Rental Income Tax NZ: What Landlords Must Know

Owning a rental property in New Zealand can be a smart way to build wealth, but getting the tax side right is crucial to avoid nasty surprises from IRD. With rental income tax rules evolving—especiall...

Sarah covers personal finance, tax, and KiwiSaver topics for Lifetimes NZ. She focuses on making money management straightforward and practical for everyday Kiwis.

Owning a rental property in New Zealand can be a smart way to build wealth, but getting the tax side right is crucial to avoid nasty surprises from IRD. With rental income tax rules evolving—especially around interest deductibility and bright-line tests—Kiwi landlords need to stay sharp on what counts as taxable income, what deductions you can claim, and how to report it all correctly for the 2026 tax year.

This guide breaks down everything you need to know about rental income tax NZ, from calculating your taxable profit to special rules for residential properties. We'll cover practical examples, current rates, and tips to maximise your deductions while keeping compliant.

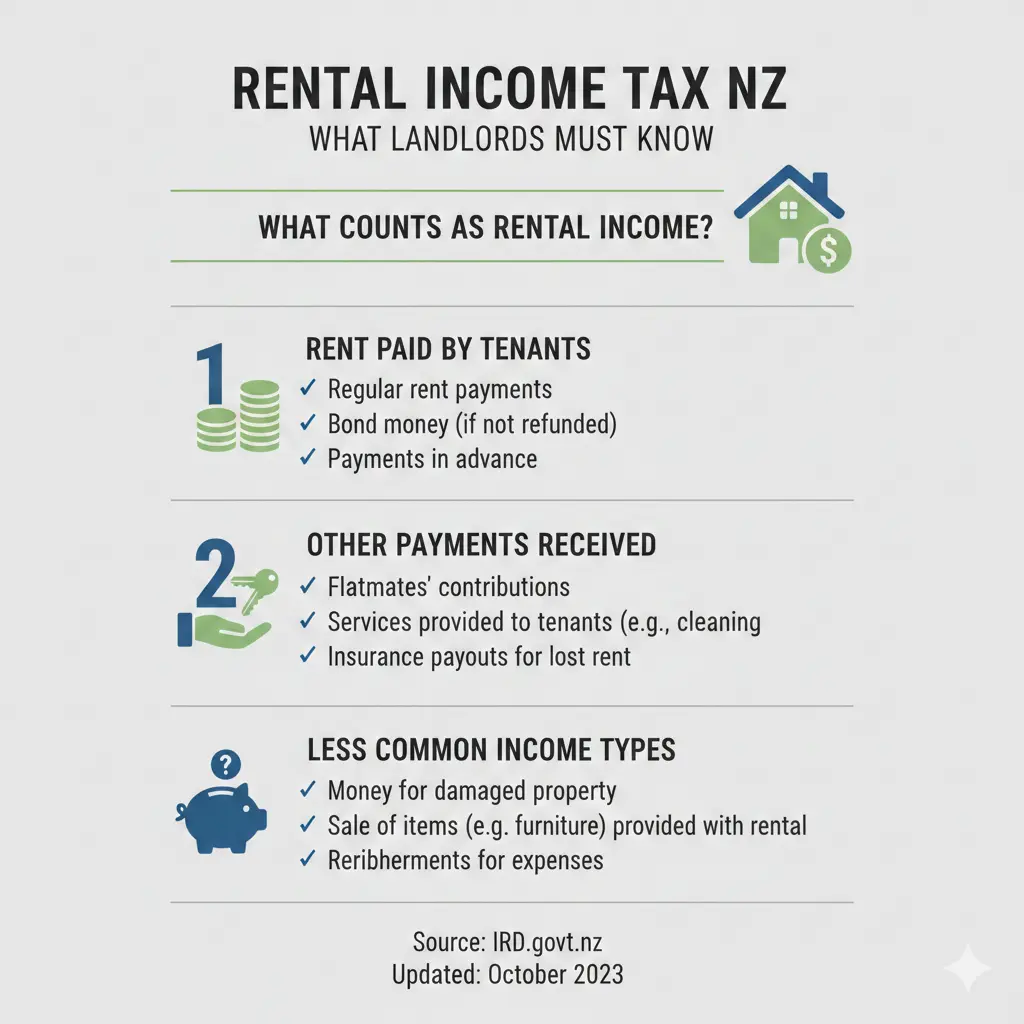

What Counts as Rental Income?

Rental income includes all money you receive from tenants, whether weekly rent, bond payments (if not refunded), or one-off fees like letting agent commissions passed on to you. IRD treats this as taxable income, just like your salary or wages.

Common types of rental income:

- Fixed weekly or monthly rent payments.

- Payments for furnishings, utilities, or cleaning if bundled into rent.

- Insurance payouts for lost rent (taxable portion).

- Overseas rental income if you're a NZ tax resident.

Don't forget: if you live in part of the property (like a granny flat), you only declare the portion rented out. For example, if you rent out a sleep-out for $200/week while living in the main house, that's fully taxable rental income.

Bright-Line Test: When Rental Profits Become Taxable

The bright-line test taxes gains on residential properties sold within a set period. For properties acquired after 27 March 2021, it's 10 years—but watch for changes. If you sell within the bright-line period and it's not your main home, the profit is taxed at your personal income tax rate.

Tip: Keep records of purchase and sale dates, plus any improvements, to calculate your gain accurately.

