Health Insurance Waiting Periods: What's Excluded When

Imagine facing a sudden health scare in New Zealand's overburdened public system, where over 74,000 Kiwis waited more than four months for their first specialist assessment as of February 2025.Health...

Sarah covers personal finance, tax, and KiwiSaver topics for Lifetimes NZ. She focuses on making money management straightforward and practical for everyday Kiwis.

Imagine facing a sudden health scare in New Zealand's overburdened public system, where over 74,000 Kiwis waited more than four months for their first specialist assessment as of February 2025.Health insurance promises a lifeline, but what if your claim is denied because of a waiting period you didn't know about? Understanding health insurance waiting periods and what's excluded during them is crucial for every Kiwi looking to safeguard their family's health without nasty surprises.

With public waiting lists stretching into years—over 3,900 patients waited more than 12 months for treatment in September 2023—private health insurance lets you skip the queues and access top specialists privately.But waiting periods built into policies mean certain treatments aren't covered right away, protecting insurers from immediate high-risk claims. This guide breaks down everything you need to know about health insurance waiting periods in New Zealand for 2026, including common exclusions, pre-existing conditions, and tips to choose wisely.

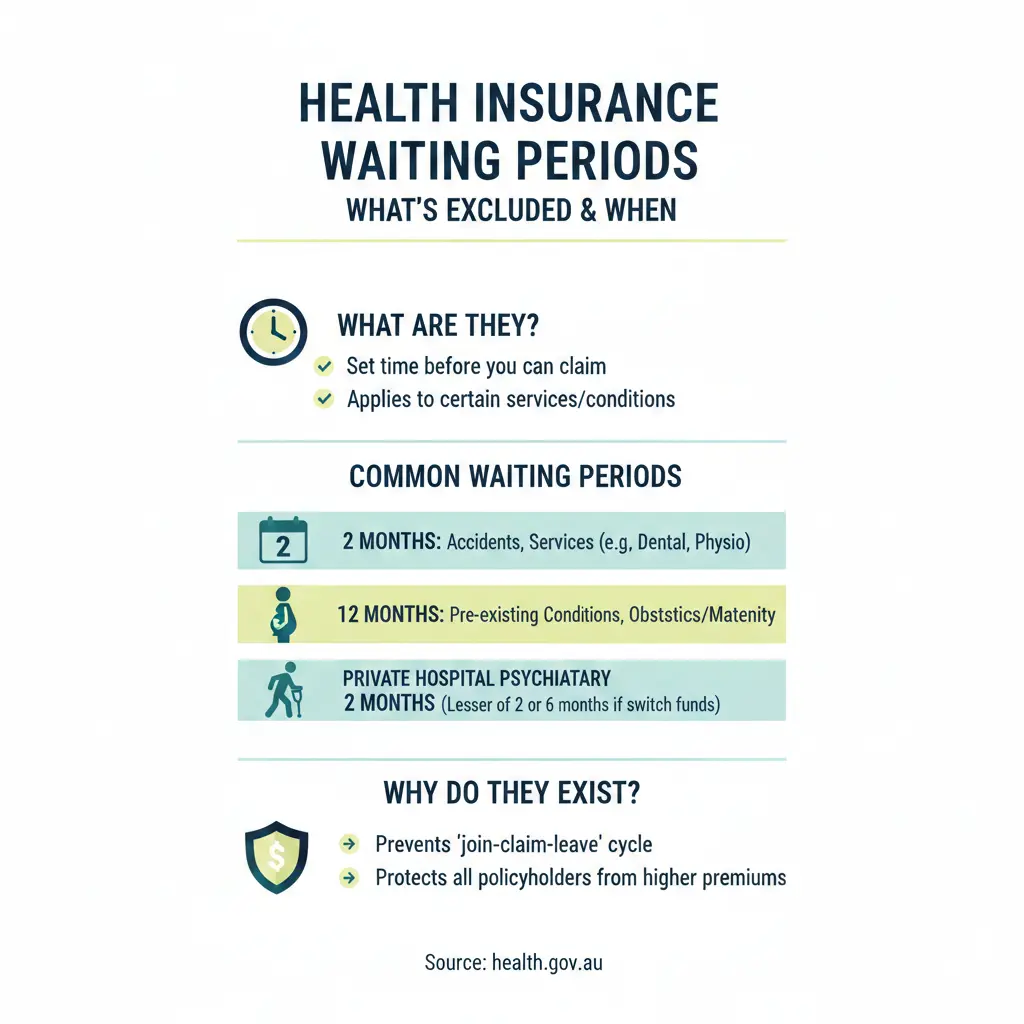

What Are Health Insurance Waiting Periods?

A health insurance waiting period, also called a stand-down period, is the initial time after your policy starts when you can't claim for specific treatments or conditions. These periods vary by insurer, policy type, and treatment, typically ranging from 90 days to three years.They're designed to prevent people from buying insurance only after symptoms appear, ensuring the risk pool remains sustainable for all policyholders.

In New Zealand, most comprehensive health policies cover core benefits like hospital stays and surgeries from day one. However, optional extras and high-risk procedures often come with delays. For instance, as of 2026, major providers enforce these to balance premiums and coverage.Reviewing your policy's Product Disclosure Statement (PDS) is essential, as terms can differ between insurers like Southern Cross, Partners Life, or nib.

Why Do Waiting Periods Exist in NZ Health Insurance?

- Risk management: Insurers avoid adverse selection, where only sick people sign up.

- Premium stability: Spreads costs fairly across healthy and at-risk members.

