public covers most basics. Always read the Product Disclosure Statement (PDS).

Major Providers and Comparing Policies

Southern Cross leads with 1.3 million members, known for broad networks. nib and AIA offer competitive pricing; Accuro and Partners Life suit budget-conscious Kiwis. Use comparison sites for 2026 quotes—input age, postcode, and needs for personalised rates.

| Provider | Strengths | Avg. Monthly Premium (40yo, Mid Cover) |

|---|---|---|

| Southern Cross | Broad hospital access, extras | $150-180 |

| nib | Flexible plans, wellness perks | $120-160 |

| AIA | Strong surgical cover | $130-170 |

| Accuro | Affordable entry-level | $100-140 |

Shop around annually; switchers save up to 20%.

Costs, Premiums, and Claims Process

Premiums rise with age and claims history—2026 hikes reflect tech advances and wage growth. Claims are straightforward: visit a network provider, get pre-approval, pay upfront or direct settle, then claim online/app. Expect 80-100% reimbursement for in-network care.

Tax relief? No direct credits, but employer subsidies count as fringe benefits—check IRD.

Practical Tips for Kiwis

- Assess Needs: Family history of heart disease? Prioritise cardiac cover.

- Get Quotes: Use MoneyHub or PolicyWise for side-by-side 2026 comparisons.

- Network Check: Ensure local specialists/hospitals are included—e.g., Aucklanders want Mercy or Wakefield.

- Bundle Smart: Pair with life/KiwiSaver for discounts.

- Review Yearly: Life changes? Adjust cover.

Pro tip: Join before 65 to dodge loading on age-related conditions.

Next Steps for Smarter Cover

Ready to explore? Get free quotes from multiple providers today, review your health needs, and chat with a broker if unsure. Pair private insurance with healthy habits to keep premiums low. Always consult a healthcare professional for personal advice—this isn't medical guidance.

Frequently Asked Questions

Sources & References

-

1

Compare Health Insurance NZ 2025: Best Policies, Quotes — www.moneyhub.co.nz

-

2

The New Zealand Health Care System — pnhp.org

-

3

New Zealand Health Insurance For Expats And Foreigners — www.internationalinsurance.com

-

4

Navigating the New Zealand Healthcare System for Expats — expatfinancial.com

-

5

New Zealand | International Health Care System Profiles — www.commonwealthfund.org

-

6

New Zealand Travel Insurance: Plans & Prices — www.squaremouth.com

-

7

Best health insurance NZ 2025: Quotes + comparison chart — www.policywise.co.nz

-

8

New Zealand healthcare costs projected to climb sharply in 2026 — www.insurancebusinessmag.com

-

9

Understanding what's behind rising health insurance costs — www.christchurchinsurance.co.nz

Related Articles

Dental Costs in NZ: Why They are High and How to Save Money

Ever stared at a dentist's quote and felt your wallet recoil? You're not alone—dental costs in New Zealand have skyrocketed, leaving many Kiwis skipping check-ups or delaying essential treatments. Wit...

How Much Does a GP Visit Cost in NZ?

Ever wondered why that nagging cough or unexpected rash sends you scrambling for your wallet before even booking a GP appointment? You're not alone—figuring out how much a GP visit costs in NZ is a co...

Emergency Department or Urgent Care: Where Should You Go?

Picture this: it's 2am, your child's fever is spiking, or you've twisted an ankle playing weekend footy. Do you race to the nearest **Emergency Department** or hunt for an **Urgent Care** clinic? Maki...

Prescription Costs & Subsidies in New Zealand 2025

If you're managing a long-term health condition in Aotearoa, understanding how much you'll pay for prescriptions can help you budget better and plan your healthcare. New Zealand's prescription system...