KiwiSaver Funds Compared: Which Type is Right for You?

Ever wondered if your KiwiSaver fund is pulling its weight, or if there's a better match out there for your dreams—like that bach by the beach or a comfy retirement? You're not alone; with over 2.8 mi...

Sarah covers personal finance, tax, and KiwiSaver topics for Lifetimes NZ. She focuses on making money management straightforward and practical for everyday Kiwis.

Ever wondered if your KiwiSaver fund is pulling its weight, or if there's a better match out there for your dreams—like that bach by the beach or a comfy retirement? You're not alone; with over 2.8 million Kiwis in KiwiSaver, picking the right fund type can feel overwhelming, but it's one of the smartest moves you can make for your financial future.Comparing KiwiSaver fund types—from Defensive to Aggressive—helps you balance risk, returns, and your timeline, so let's dive in and find what suits you best.

Understanding KiwiSaver Fund Types in New Zealand

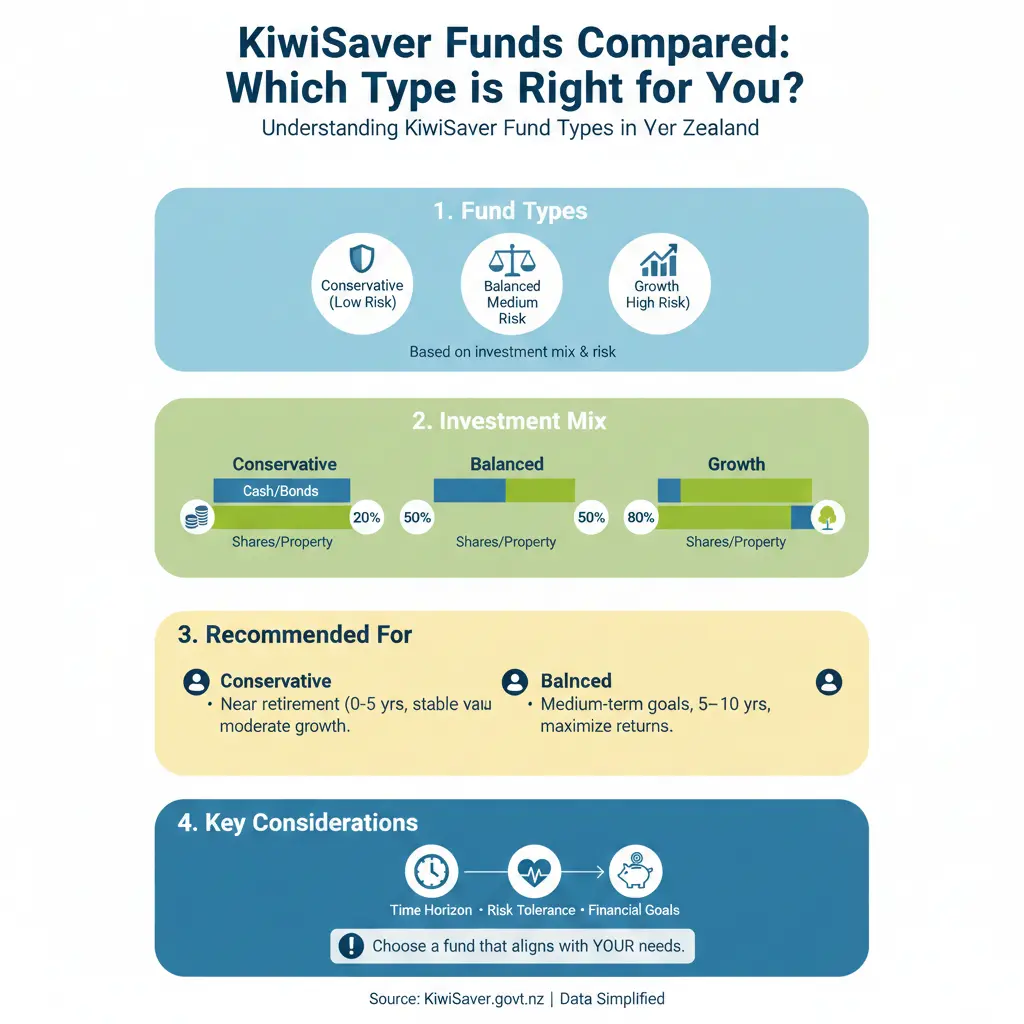

KiwiSaver funds are grouped into five main types: Defensive (also called Cash), Conservative, Balanced, Growth, and Aggressive (sometimes labelled High Growth). Each has a distinct mix of assets like cash, bonds, shares, and property, affecting their risk profile and potential returns. The Financial Markets Authority (FMA) regulates these, ensuring transparency on risk indicators from 1/7 (lowest) to 7/7 (highest).

