KiwiSaver Contribution Rate: Should You Increase Yours?

Ever wondered if that extra 0.5% from your paycheck could supercharge your retirement dreams? With KiwiSaver contribution rates set to rise to 3.5% from 1 April 2026, many Kiwis are asking: should I i...

Sarah covers personal finance, tax, and KiwiSaver topics for Lifetimes NZ. She focuses on making money management straightforward and practical for everyday Kiwis.

Ever wondered if that extra 0.5% from your paycheck could supercharge your retirement dreams? With KiwiSaver contribution rates set to rise to 3.5% from 1 April 2026, many Kiwis are asking: should I increase my rate now or stick with the default?

Whether you're just starting out or nearing retirement, tweaking your KiwiSaver contribution rate can make a huge difference. This guide breaks it down with the latest 2026 changes, real Kiwi examples, and practical steps to decide if boosting yours is right for you.

Understanding KiwiSaver Contribution Rates in 2026

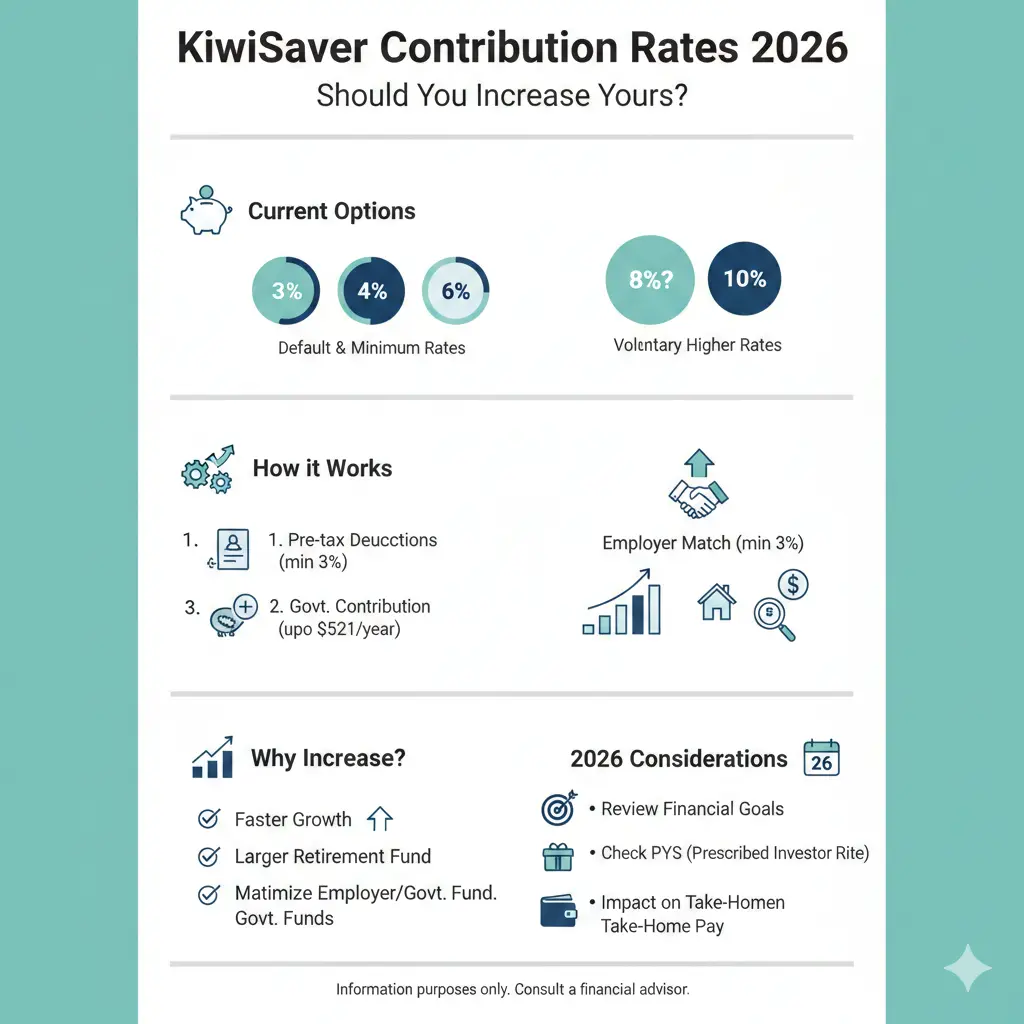

KiwiSaver is our go-to for retirement savings, but the rules are evolving to help us save more. The default rate – that's what happens if you do nothing – is jumping from 3% to 3.5% for both you and your employer starting 1 April 2026, then to 4% in April 2028. This means more money heading into your fund automatically, but it could pinch your weekly budget.

Key Changes Coming Up

- 1 April 2026: Default employee and employer rate rises to 3.5% (from 3%).

- 1 April 2028: Rises again to 4%.

- Temporary relief: Apply via myIR from 1 February 2026 to stay at 3% for up to 12 months if the increase is too much.

- Govvie contribution tweak (from 1 July 2025): Now 25 cents per dollar you put in (down from 50 cents), max $260.72 yearly. No govvie top-up if you earn over $180,000, but 16-17-year-olds now qualify.

These shifts aim to align us closer to global standards – think Australia's 12% or OECD's 15% average – without a big sudden hit.

