KiwiSaver Serious Illness Withdrawal: When You Can Access Funds

Imagine facing a diagnosis that turns your world upside down—a serious illness that not only threatens your health but also your financial stability. For Kiwis, KiwiSaver represents long-term security...

The Lifetimes NZ editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes NZ readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Imagine facing a diagnosis that turns your world upside down—a serious illness that not only threatens your health but also your financial stability. For Kiwis, KiwiSaver represents long-term security, locked away until age 65. But when health crises strike, understanding KiwiSaver serious illness withdrawal rules can provide vital relief, allowing access to your savings when you need it most.

This guide breaks down eligibility, the application process, and key considerations under New Zealand law as of 2026. Whether you're dealing with a life-threatening condition or permanent disability, we'll cover everything you need to know to navigate this option effectively.

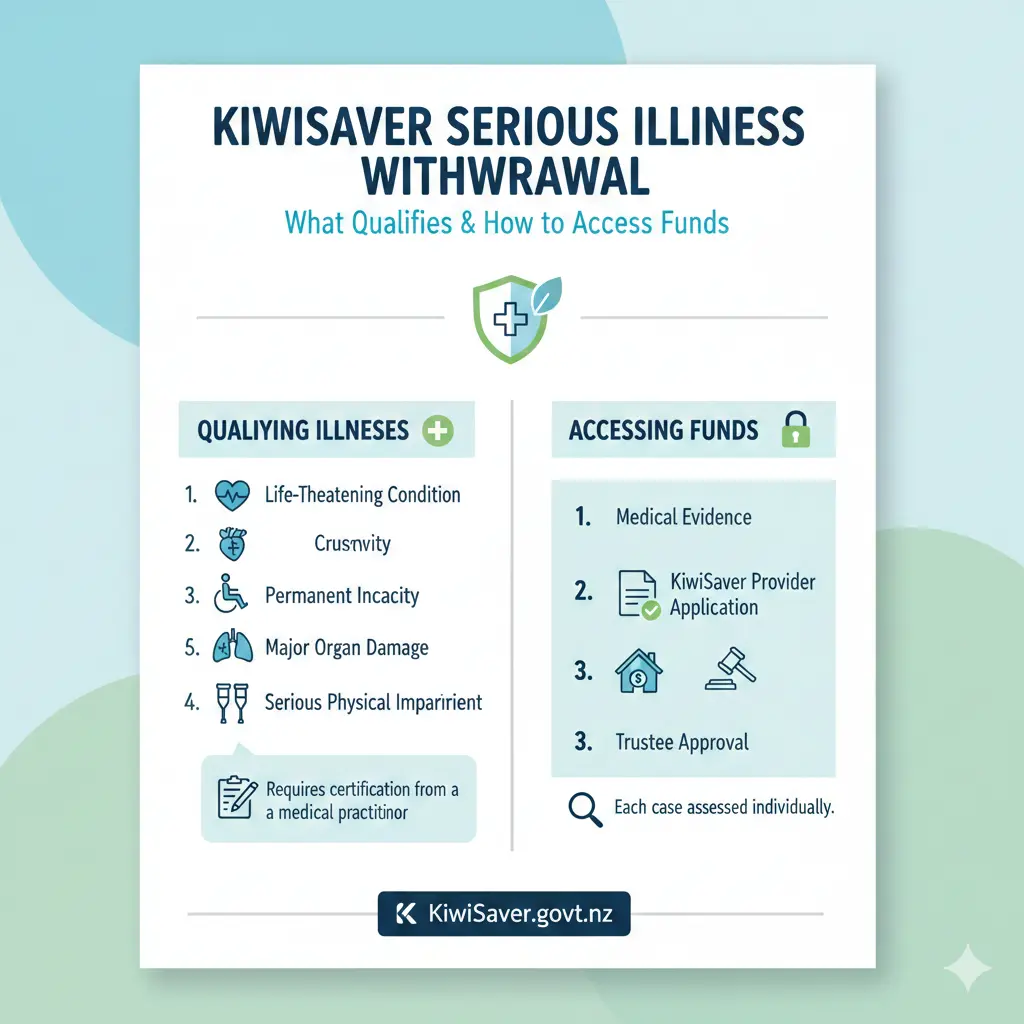

What Qualifies as a Serious Illness for KiwiSaver Withdrawal?

KiwiSaver funds are generally preserved for retirement, but the KiwiSaver Act 2006 allows early access in specific health-related scenarios. A serious illness withdrawal applies if you have an illness, injury, or disability that meets strict criteria set by legislation and reviewed by an independent supervisor.

Key Eligibility Criteria

To qualify, your condition must fall into one of these categories:

- Totally and permanently unable to work in any job suited to your education, skills, training, or experience. This means you can't perform any suitable employment on a long-term basis.

- A condition that poses a serious and imminent risk of death, such as advanced cancer or critical organ failure confirmed by medical evidence.

- A life-shortening congenital condition that reduces your life expectancy below New Zealand Superannuation age (65). Note: This stops future government and employer contributions.

These thresholds are deliberately high to protect retirement savings. For instance, chronic but manageable conditions like early-stage diabetes typically don't qualify unless they lead to total work incapacity. Always consult your doctor for a formal assessment.

How to Apply for KiwiSaver Serious Illness Withdrawal

The process varies based on your membership duration and condition type. Inland Revenue (IRD) oversees rules, but applications go through your provider or IRD depending on circumstances.

