KiwiSaver Death Benefit: What Happens to Your Savings

Imagine this: you've diligently contributed to your KiwiSaver for decades, watching it grow into a substantial nest egg. But what happens to those hard-earned savings when you're no longer here to enj...

The Lifetimes NZ editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes NZ readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Imagine this: you've diligently contributed to your KiwiSaver for decades, watching it grow into a substantial nest egg. But what happens to those hard-earned savings when you're no longer here to enjoy them? For Kiwis, understanding the KiwiSaver death benefit ensures your savings go exactly where you intend, avoiding unnecessary delays or disputes for your loved ones.

In New Zealand, KiwiSaver funds don't vanish or go to the government upon death—they form part of your estate and are distributed according to your will or intestacy rules. With average balances often exceeding $20,000, getting this right is crucial, especially as KiwiSaver has become one of our largest solely-owned assets. This guide breaks down the process, recent rule changes, and practical steps to protect your family's future.

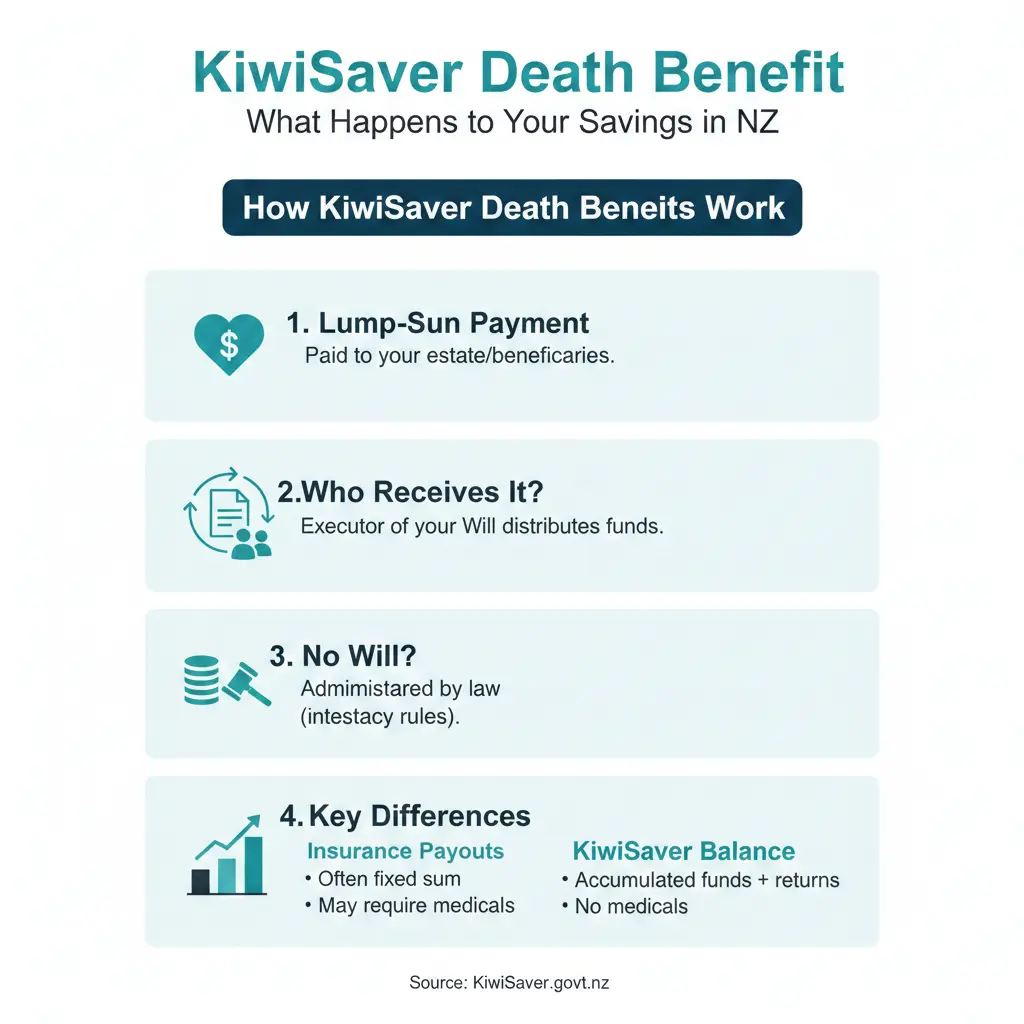

How KiwiSaver Death Benefits Work in New Zealand

When a KiwiSaver member dies, the trustees of the scheme must pay the full account balance—including member contributions, employer matches, and Crown contributions—to the member's personal representative upon application. This amount is calculated on the date the application is accepted and becomes part of the deceased's estate, alongside homes, bank accounts, and other assets.

Unlike life insurance or joint bank accounts, you cannot nominate a direct beneficiary for your KiwiSaver funds through your provider. Instead, distribution follows your will or the Administration Act 1969 if you die intestate (without a will). This setup ensures funds are handled securely but requires proactive planning.

Key Steps After a KiwiSaver Member's Death

- Notify the Provider: The personal representative (executor if there's a will, or administrator) contacts the KiwiSaver provider with proof of death, such as a death certificate.

- Application Process: Submit a formal application; trustees verify and release funds to the estate.

- Estate Distribution: Funds pay estate debts, taxes, and expenses first, then go to beneficiaries as specified.

Providers vary in their processes—some release funds pre-probate, others wait—highlighting the need to check with your scheme.

