How to Build an Emergency Fund (NZ Guide)

If you've ever been caught off guard by an unexpected car repair, medical bill, or job loss, you'll know how stressful financial emergencies can be. An emergency fund is your financial safety net—mone...

Sarah covers personal finance, tax, and KiwiSaver topics for Lifetimes NZ. She focuses on making money management straightforward and practical for everyday Kiwis.

If you've ever been caught off guard by an unexpected car repair, medical bill, or job loss, you'll know how stressful financial emergencies can be. An emergency fund is your financial safety net—money set aside specifically to cover life's surprises without resorting to high-interest credit cards or loans. The good news? Building one is entirely achievable, and we're here to show you how.

Why New Zealanders Need an Emergency Fund

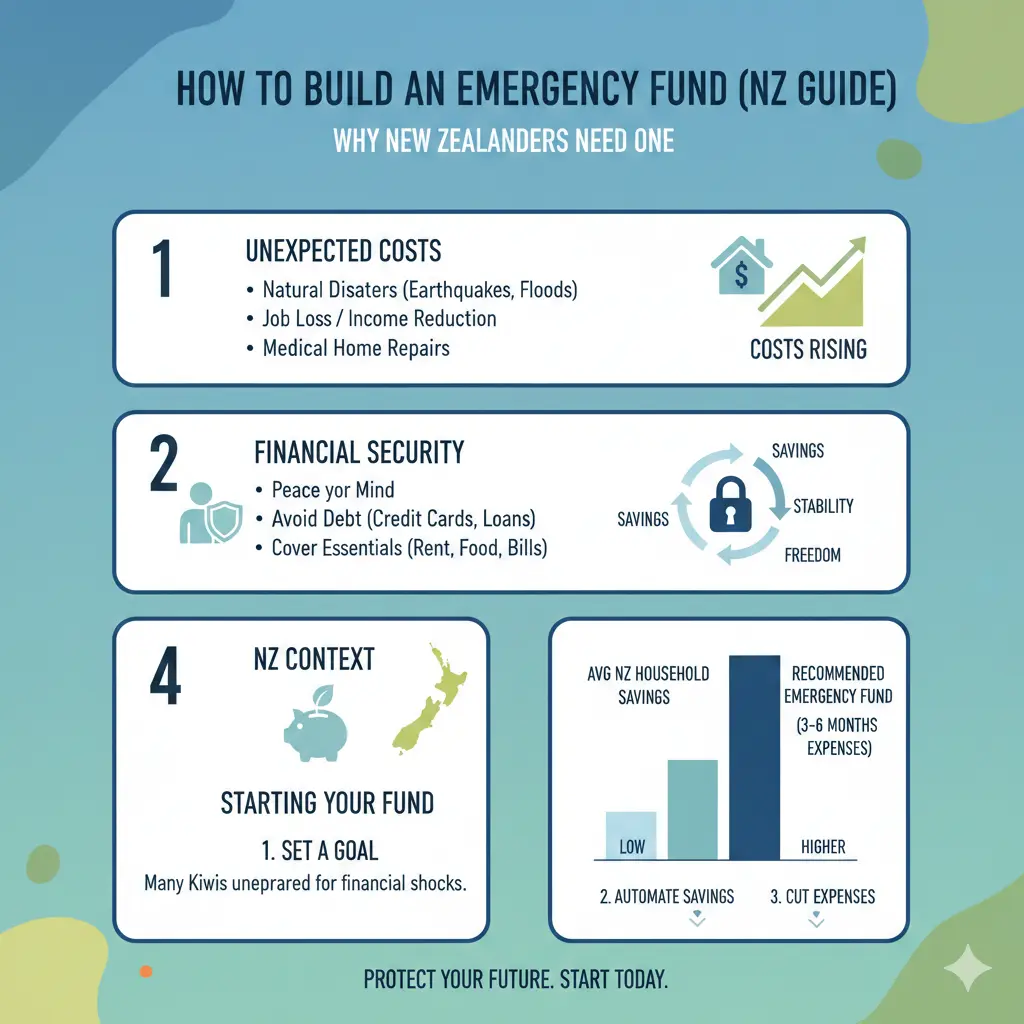

The statistics paint a sobering picture of Kiwi finances. Research shows that only one in three New Zealanders could last more than a month financially if they lost their job, and just one in four could manage three months without income. Even more concerning, more than one million New Zealanders have no emergency savings at all.

With New Zealand's cost-of-living pressures, having an emergency fund has never been more critical. When unexpected expenses arise—and they will—you'll face a choice: raid your emergency fund or take on debt. Without that safety net, many Kiwis turn to credit cards or personal loans, which can spiral into expensive long-term debt.

Beyond the practical benefits, research from the Retirement Commission shows that people with an emergency fund are much more likely to feel optimistic and confident about their future, and less likely to worry about finances from one pay day to the next.

How Much Should You Save?

The most common recommendation is to have three to six months' worth of living expenses saved in your emergency fund. However, the right amount for you depends on your personal circumstances.