Step-by-Step Application Guide

- Determine your eligibility timeline: If within your first 2 months of membership, apply directly to IRD. For longer members, contact your KiwiSaver provider (e.g., Generate, AMP, or NZ Funds).

- Gather medical evidence: Your health practitioner must complete a Declaration of Serious Illness (included in provider forms). Attach a medical certificate; supervisors may request more details.

- Complete required forms: Fill out the Serious Illness Withdrawal Application, including a statutory declaration witnessed by an authorised person. Provide certified ID, proof of address, and bank details.

- Submit to your provider or IRD: For life-shortening congenital conditions, your provider handles submission to the supervisor.

- Await supervisor review: An independent supervisor decides based on KiwiSaver Act criteria. Approval isn't guaranteed.

If approved, you can withdraw some or all funds, including your contributions, employer matches, government contributions ($521 annual max in 2026), $1,000 kick-start (if received), fee subsidies, and investment returns. Processing typically takes 10-15 working days.

Savings Suspension Option

If facing serious illness, you can also suspend contributions from salary or wages to ease immediate pressure. Apply within the first 12 months of membership if hardship is likely. This pauses deductions but preserves existing funds.

What Funds Can You Access?

Upon approval, KiwiSaver serious illness withdrawals are comprehensive:

| Withdrawable Components | Details |

|---|---|

| Your contributions | All personal pre-tax and after-tax amounts |

| Employer contributions | Minimum 3% matches |

| Government contributions | Up to $521/year (2026 rate), including kick-start |

| Investment returns & subsidies | Interest, growth, and fee credits |

Unlike hardship withdrawals, serious illness allows full access, not just member/employer portions. However, for congenital conditions, future contributions cease.

Serious Illness vs. Significant Financial Hardship Withdrawals

Don't confuse serious illness with financial hardship—though illness can trigger both. Hardship applies to situations like unpaid bills, rent arrears, or medical costs for you/dependants, but limits withdrawals to member/employer contributions (no government funds).

Quick Comparison

| Aspect | Serious Illness | Financial Hardship |

|---|---|---|

| Eligible Conditions | Total incapacity, imminent death risk, congenital life-shortening | Essential living costs, medical/funeral for dependants |

| Withdrawable Funds | All (including govt) | Member + employer only |

| Evidence Needed | Medical declaration + certificate | Statutory declaration + proof of hardship |

| Approval Body | Provider supervisor | Provider + supervisor |

Choose based on your situation—many with serious illness qualify for both.

Real-Life Example: James's Story

James, a 42-year-old builder from Auckland, was diagnosed with aggressive cancer posing an imminent risk of death. Unable to work, he applied for a serious illness withdrawal through his provider. With his doctor's declaration, approval came swiftly, releasing $85,000—including government contributions—to cover treatments and home modifications.

"Without this access, we'd have lost our home. It bought us time for recovery." — James (adapted from case study)

Tax Implications and Long-Term Effects

Withdrawals are generally tax-free on growth if rules are followed, but PIE tax rates apply to earnings (10.5%-28% based on balance). Withdrawing reduces compounding—$10,000 at 5% annual return could grow to $26,533 in 20 years. Future employer/government contributions stop for congenital cases.

IRD tracks withdrawals via myIR; report any income effects for Working for Families or benefits.

Alternatives to Protect Your KiwiSaver

Before withdrawing, explore these Kiwi options:

- Health and life insurance: Covers treatments, surgeries, and lump sums for critical illness, preserving KiwiSaver growth.

- Income protection: Replaces salary (up to 75%) during incapacity; some continue KiwiSaver contributions.

- ACC support: Covers injury-related costs; check entitlements via acc.co.nz.

- WINZ benefits: Sickness Benefit or Supported Living Payment for low-income illness.

- Hardship withdrawal: If illness causes bills but not full incapacity.

Insurance Benefits Table

| Insurance Type | Key Protection | KiwiSaver Impact |

|---|---|---|

| Health | Private treatment, cancer drugs | Reduces withdrawal need |

| Trauma/Life | Lump sum for serious illness | Buffers expenses, keeps funds invested |

| Income Protection | Monthly income replacement | Maintains contributions during illness |

James's insurer covered treatments and contributions, avoiding KiwiSaver dip.

Common Mistakes to Avoid

- Applying without full medical evidence—leads to rejection.

- Ignoring alternatives like insurance or WINZ.

- Not suspending contributions early to prevent over-deduction.

- Assuming all illnesses qualify—criteria are strict.

Frequently Asked Questions

Related Articles

Working Multiple Jobs NZ: Tax and Legal Considerations

Juggling multiple jobs can boost your income, but it's crucial to understand the tax implications and legal requirements that come with working more than one role in Aotearoa. Whether you're a contrac...

Name Changes NZ: Legal Process and Costs

Considering a fresh start with a new name? Whether it's after marriage, divorce, or simply embracing a personal transformation, changing your name in New Zealand is straightforward but requires follow...

Holiday Home Tax Rules NZ: Private Use and Rental

Own a bach in Coromandel or a holiday home in Queenstown? You're not alone—many Kiwis cherish these escapes, but renting them out while enjoying personal use can trip you up on tax rules. Getting the...

Industry Bodies and Professional Associations NZ

Whether you're launching a business, advancing your career, or navigating financial regulations, industry bodies and professional associations in New Zealand offer invaluable support. These organisati...