- Public system integration: Encourages using free public GP services initially, reserving private cover for non-urgent needs.

Health New Zealand | Te Whatu Ora reports ongoing strains, with 27,000 to 37,000 patients waiting over four months for treatments from March 2024 to February 2025, underscoring why Kiwis turn to private options—but with these built-in safeguards.

Common Health Insurance Waiting Periods in New Zealand

Waiting periods aren't one-size-fits-all. Here's a breakdown of typical durations from leading NZ providers in 2026, based on policy reviews. Always confirm with your insurer, as updates occur annually.

| Treatment Category | Typical Waiting Period | Examples |

|---|---|---|

| GP Visits & Serious Conditions | 90 days | Consultations, initial diagnoses |

| Dental & Optical | 3 months | Teeth cleanings, glasses, contacts |

| Health Checks | 6 months | Proactive screenings |

| Specific Procedures | 1 year | Impacted teeth extraction, obstetrics, vasectomy |

| Major Surgeries | Up to 3 years | Breast reduction, gastric bypass, palliative care |

These align with Canstar's analysis of major policies, where elective treatments often cap lifetime claims too.Accidental injuries usually have zero waiting periods, providing immediate cover—a key benefit for active Kiwis.

Waiting Periods for Pre-Existing Conditions

Pre-existing conditions—any diagnosed or treated issue before policy start—are the biggest exclusion. Most NZ policies exclude them entirely, but some offer coverage after long waits: 12 months to four years, depending on the provider and condition severity.

For example, if you have ongoing back pain, you might wait three years for related surgery cover. Insurers like those reviewed by Imsure assess applications individually; continuous prior cover elsewhere can sometimes shorten this via portability credits. Expats note: Visa health requirements mean chronic issues could bar entry, making early insurance vital.

What's Excluded During Health Insurance Waiting Periods?

During waiting periods, claims for listed treatments are fully excluded—no reimbursement, even if urgent. Common exclusions include:

- Elective and cosmetic procedures: Gastric banding, breast reductions (up to 3 years).

- Reproductive services: Obstetrics, fertility treatments (1+ years).

- Dental extras: Beyond emergencies, like extractions (1 year for impacted teeth).

- Pre-existing or related conditions: Anything linked to prior health history, often forever unless waived.

- High-risk therapies: Palliative or prophylactic care (3 years).

If you claim too early, it's rejected outright. Post-period, coverage kicks in, but excess fees or co-pays may apply. Moneyhub advises checking for policy caps on electives.