Your choice depends on your age, risk tolerance, and how long until you need the money—typically 5+ years for growth. Default funds (like those from BNZ, Booster, or Simplicity) are Balanced for auto-enrolled savers. Providers like Milford, Generate, and Pathfinder offer variations, including socially responsible options.

Defensive (Cash) Funds: Safe as Houses

These are the chill-out funds for when you want stability over excitement. Mostly in bank deposits and fixed-interest (20% or less in growth assets like shares), they're risk profile 1/7—perfect if you're nearing retirement or can't stomach market dips.

- Who suits: Over-65s, risk-averse folks, or those with a 0-3 year horizon.

- Risk vs return: Lowest risk, but returns lag inflation (around 1-2% annually after fees). Great for preserving capital.

- 2026 averages: Expect modest gains; Milford's CashPlus (ex-Defensive) focuses on cash-like stability.

If markets crash, these barely blink, but over decades, they won't grow your nest egg much.

Conservative Funds: A Gentle Step Up

Building on Defensive, these hold mostly cash and bonds (around 70%), with 30% in shares/property. Risk profile 3/7, suitable for 3-5+ year timelines.

- Who suits: 50+ Kiwis, cautious investors, or those protecting family savings.

- Risk vs return: Low-medium risk; smoother ride than growth funds, with better inflation-beating potential.

- 2026 averages: Pathfinder Conservative at 3.65% over 5 years—one of the steadier performers.

Ideal if you're dipping toes into investing without sleepless nights.

Balanced Funds: The Even-Keeled Choice

Medium risk (profile 4/7), with 50-60% split between growth (shares/property) and defensive assets. Default provider funds often land here.

- Who suits: Mid-40s to 60s, moderate risk tolerance, 5-7+ year horizon.

- Risk vs return: Balanced volatility; good for most Kiwis wanting steady growth without extremes.

- 2026 averages: Quaystreet Socially Responsible Balanced at 7.76% over 5 years, shining for ethical investors.

Providers like Generate and ASB offer these as core options, blending global and NZ assets.

Growth Funds: Revving Up for the Long Haul

Higher risk (profile 5/7), with 70-80% in shares/property. Minimum 7+ years suggested.

- Who suits: 30-50s, medium-high risk tolerance, building serious wealth.

- Risk vs return: More ups and downs, but historically higher returns to outpace inflation.

- 2026 averages: Milford Growth at 10.12% over 5 years—top-tier performance.

Pathfinder's Growth fund appeals to ethical savers, with strong awards.

Aggressive (High Growth) Funds: High Octane for Bold Kiwis

The thrill-seekers: 80-100% growth assets, risk profile 6-7/7, for 10+ year horizons.

- Who suits: Under-40s, high risk tolerance, maximising retirement pots.

- Risk vs return: Big swings possible (e.g., 20% drops in bad years), but best long-term returns.

- 2026 averages: Milford Aggressive at 10.07% over 5 years; Generate's geared options push further.

Suits young professionals or those with emergency funds elsewhere.

KiwiSaver Funds Compared: Side-by-Side Breakdown

Here's a quick comparison table to compare KiwiSaver fund types at a glance, using 2026 data and standard profiles.

| Fund Type | Risk Profile | Asset Mix (Growth %) | 5-Year Avg Return (2026) | Best For (Age/Timeline) |

|---|---|---|---|---|

| Defensive/Cash | 1/7 | 0-20% | ~1-2% | 65+ / 0-3 yrs |

| Conservative | 3/7 | ~30% | 3.65% (Pathfinder) | 50+ / 3-5 yrs |

| Balanced | 4/7 | 50-60% | 7.76% (Quaystreet SR) | 40-60 / 5-7 yrs |

| Growth | 5/7 | 70-80% | 10.12% (Milford) | 30-50 / 7+ yrs |

| Aggressive | 6-7/7 | 80-100% | 10.07% (Milford) | Under 40 / 10+ yrs |

Past returns aren't guarantees, but they show trends. Milford and Pathfinder lead in multiple categories.

