How to Choose the Right KiwiSaver Fund for Your Age

Choosing the right KiwiSaver fund is one of the most important financial decisions you'll make for your retirement. Your age, time horizon, and risk tolerance should guide your choice, but with 370 fu...

Sarah covers personal finance, tax, and KiwiSaver topics for Lifetimes NZ. She focuses on making money management straightforward and practical for everyday Kiwis.

Choosing the right KiwiSaver fund is one of the most important financial decisions you'll make for your retirement. Your age, time horizon, and risk tolerance should guide your choice, but with 370 funds across 29 providers, it's easy to feel overwhelmed. This guide will help you navigate the options and find a fund that actually works for your life stage.

Understanding KiwiSaver Fund Types

KiwiSaver funds are grouped by risk level, and understanding these categories is essential to making the right choice. The main fund types are:

- Conservative funds – Focus on income assets (typically 80% income, 20% growth). Best for short-term horizons (3+ years) and those nearing retirement.

- Balanced funds – Mix of income and growth assets (usually 40-60% growth). Suited to medium-term investors seeking moderate returns.

- Growth funds – Emphasise growth assets (typically 70-80% growth). Designed for longer time horizons with higher volatility tolerance.

- Aggressive funds – Maximum growth focus with highest volatility. For investors 10+ years from retirement.

- Default funds – A middle-ground option that automatically adjusts as you age.

The key difference? Conservative funds prioritise stability, while growth funds prioritise long-term capital growth. Your age should heavily influence which category suits you best.