Deductible Expenses: What You Can Claim

The good news? You don't pay tax on gross rent—only on profit after deductions. Legitimate expenses reduce your taxable income, potentially dropping you into a lower tax bracket.

Key deductible expenses for 2026:

- Interest on loans for properties bought before 27 March 2021 (now 100% deductible in 2026, up from 80% in 2025).

- Rates, insurance, and maintenance repairs (but not capital improvements like a new roof).

- Property management fees and legal costs for tenancy agreements.

- Travel to inspect the property (km logs required).

- Depreciation on buildings (phasing out for some assets) and chattels like appliances.

Interest Deductibility Rules Explained

For rentals bought after 27 March 2021, interest deductibility phased in slowly, but pre-2021 properties are fully deductible again in 2026. Say your annual rent is $52,000, loan interest $30,000, and other expenses $10,000—your taxable profit is just $12,000.

Actionable tip: Use IRD's rental expenses checklist to ensure you're claiming everything. Track costs with apps like Xero or Splithire for easy myIR uploads.

Tax Rates on Rental Income for 2026

Rental profit adds to your total income and is taxed at progressive personal rates. For the 2025/26 tax year (1 April 2025 onwards), here's the scale:

| For each dollar of income | Tax rate |

|---|---|

| 0 - $15,600 | 10.5% |

| $15,601 - $53,500 | 17.5% |

| $53,501 - $78,100 | 30% |

| $78,101 - $180,000 | 33% |

| $180,001 and over | 39% |

Example calculation: Sarah earns $60,000 salary plus $20,000 rental profit (total $80,000). Tax on salary up to $78,100, then 33% on the extra $1,900. Use IRD's tax calculator for precision.

Bright-Line Extension and Other Investor Rates

Resident individual investors may qualify for lower rates like 10.5% or 17.5% on certain income if thresholds are met (e.g., total income under $78,100). Trusts and companies face 28-39%—seek advice.

ACC levies apply too: 1.67% on earnings up to $2,551.59 for 2025/26.

How to Report Rental Income to IRD

Declare via myIR annually by 7 July (or 31 March with an agent). Use the IRD rental income/expense worksheet (IR1100) or property schedule.

- Gather bank statements, invoices, and loan docs.

- Calculate profit: Income minus deductions.

- Enter in your tax return—IRD pre-fills some data if linked.

- Pay any owing tax, or claim overpaid refunds.

New for 2026: Enhanced digital tracking means better pre-fills, but double-check for accuracy. Non-residents use RWT at 28% unless approved.

Record-Keeping Essentials

Keep records for 7 years: receipts, contracts, km logs. Digital tools like Receipt Bank integrate with myIR seamlessly.

Special Rules for Kiwi Landlords

Residential vs Commercial Rentals

Residential follows bright-line; commercial doesn't. Mixed-use? Apportion fairly.

Losses and Ring-Fencing

Rental losses can't offset other income anymore—they're ring-fenced against future rental profits. Carry forward indefinitely.

KiwiSaver and Rentals

Rental income doesn't affect contributions, but profits can boost withdrawals. Link to IRD for auto-adjustments.

Practical Tips to Minimise Your Tax Bill

- Time repairs before year-end for deductions.

- Consider a look-through company (LTC) for high earners—taxed at shareholder rates.

- Claim home office if managing rentals from home (pro-rata space).

- Watch GST: Register if turnover over $60,000 (rentals usually exempt).

- Prepay expenses before 31 March.

"Funds borrowed before 27 March 2021 on rental properties are now 100% deductible for the 2026 year." Evans & Co Accountants

Next Steps for Kiwi Landlords

Review your 2026 projections now—grab IRD's rental calculator, tally expenses, and simulate tax. If properties exceed three or income's complex, book a tax advisor via ird.govt.nz. Remember, this isn't personalised advice—consult a professional for your situation. Stay compliant, claim smart, and keep more profit in your pocket.

Disclaimer: Tax rules change; seek independent advice from a chartered accountant or IRD. Rates current as of 2026 tax year.

Frequently Asked Questions

Sources & References

-

1

New Zealand Tax Facts - Baker Tilly Staples Rodway — bakertillysr.nz

-

2

New Zealand PAYE Tax Rates 2025 & 2026 - MoneyHub NZ — www.moneyhub.co.nz

-

3

Tax rates for individuals - Inland Revenue — www.ird.govt.nz

-

4

Key Tax Changes | Evans & Co Accountants & Advisors — www.evansaccountants.co.nz

-

5

Expatriate tax - New Zealand - Grant Thornton International — www.grantthornton.global

-

6

New Zealand - Individual - Income determination — taxsummaries.pwc.com

- 7

Useful Tools

Related Articles

Industry Bodies and Professional Associations NZ

Whether you're launching a business, advancing your career, or navigating financial regulations, industry bodies and professional associations in New Zealand offer invaluable support. These organisati...

Emergency Benefit NZ: When You Have No Other Options

When you're struggling financially and don't qualify for other benefits, the Emergency Benefit might be your lifeline. It's a discretionary payment designed for Kiwis in genuine hardship who've exhaus...

Unpaid Internships NZ: Are They Legal?

Unpaid internships are a common pathway for students and graduates to gain work experience in New Zealand, but there's often confusion about whether they're actually legal. The short answer is: unpaid...

Estate Administration NZ: Managing Someone's Affairs After Death

Losing a loved one is one of life's toughest challenges, and stepping in to manage their estate can feel overwhelming. In New Zealand, estate administration—the process of handling someone's affairs a...