How Rates Work for Different Folks

| Group | Default Rate (post-1 Apr 2026) | Options |

|---|---|---|

| Employees | 3.5% | 3%, 3.5%, 4%, 6%, 8%, 10% (or apply for temp 3%). |

| Employers | Match your rate (min 3.5%) | Can match lower if you opt for temp reduction, but must hit min when you increase. |

| Self-employed | Your choice | Set auto $24/week for max govvie $260.72. |

| 16-17 year olds | 3.5% (employer from Apr 2026) | Now get govvie contributions. |

Should You Increase Your KiwiSaver Contribution Rate?

Short answer: probably yes, if you can swing it. Here's why, with Kiwi maths to back it up.

The Power of Compounding: Real Kiwi Examples

Let's crunch numbers for a typical Kiwi earner on $60,000 a year. At 3%, that's about $30 a week from you, matched by your boss – $60 total into KiwiSaver weekly.

Bumping to 3.5%? An extra $6/week from you ($180/year), plus employer's match – $420 more yearly. Over 30 years at 5% growth, that could add over $30,000 to your nest egg. (Note: Growth isn't guaranteed; past performance isn't future results.)

"Contributing 4% could see a member’s KiwiSaver savings lasting up to 30% longer."

For higher earners, say $100k: 3.5% is $58/week each from you and employer. If you're already over $180k, skip govvie perks but still get employer match – worth pushing to 6-10% for tax credits on higher contributions.

Pros of Increasing Your Rate

- Free money match: Employer must match at least 3.5%, often more voluntarily.

- Govvie top-up: Contribute $1,042.86 yearly ($20/week) for full $260.72 match.

- Tax perks: Your contributions are from pre-tax pay via PAYE, lowering taxable income.

- Longer retirement funds: Small hikes now mean big wins later.

- Flexibility: Change anytime via KS2 form to your employer or provider.

Cons and When to Hold Off

- Cashflow hit: That 0.5% is $6-10/week – tight if mortgage rates are high or kids' fees loom.

- Temp reduction risk: Stay at 3%, employer might match only 3% too.

- No govvie over $180k: Focus on employer match instead.

- Suspension option: Pause entirely if really strapped (but no contributions or match).

Pro tip: Use IRD's KiwiSaver calculator at ird.govt.nz to model your scenario.

How to Change or Increase Your Contribution Rate

It's straightforward – no excuses!

Step-by-Step for Employees

- Log into myIR: Check your current rate and apply for temp reduction if needed (from 1 Feb 2026).

- Fill KS2 form: Tick your new rate (3.5%, 4%, etc.) and give to employer.

- Show certificate: If reducing, employer needs IRD proof.

- Confirm with provider: Apps like Westpac or Kōura let you track changes instantly.

For Self-Employed or No Employer Match

- Set up auto payments via bank to hit $20/week for max govvie.

- Update in myIR or provider portal.

Employers: Update payroll systems for new rates – tools like Dayforce auto-handle validations.

Factors to Consider Before Boosting Your Rate

Your Age and Timeline

Young gun in your 20s? Crank it to 10% – time is your superpower. Nearing 65? Balance with liquidity for first-home or hardship withdrawals.

Risk Tolerance and Funds

Higher contributions shine in growth funds, but check fees (aim under 0.5%). Diversify if markets wobble.

Life Stage Check

- Buying a home? Contribute min, withdraw at 3-5 years for First Home Grant.

- Family pressures? Temp reduction via IRD, then ramp up.

- High debt? Pay off high-interest first (e.g., credit cards over 15%).

2026 Budget Impact

With inflation cooling but living costs stubborn, model after bills: rent/mortgage 30%, food 15%, then KiwiSaver 4-6%.

Next Steps: Take Control of Your KiwiSaver Today

Don't sleep on this – log into myIR now, run the numbers, and chat with your provider. If affordable, bump to 4-6% for turbocharged savings. Track via the Sorted.org.nz KiwiSaver dashboard for free advice tailored to Kiwis.

Your future self (and maybe that OE in Europe) will thank you. Small changes today build big security tomorrow.

Frequently Asked Questions

Sources & References

-

1

KiwiSaver changes - Inland Revenue — www.ird.govt.nz

-

2

Changes to KiwiSaver contributions - Westpac — www.westpac.co.nz

-

3

KiwiSaver contribution rates are increasing – what does it mean for you - Koura Wealth — www.kourawealth.co.nz

-

4

New Zealand Employee KiwiSaver Contribution Rate Updates - Dayforce — help.dayforce.com

-

5

KiwiSaver Changes in 2026 - proHR — www.prohr.co.nz

-

6

Changes to the KiwiSaver contribution rate - Inland Revenue — www.ird.govt.nz

Related Articles

KiwiSaver 2026: Which Fund is Actually Winning the Performance Race?

If you're tracking your KiwiSaver fund performance in 2026, you might be surprised to learn that the winners aren't always the biggest banks – and the rankings keep shifting. The latest investment sur...

PIR Rates Explained: Are You Paying Too Much Tax on Your KiwiSaver?

Ever checked your KiwiSaver statement and wondered why the tax on your returns seems off? You're not alone—many Kiwis are paying too much (or too little) on their KiwiSaver earnings because of an inco...

KiwiSaver vs Other Investments: Where Should Your Money Go?

Ever wondered if your hard-earned cash is working as hard as it could in KiwiSaver, or if there's a better spot for it elsewhere? With house prices cooling and shares hitting new highs, many Kiwis are...

Best KiwiSaver Providers in NZ 2025: Complete Comparison

Choosing the right KiwiSaver provider can supercharge your retirement savings or first home deposit, especially with government contributions and employer matches adding free money to your account. In...