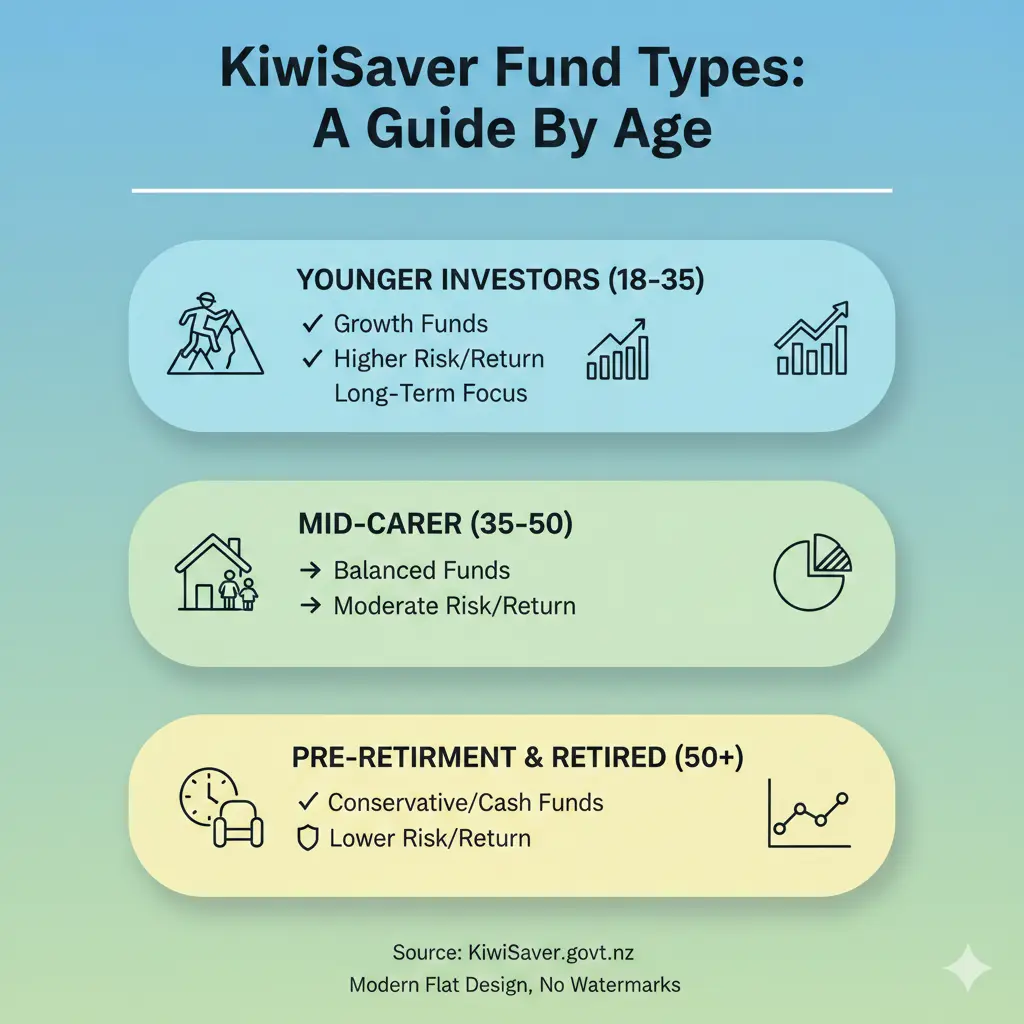

Age-Based KiwiSaver Strategy

Your 20s and 30s: Time to Take Risk

If you're in your 20s or 30s, you've got 30+ years until retirement—your greatest asset is time. This means you can weather market volatility and benefit from compound growth. Growth and aggressive funds are typically ideal at this life stage.

Consider the performance data: the Westpac KiwiSaver Growth Fund delivered 12.8% returns over the past year, while the Generate Focused Growth Fund achieved 15.0%. Over a 10-year period, growth funds have averaged 7-10% annual returns. That compounding effect is powerful when you've got decades to invest.

The trade-off? Your balance will fluctuate. A growth fund might drop 15-20% in a market downturn, but historically recovers within 2-3 years. If you're not touching the money for 30 years, that volatility shouldn't worry you.

Your 40s: Maintain Growth, Watch Risk

By your 40s, you're likely earning more and contributing more to KiwiSaver. You still have 20+ years to retirement, so growth funds remain appropriate. However, this is a good time to assess whether you're on track for your retirement goals.

Many investors in this bracket stay in growth funds but might consider a balanced fund if they're uncomfortable with market swings. Balanced funds like the ASB Balanced Fund (which targets 58% growth assets) offer a middle ground, delivering 11.8% returns over the past year with less volatility than pure growth funds.

This is also the stage where you should review your fund's fees. The average KiwiSaver management fee is 0.88% per year, but some funds charge significantly less. Over 20 years, a difference of 0.5% in fees can cost you tens of thousands of dollars in lost returns.

Your 50s: Gradual Shift Towards Stability

As you enter your 50s with 10-15 years until retirement, it's time to think about de-risking gradually. Many investors switch to a balanced fund or start considering conservative options. This isn't about abandoning growth—it's about reducing your exposure to severe market downturns close to retirement.

A balanced fund targeting 40-60% growth assets still provides reasonable returns while offering more stability. The ASB Balanced Fund, for example, achieved 6.7% net returns over 10 years, which is solid for a mid-risk option.

Some KiwiSaver providers offer lifecycle or "default" funds that automatically shift from growth to conservative as you approach retirement age. These can be a hands-off solution if you prefer not to manage the transition yourself.

Within 5 Years of Retirement: Conservative Focus

Once you're within 5 years of your target retirement date, conservative funds become more appropriate. These funds prioritise capital preservation over growth, typically holding 80% income assets and 20% growth assets.

The ASB KiwiSaver Conservative Fund, for example, delivered 6.8% returns over the past year with significantly less volatility than growth funds. While the returns are lower, the stability matters when you're about to start withdrawing.

That said, you'll likely still live 30+ years in retirement, so maintaining some growth exposure (20-30%) is still wise to protect against inflation.

Key Factors Beyond Your Age

Your Risk Tolerance

Age is a guide, not a rule. If you're in your 30s but uncomfortable watching your balance drop 15% in a market downturn, a balanced fund might suit you better than a pure growth fund. Conversely, if you're 50 and comfortable with volatility, growth funds can still work.

Ask yourself: Could I stay invested during a 20% market drop, or would I panic and switch funds? Your honest answer matters more than any age-based formula.

Your Time Horizon

Time horizon isn't just about age—it's about when you actually need the money. If you're planning to buy a first home in 5 years, a conservative or balanced fund makes sense, regardless of your age. If you're 55 but won't touch KiwiSaver until 65, growth funds are still appropriate.