Impact of Account Balance: The $40,000 Threshold

A major 2023 rule change raised the threshold for accessing KiwiSaver funds without probate from $15,000 to $40,000, simplifying things for smaller estates. This update addresses the reality that most KiwiSaver balances now exceed the old limit, reducing court costs that could devour modest estates.

| Account Balance | Process Required | Who Can Apply |

|---|---|---|

| Under $40,000 | No probate or letters of administration needed | Partner, children, or caregiver for children—apply directly to provider |

| Over $40,000 | Probate (with will) or letters of administration (no will) required | Executor/administrator via High Court, then provider releases to estate |

For example, if your balance is $30,000, your spouse could access it quickly with a death certificate, ideal for covering funeral costs when other estate funds are tied up. Above $40,000—like the average KiwiSaver balance of around $55,000 (per 2019 FMA data, likely higher in 2026)—court approval adds time and expense.

Real-Life Example: Avoiding Probate Pitfalls

Consider a case where a father's KiwiSaver grew past $15,000 post-death but pre-application. His son faced delays until the threshold rose to $40,000, allowing payout without probate via FSCL mediation. Today, with the higher limit, families save time and money, but joint assets like homes still bypass probate.

With a Will vs. Without: Protecting Your Wishes

If You Have a Will

Your will dictates distribution—specify KiwiSaver explicitly to avoid ambiguity. Name an executor you trust; they'll apply for probate if needed, then claim funds. Relationship property claims (e.g., from a de facto partner) may still apply under the Property (Relationships) Act 1976.

- Tip: Update your will after life events like marriage, kids, or KiwiSaver balance growth. Providers like Fisher Funds stress this for smaller estates.

- Action: Store your will safely and inform your executor of your KiwiSaver details.

If You Die Intestate (No Will)

Under the Administration Act 1969, funds go to spouses/partners first, then children, parents, siblings—in that rough order. Courts appoint an administrator, potentially delaying access and overriding your unspoken wishes. Intestacy is common—don't leave it to chance.

"It's still important that checks and safeguards remain in place to protect people's money." — Generate customer service manager Dan Alden on probate processes

Taxes, IRD, and Other Considerations

KiwiSaver death benefits are not taxed as income for recipients, but estate income earned post-death may be. Notify IRD promptly with proof of death; processing takes about 10 weeks. Pay any outstanding taxes, ACC debts, or WINZ overpayments from the estate before distribution.

Crown contributions are included fully. For significant financial hardship or serious illness withdrawals pre-death, different rules apply—but death benefits are straightforward estate payouts.

Common Myths Busted

- Myth: Government takes it all. Fact: No—straight to estate.

- Myth: Auto-pays to spouse. Fact: Follows will/intestacy.

- Myth: Direct beneficiary nomination possible. Fact: Not via KiwiSaver.

Practical Tips for KiwiSaver Estate Planning

Secure your KiwiSaver death benefit with these actionable steps:

- Draft or Update Your Will: Use Public Trust or a lawyer; cost under $500 for simple ones. Include KiwiSaver specifics.

- Check Balance Regularly: If nearing $40,000, prioritise probate planning.

- Discuss with Family: Share provider details (e.g., AMP, Fisher Funds) and will location.

- Consider Enduring Power of Attorney (EPOA): Appoint someone now for incapacity, easing future estate management.

- Review Annually: Life changes? Update via your provider's online portal.

For estates with KiwiSaver as the main asset, a will prevents High Court delays—17,500 applications yearly pre-change. Pair with KiwiSaver growth strategies for maximum impact.

Next Steps: Secure Your KiwiSaver Legacy Today

Your KiwiSaver is more than savings—it's your legacy. Start by reviewing your will and contacting your provider for a balance statement. Consult a lawyer or Public Trust for personalised advice, and notify IRD if managing a deceased estate. With planning, your savings support your whānau seamlessly.

Disclaimer: This is general information, not personalised financial advice. Tax laws and thresholds can change; seek professional advice from a lawyer, accountant, or financial adviser for your situation. Rates current as of 2026.

Frequently Asked Questions

Sources & References

-

1

KiwiSaver scheme rules - Tax Technical - Inland Revenue — www.taxtechnical.ird.govt.nz

-

2

Rule change helps improve access to KiwiSaver after death - RNZ — www.rnz.co.nz

-

3

What happens to your KiwiSaver funds if you die? - AMP — www.amp.co.nz

-

4

What Happens to my KiwiSaver money if I Die? - National Capital — www.nationalcapital.co.nz

-

5

What Happens to KiwiSaver When You Die? An In Depth Guide - One Stop Financial — onestopfinancial.co.nz

-

6

What Happens To KiwiSaver Funds if I Die? - LegalVision NZ — legalvision.co.nz

-

7

What Happens to Your KiwiSaver When You Die - Aurora Capital — aurora.co.nz

-

8

Do You Have KiwiSaver? Then You NEED A Will - Smith Partners — smithpartners.co.nz

-

9

Making sure your KiwiSaver house is in order - Fisher Funds — fisherfunds.co.nz

-

10

Let us know someone has died - Inland Revenue — www.ird.govt.nz

Related Articles

Working Multiple Jobs NZ: Tax and Legal Considerations

Juggling multiple jobs can boost your income, but it's crucial to understand the tax implications and legal requirements that come with working more than one role in Aotearoa. Whether you're a contrac...

Name Changes NZ: Legal Process and Costs

Considering a fresh start with a new name? Whether it's after marriage, divorce, or simply embracing a personal transformation, changing your name in New Zealand is straightforward but requires follow...

Holiday Home Tax Rules NZ: Private Use and Rental

Own a bach in Coromandel or a holiday home in Queenstown? You're not alone—many Kiwis cherish these escapes, but renting them out while enjoying personal use can trip you up on tax rules. Getting the...

Industry Bodies and Professional Associations NZ

Whether you're launching a business, advancing your career, or navigating financial regulations, industry bodies and professional associations in New Zealand offer invaluable support. These organisati...