Calculating Your Target Amount

Start by working out your actual monthly expenses. The best way to do this is to download your bank and credit card statements from the last year, then add up everything you've spent (excluding transfers between accounts). This gives you a realistic picture of your true living costs.

Stats NZ data shows the average weekly household expenditure in New Zealand is $1,598, but this varies significantly. Many households spend more than 40 percent of their income on housing alone.

Once you know your monthly expenses, multiply that figure by three (or six for greater security). For example, if your monthly expenses are $4,000, your emergency fund target would be $12,000 to $24,000.

Factors to Consider

Your emergency fund should reflect your unique situation. Consider these questions:

- Are you the sole income earner in your household?

- Do you have children or dependents?

- Do you have a mortgage or large regular expenses?

- Could family members provide financial assistance in a crisis?

- How long would it realistically take you to find another job?

- What insurance do you have in place (income protection, car insurance, etc.)?

If you're single with no dependents, you might need less of a buffer than someone supporting a family. Similarly, if you have job security or supplementary income sources, you may need less than someone in a precarious employment situation.

Minimum Emergency Fund Targets

If the three-to-six-month target feels overwhelming, here are some realistic minimums to aim for:

- $5,000 minimum for a single person

- $10,000 minimum for a couple

- A realistic emergency fund for most people is around $10,000 to $20,000

Step-by-Step Guide to Building Your Emergency Fund

Step 1: Assess Your Monthly Expenses

Make a detailed list of all your essential monthly costs. Include:

- Rent or mortgage payments

- Groceries and food

- Electricity, water, and gas

- Phone and broadband

- Insurance (home, car, health)

- Childcare or education costs

- Transport and fuel

- Any loan repayments

Be honest about your spending. Check your last year of bank statements to see what you actually spend, not what you think you spend.

Step 2: Set a Realistic Savings Goal

Don't let the final target intimidate you. If you need $15,000 but currently have nothing saved, that's a marathon, not a sprint. Start with a smaller goal—even $1,000 is a solid first milestone. Once you've reached that, aim for $5,000, then work towards your three-to-six-month target. Every contribution counts.

Step 3: Choose Where to Keep Your Emergency Fund

Your emergency fund needs to be easily accessible but separate from your everyday spending money. Consider:

- A dedicated savings account with your current bank—keeps it close but separate

- A high-interest savings account—earn a bit while you save (check current rates with providers like ASB, BNZ, Westpac, or ANZ)

- A term deposit ladder—if you want slightly better returns, though this reduces accessibility

Avoid investing your emergency fund in shares or KiwiSaver—you need quick access to these funds without worrying about market fluctuations.

Step 4: Automate Your Savings

Set up an automatic transfer from your main account to your emergency fund account on payday. Even $50 per week adds up—that's $2,600 per year. The key is consistency; automate it so you don't have to think about it.

Step 5: Use the 50/30/20 Budget Strategy

To free up money for your emergency fund, try the 50/30/20 budget approach:

- 50% of your income for fixed essentials (housing, utilities, food, transport)

- 30% for wants and luxuries (entertainment, dining out, hobbies)

- 20% for debt repayment and savings

Focus that 20% on clearing high-interest credit card debt first, then building your emergency fund.

Where to Keep Your Emergency Fund

Your emergency fund should be:

- Easily accessible—you might need it within days

- Safe and secure—ideally in a bank account covered by the Deposit Protection Scheme (up to $100,000 per person, per bank)

- Separate from everyday spending—out of sight, out of mind, so you're not tempted to dip into it

- Earning some interest—while not your priority, a high-interest savings account helps your fund grow

Avoid keeping large amounts in cash at home, and don't invest your emergency fund in shares or property—you need liquidity and certainty.

What Counts as an Emergency?

Your emergency fund is for genuine, unexpected expenses. Legitimate emergencies include:

- Job loss or unexpected income reduction

- Major car repairs or replacement

- Urgent home repairs (roof leak, plumbing failure)

- Medical or dental emergencies

- Unexpected travel (family emergency)

- Temporary inability to work due to illness or injury

It's not for planned expenses like holidays, Christmas shopping, or lifestyle upgrades. Keep your emergency fund sacred—it's your financial safety net, not a piggy bank for wants.

Getting Started Today

Building an emergency fund doesn't require a windfall or perfect income. It requires commitment and consistency. Start today by calculating your monthly expenses, then set up an automatic transfer of whatever amount you can afford—even $25 per week makes a difference.

Remember, you're not aiming for perfection. You're building financial security, one deposit at a time. In six months, you'll have made real progress. In a year, you'll have a genuine safety net. And when life throws you an unexpected curve ball, you'll be grateful you did.

Take action now: download your last three months of bank statements, calculate your monthly expenses, and set up your first automatic transfer this week. Your future self will thank you.

Frequently Asked Questions

Sources & References

-

1

Emergency Fund - Saving for When it Matters — www.moneyhub.co.nz

-

2

How to Set Up an Emergency Fund in NZ's Cost-of-Living Climate — info.better.co.nz

-

3

How to build up your emergency savings to cover unexpected costs — sorted.org.nz

-

4

How to Set Up an Emergency Fund — kernelwealth.co.nz