Risk vs Return: What You Need to Know

Higher risk often means higher long-term returns, but short-term losses hurt. Over 10 years, Growth/Aggressive have averaged 8-12%, vs 2-4% for Conservative. Factor in fees (0.3-1.5% PIR-taxed) and your KiwiSaver contributions (at least 3%, plus employer/govt top-ups).

Practical tip: Use Sorted's KiwiSaver Fund Finder to check your fund's star rating and fees—it's free and compares all 300+ options.

Who Should Choose Which Fund? By Age and Risk Tolerance

- 20s-30s (High tolerance): Aggressive or Growth—time is on your side for recovery.

- 40s (Medium): Balanced or Growth—balance family needs with growth.

- 50s-60s (Low-medium): Conservative or Balanced—protect gains.

- Nearing retirement: Defensive—shift gradually (lifecycle funds auto-do this).

Assess your risk with FMA's tool or chat to a Sorted adviser. Socially responsible? Milford or Pathfinder excel.

How to Switch KiwiSaver Funds: Easy Steps for Kiwis

Switching is free, simple, and doesn't reset your balance. Here's how:

- Log in: Via your provider's app/site (e.g., Milford app for real-time tracking).

- Compare: Use Canstar or Sorted tools.

- Choose: Select new fund—many allow multi-fund mixes.

- Confirm: Takes 1-2 weeks; contributions redirect automatically.

- Monitor: Review annually or after life changes (e.g., kids, job switch).

No lock-in penalties, but check for exit fees (rare). IRD handles tax via PIR—update if income changes.

Top-Performing Providers in 2026

Milford dominates Growth/Aggressive (10%+ returns), Pathfinder for ethical Conservative (3.65%), Quaystreet for Balanced. Compound Wealth offers bespoke advice for high-net-worth. ANZ suits bank loyalists with convenience.

Practical Tips to Maximise Your KiwiSaver

- Contribute at least 3% for govt $521/year (18-65s).

- Salary sacrifice via payroll for tax perks.

- Review fees—aim under 0.8%.

- Diversify with ethical or geared options if suitable.

- Track via apps; withdraw for first home (with conditions).

Disclaimer: This isn't personalised advice. Consult a licensed adviser or use free Sorted tools before changing funds. Past performance doesn't predict future results, and investments can fall in value.

Next Steps: Take Control Today

Grab your KiwiSaver statement, hop on Sorted's Fund Finder, and compare options that match your life stage. Chat with a financial adviser via MoneyTalks (0800 345 123) or your provider—small tweaks now could add thousands by retirement. You've got this, Kiwi—start building that secure future!

Frequently Asked Questions

Sources & References

-

1

Best KiwiSaver providers: 2025 comparison - Policywise — www.policywise.co.nz

-

2

Best KiwiSaver Funds 2026 | KiwiSaver Options & Best Returns — www.nationalcapital.co.nz

-

3

Best Performing KiwiSaver Funds in 2026 | MEXC News — www.mexc.co

-

4

Compare KiwiSaver Funds — www.canstar.co.nz

-

5

Best KiwiSaver Providers in 2026 - Compound Wealth — www.compoundwealth.co.nz

-

6

Compare ASB KiwiSaver Scheme funds — www.asb.co.nz

-

7

Top KiwiSaver Funds Ranked For 2026! - YouTube — www.youtube.com

-

8

Compare KiwiSaver Funds | AMP New Zealand — www.amp.co.nz

-

9

Our Favourite KiwiSaver Funds — www.moneyhub.co.nz

-

10

KiwiSaver fund finder - Sorted — sorted.org.nz

Related Articles

Industry Bodies and Professional Associations NZ

Whether you're launching a business, advancing your career, or navigating financial regulations, industry bodies and professional associations in New Zealand offer invaluable support. These organisati...

Emergency Benefit NZ: When You Have No Other Options

When you're struggling financially and don't qualify for other benefits, the Emergency Benefit might be your lifeline. It's a discretionary payment designed for Kiwis in genuine hardship who've exhaus...

Unpaid Internships NZ: Are They Legal?

Unpaid internships are a common pathway for students and graduates to gain work experience in New Zealand, but there's often confusion about whether they're actually legal. The short answer is: unpaid...

Estate Administration NZ: Managing Someone's Affairs After Death

Losing a loved one is one of life's toughest challenges, and stepping in to manage their estate can feel overwhelming. In New Zealand, estate administration—the process of handling someone's affairs a...