Your Contribution Level

KiwiSaver members contribute between 3% and 10% of gross earnings. If you're maximising contributions at 10%, you might be more comfortable with growth funds because you're building a larger nest egg. If you're at the minimum 3%, you might need slightly higher returns, again pointing toward growth funds earlier in your career.

Fees and Performance

With 370 KiwiSaver funds available, comparing fees and performance is crucial. The lowest-cost funds charge as little as 0.03% per year, while others charge significantly more. Over 30 years, this difference compounds dramatically.

Look at net returns (after fees and tax), not gross returns. The ANZ KiwiSaver Growth Fund, New Zealand's most popular fund with 230,946 members, delivered 10.3% net returns over the past year and 7.1% over 10 years. Compare this against similar funds to ensure you're not paying for underperformance.

Top KiwiSaver Funds by Popularity (2026)

Here are the most popular funds, which might give you a starting point for comparison:

- ANZ KiwiSaver Growth Fund – 230,946 members, 10.3% past-year return, 7.1% 10-year return

- ASB KiwiSaver Growth Fund – Large membership base with solid growth focus

- Westpac KiwiSaver Conservative Fund – 145,082 members for stable, lower-risk investing

- Westpac KiwiSaver Growth Fund – 119,814 members, 12.8% past-year return, 7.4% 10-year return

- Fisher Funds KiwiSaver Growth Fund – 117,798 members, 8.1% 10-year return

Popular doesn't always mean best for you, but these funds have proven track records and transparent fee structures.

How to Actually Choose Your Fund

Here's a practical process:

- Determine your age and retirement timeline. Use the age-based guidelines above as your starting point.

- Assess your risk tolerance honestly. Can you handle volatility, or do you need stability?

- Use comparison tools. The Inland Revenue's Sorted platform has a KiwiSaver fund finder that lets you compare funds side-by-side. KiwiSaver comparison websites like kiwisavercomparison.co.nz also provide real-time data.

- Compare fees and net returns. Look at returns after fees and tax, not gross returns.

- Check your provider's fund options. Most major banks (ANZ, ASB, BNZ, Westpac) and independent providers offer multiple funds.

- Make a decision and review annually. You don't need to switch constantly, but reviewing your fund choice once a year ensures it still suits your circumstances.

Next Steps

Choosing the right KiwiSaver fund isn't complicated once you understand the basics. Start by identifying your age bracket and time horizon, then use that to guide your fund selection. Use free comparison tools like Sorted's KiwiSaver fund finder or kiwisavercomparison.co.nz to compare specific funds in your chosen category. Pay attention to fees—they matter more than you might think over 30+ years.

Remember, the best KiwiSaver fund is one you'll stay invested in. Market volatility is normal, and switching funds in a panic often locks in losses. Choose thoughtfully, review annually, and let compound growth do the heavy lifting.

If you're unsure, many KiwiSaver providers offer free guidance. Don't hesitate to contact your provider or use the Inland Revenue's resources to get clarity before making your choice.

Frequently Asked Questions

Sources & References

-

1

Compare All 200+ KiwiSaver Funds | Free NZ Comparison Tool 2026 — kiwisavercomparison.co.nz

-

2

New Zealand's Top 10 KiwiSaver Funds — www.canstar.co.nz

-

3

Choosing a KiwiSaver fund — www.ird.govt.nz

Related Articles

KiwiSaver 2026: Which Fund is Actually Winning the Performance Race?

If you're tracking your KiwiSaver fund performance in 2026, you might be surprised to learn that the winners aren't always the biggest banks – and the rankings keep shifting. The latest investment sur...

PIR Rates Explained: Are You Paying Too Much Tax on Your KiwiSaver?

Ever checked your KiwiSaver statement and wondered why the tax on your returns seems off? You're not alone—many Kiwis are paying too much (or too little) on their KiwiSaver earnings because of an inco...

KiwiSaver vs Other Investments: Where Should Your Money Go?

Ever wondered if your hard-earned cash is working as hard as it could in KiwiSaver, or if there's a better spot for it elsewhere? With house prices cooling and shares hitting new highs, many Kiwis are...

Best KiwiSaver Providers in NZ 2025: Complete Comparison

Choosing the right KiwiSaver provider can supercharge your retirement savings or first home deposit, especially with government contributions and employer matches adding free money to your account. In...