Mortgage Stress Test: Can You Afford Rate Rises?

Imagine locking in your dream home at rock-bottom rates, only to face a refix that spikes your repayments by $600 a month. For many Kiwis, this isn't a nightmare—it's the reality looming in 2026 as fi...

Sarah covers personal finance, tax, and KiwiSaver topics for Lifetimes NZ. She focuses on making money management straightforward and practical for everyday Kiwis.

Imagine locking in your dream home at rock-bottom rates, only to face a refix that spikes your repayments by $600 a month. For many Kiwis, this isn't a nightmare—it's the reality looming in 2026 as fixed-term mortgages expire.

With the Official Cash Rate (OCR) influencing mortgage rates and banks stress testing at levels up to 6.9%, understanding a mortgage stress test is crucial to see if you can truly afford rate rises. This guide breaks it down for New Zealand homeowners and buyers, with practical steps to safeguard your finances.

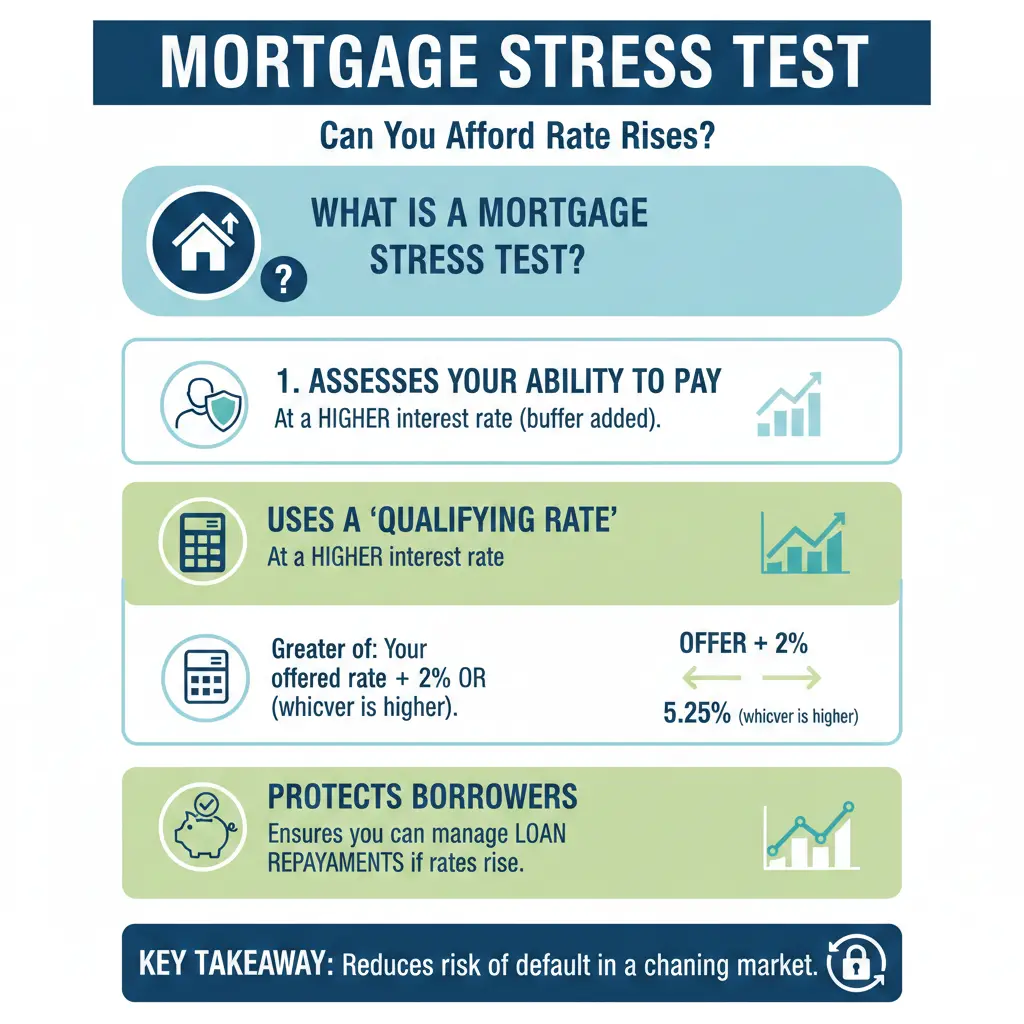

What is a Mortgage Stress Test?

A mortgage stress test checks if you can handle higher interest rates beyond today's advertised deals. Banks use a "servicing test rate"—often 2-2.5% above current rates—to simulate worst-case scenarios. In 2026, these rates range from 6.4% to 6.9% across major lenders, with ANZ recently dropping to 6.7%.

This isn't just for new applicants. Current homeowners should self-stress test before refixing, especially with one-year fixed rates around 7.3% and test rates 1.7% higher. Lenders like those referenced by Opes Partners confirm these figures ensure serviceability even if rates climb further.

Why Banks Use Stress Tests in New Zealand

Reserve Bank rules require banks to verify borrowing capacity amid economic shifts. For low-deposit buyers under LVR restrictions, stress tests raise the bar—ensuring you have "the chops to cover" repayments if things go south. This protects both you and the lender from defaults.

In 2026, with OCR forecasts stabilising but mortgage rates elevated, tests prevent over-borrowing. As Sue Tierney notes, it's like preparing for a typhoon: rates have jumped from under 2.5% to over 5%, and could hit 6% or more.

How Does a Mortgage Stress Test Work?

Banks calculate your repayments using their internal test rate, factoring in income, expenses, debts, and KiwiSaver contributions. They assess debt-to-income (DTI) ratios alongside serviceability—newer metrics gaining traction.