"Waiting periods may apply to specific treatments, pre-existing conditions, or for a set period after joining a new policy. These can vary between providers."

How Waiting Periods Affect New Zealanders

For Kiwis, long public waits—up to 400 patients over a year for surgery despite zero targets—make insurance appealing, with 25% of doctors now private-only by mid-2024. But exclusions hit hard: a new parent can't claim maternity costs immediately, or a fitness enthusiast faces dental delays post-policy.

Expats and visa holders face extra hurdles; it takes up to three months to enrol with a GP via the public system, amplifying private needs. In 2026, with Health NZ streamlining info via a single portal by mid-year, awareness is rising—but so are premiums amid system strains.

Real Kiwi Examples

- Auckland family: Signed up for comprehensive cover; waited 90 days for child's tonsillectomy after GP referral—public list was 6+ months.

- Wellington expat: Pre-existing asthma excluded surgery for 2 years; portability from UK policy reduced it to 12 months.

- Christchurch retiree: Gastric procedure denied at 18 months; switched providers crediting time served.

Tips to Minimise Health Insurance Waiting Periods

Don't let exclusions catch you out. Here's actionable advice for Kiwis:

- Compare policies early: Use tools from Canstar or Policywise to find shorter waits or zero-period options for accidents.

- Disclose everything: Honesty upfront avoids claim denials; brokers help negotiate pre-existing waivers.

- Opt for reductions: Some plans let you buy shorter PED waits (e.g., 1-2 years) for extra premium—worth it for families.

- Port your cover: Continuous insurance credits prior waiting time when switching.

- Read the PDS: Check insurer sites or consult advisers—free via licenced brokers.

- Bundle family policies: Multi-member discounts often align waits.

Budget tip: Basic policies start at $50/month per adult; comprehensive ~$150+, tax-deductible for self-employed via IRD. Always seek professional advice—this isn't financial advice.

Next Steps for Kiwi Health Security

Protect your whānau from public delays and policy pitfalls: Get quotes from multiple NZ insurers today, review PDS for waits, and chat with a licenced adviser. Sites like Policywise offer free matching to your needs. Remember, while public care is free, time isn't—health insurance with smart waiting awareness delivers peace of mind.

Disclaimer: This is general information only. Consult a qualified financial adviser or insurer for personalised advice tailored to your situation. Premiums and terms change; verify 2026 rates.

Frequently Asked Questions

Sources & References

-

1

Long waiting lists and wait times in NZ's public health system — policywise.co.nz — www.policywise.co.nz

-

2

How Long Before I Can Claim on my Health Insurance? — canstar.co.nz — www.canstar.co.nz

-

3

New Zealand Health Insurance For Expats And Foreigners — internationalinsurance.com — www.internationalinsurance.com

-

4

Health insurance for pre-existing conditions — imsure.co.nz — www.imsure.co.nz

-

5

Compare Health Insurance NZ 2026: Best Policies, Quotes & Deals — moneyhub.co.nz — www.moneyhub.co.nz

-

6

What is Waiting Period in Health Insurance 2026 — policybazaar.com — www.policybazaar.com

-

7

Health New Zealand | Te Whatu Ora — tewhatuora.govt.nz — www.tewhatuora.govt.nz

Related Articles

Industry Bodies and Professional Associations NZ

Whether you're launching a business, advancing your career, or navigating financial regulations, industry bodies and professional associations in New Zealand offer invaluable support. These organisati...

Emergency Benefit NZ: When You Have No Other Options

When you're struggling financially and don't qualify for other benefits, the Emergency Benefit might be your lifeline. It's a discretionary payment designed for Kiwis in genuine hardship who've exhaus...

Unpaid Internships NZ: Are They Legal?

Unpaid internships are a common pathway for students and graduates to gain work experience in New Zealand, but there's often confusion about whether they're actually legal. The short answer is: unpaid...

Estate Administration NZ: Managing Someone's Affairs After Death

Losing a loved one is one of life's toughest challenges, and stepping in to manage their estate can feel overwhelming. In New Zealand, estate administration—the process of handling someone's affairs a...