Example calculation: On a $600,000 loan at a 9% test rate (100% lending, interest-only for investors), approval might cap at that amount. Drop to 8.9%, and it rises to $615,000—a $15,000 boost. Further to 8%, you're looking at $682,000.

Impact on Borrowing Power

- A pre-approval for $800,000 could shrink to $760,000 at higher test rates like 8.15%.

- Monthly expenses pegged at $3,000 might jump to $4,000, slashing affordability.

- First-home buyers with smaller deposits face stricter scrutiny, debunking the 20% deposit myth.

Test rates fluctuate: some banks hike, others cut, based on market data. Shop around or use a broker to find the best fit.

Current Servicing Test Rates in New Zealand (2026)

As of early 2026, rates sit between 6.4% and 6.9%. Here's a snapshot:

| Bank | Test Rate | Recent Change |

|---|---|---|

| ANZ | 6.7% | Reduced recently |

| Others (average) | 6.4-6.9% | Varies weekly |

These are higher than one-year fixed rates (~7.3%), creating a buffer. Track via brokers, as banks don't publicise them widely.

Can You Afford Rate Rises? Run Your Own Stress Test

Don't wait for bank rejection—stress test at home. Use online calculators from sites like MoneyHub or Opes Partners, inputting a rate 2% above your current one.

Step-by-Step Guide to Self-Stress Testing

- Gather docs: Payslips, bank statements, expenses (include WINZ payments if applicable).

- Calculate current repayment: Use your loan balance, term, and rate.

- Add buffer: Test at 6.5-7.5% (or lender's rate via broker).

- Factor extras: Rates, insurance, maintenance—aim for repayments under 35-40% of income.

- Adjust scenario: Add job loss buffer (3-6 months expenses).

Real Kiwi example: $800,000 mortgage at 5.5% = ~$4,500/month. At 7.5% test rate: $5,900—$1,400 more. Can your budget stretch?

"A borrower that was pre-approved for $800,000 previously could now have his or her borrowing capacity reduced to $760,000."

Tools and Resources for Kiwis

- Opes Partners calculator for test rates.

- Reserve Bank site for LVR updates: rbnz.govt.nz.

- Kāinga Ora for first-home support, even if low-deposit ineligible.

Strategies to Pass the Stress Test and Handle Rate Rises

Boost your position proactively. Here's how:

For New Buyers

- Pay down "bubblegum debt" (credit cards, Buy Now Pay Later).

- Boost income via side hustles or KiwiSaver withdrawals if eligible.

- Target lenders with lower test rates—brokers compare across panels.

- Leverage First Home Grants or Kāinga Ora packages.

For Current Homeowners Facing Refix

2026 refixes could hike payments $200-$600 monthly due to higher rates, large balances, and longer terms.

- Prepay now: Reduce principal while on low rates.

- Build a repayment fund: Save extra for top-ups.

- Cut non-essentials: Redirect to mock higher repayments.

- Split terms: Fix part short, part long for flexibility.

- Review 6-12 months ahead; consider floating if rates fall.

Interest rate predictions for 2026-2027 suggest OCR stability, but mortgage rates may hover high—plan accordingly.

Risks of Failing the Stress Test

For applicants: Reduced borrowing power cools house prices. For owners: Forced sales or defaults strain families. In 2026's "Goldilocks year" for buyers, low deposits are viable but demand ironclad serviceability.

Pro tip: Stress test quarterly. If tight, consult a broker before refix deadlines.

Next Steps to Secure Your Mortgage

Grab a coffee, pull your statements, and run a stress test today—use the steps above. Contact a licensed broker for personalised rates; many offer free assessments. Track OCR via rbnz.govt.nz and refix 90 days early. Prepay what you can, trim spending, and build that buffer. You're not powerless—smart prep keeps you ahead of rate rises.

Disclaimer: This is general info, not personalised advice. Consult a financial adviser or mortgage broker for your situation. Rates and policies change; verify with lenders.

Frequently Asked Questions

Sources & References

-

1

Why You Need to Stress Test Your Mortgage Now | Sue Tierney — www.stml.co.nz

-

2

Servicing Test Rates in NZ (2026) - Opes Partners — www.opespartners.co.nz

-

3

Why 2026 is a 'Goldilocks year' for first-home buyers | RNZ News — www.rnz.co.nz

-

4

Mortgage Refix Shock NZ 2026 — Payments Could Jump $200–$600 a Month — www.artbeat.org.nz

-

5

The Big Advantage of Falling Bank Test Rates for Homebuyers — www.krispedersen.co.nz

-

6

Refixing in 2026: A Decision Framework (Split, Float, or Fix Longer?) — www.newzealandmortgages.co.nz

-

7

Interest Rate Predictions 2026 & 2027 - MoneyHub NZ — www.moneyhub.co.nz

-

8

Mortgage Outlook for 2026: Rates, OCR & What to Expect — haven.co.nz

-

9

Mortgage Refix Shock NZ 2026 — Payments Could Jump $200... — www.natsquash.co.nz

Related Articles

Industry Bodies and Professional Associations NZ

Whether you're launching a business, advancing your career, or navigating financial regulations, industry bodies and professional associations in New Zealand offer invaluable support. These organisati...

Emergency Benefit NZ: When You Have No Other Options

When you're struggling financially and don't qualify for other benefits, the Emergency Benefit might be your lifeline. It's a discretionary payment designed for Kiwis in genuine hardship who've exhaus...

Unpaid Internships NZ: Are They Legal?

Unpaid internships are a common pathway for students and graduates to gain work experience in New Zealand, but there's often confusion about whether they're actually legal. The short answer is: unpaid...

Estate Administration NZ: Managing Someone's Affairs After Death

Losing a loved one is one of life's toughest challenges, and stepping in to manage their estate can feel overwhelming. In New Zealand, estate administration—the process of handling someone's affairs a...