New Zealand's Debt-to-Income Ratio Lending Rules Explained

If you're thinking about buying a home in New Zealand, you've probably heard lenders mention your debt-to-income (DTI) ratio. This number plays a crucial role in whether you'll get approved for a mort...

James writes about the New Zealand property market, renting, home ownership, and housing costs. He breaks down complex property topics into practical advice for renters and buyers.

If you're thinking about buying a home in New Zealand, you've probably heard lenders mention your debt-to-income (DTI) ratio. This number plays a crucial role in whether you'll get approved for a mortgage and how much you can borrow. Since new DTI lending rules came into effect on 1 July 2024, understanding how they work has become even more important for anyone applying for a home loan.

What Is a Debt-to-Income Ratio?

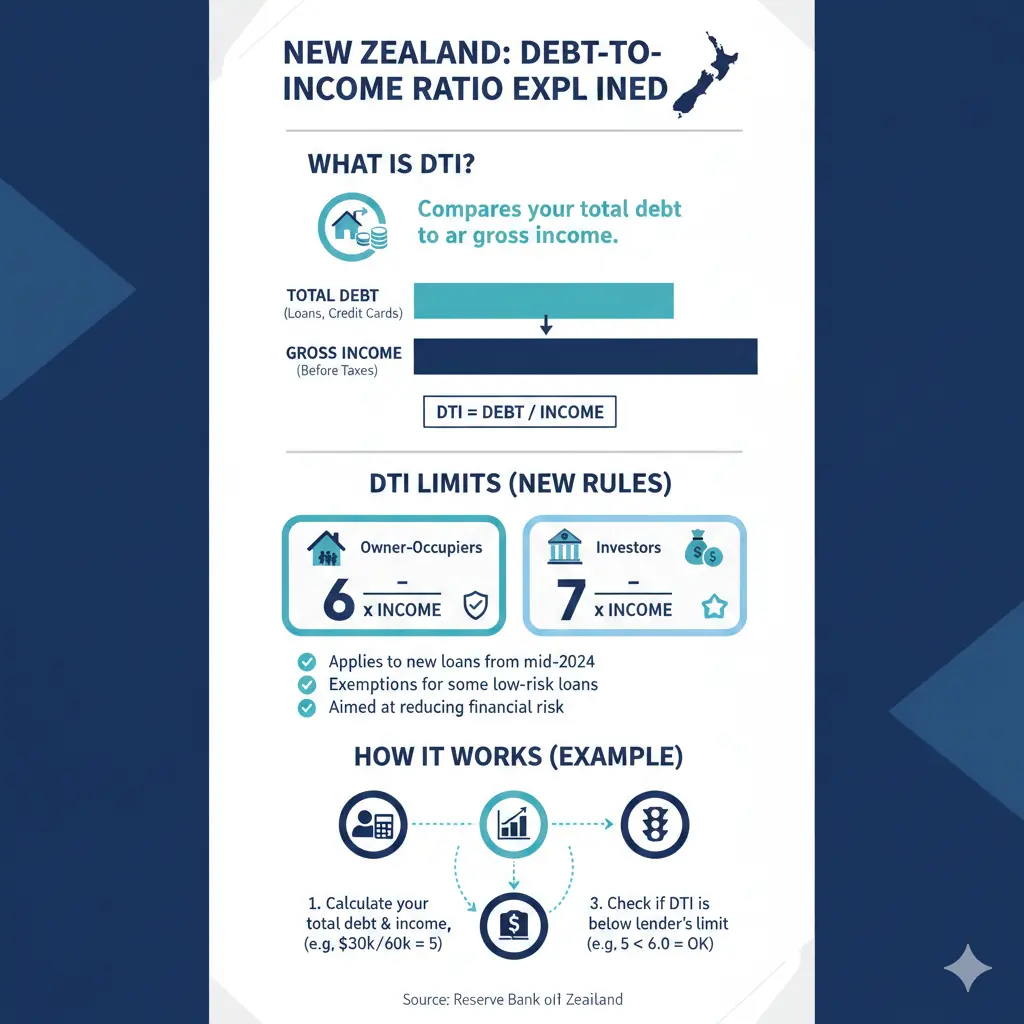

Your DTI ratio is a straightforward calculation that shows how much debt you have compared to your annual income. It's expressed as a simple number that tells lenders how many times your total debt is relative to your gross income.

Here's how it works: if you have total debt of $500,000 and earn $80,000 per year, your DTI ratio is 6.25. This means your debt is 6.25 times your annual gross income.

Banks use this metric because it gives them a quick snapshot of your financial health and your ability to repay a loan. The lower your DTI ratio, the less risky you appear as a borrower.

How to Calculate Your DTI Ratio

Calculating your DTI ratio takes just a few steps. You'll need to gather information about your debts and your income, then divide one by the other.

Step 1: Add Up Your Total Debt

Your total debt includes:

- Your existing mortgage or home loan

- Car loans

- Credit card balances

- Personal loans

- Student loans

- Any other outstanding debts

- The limits on credit cards and overdrafts (not just what you've used)

- Any new loans you're applying for

Step 2: Calculate Your Gross Income

Your gross income is what you earn before taxes and deductions. This includes:

- Your annual salary or wages

- Rental income (if you own investment properties)

- Self-employment income

- Other income sources

Step 3: Do the Maths

The formula is simple:

DTI ratio = Total debt ÷ Gross income

For example, if you have $550,000 in total debt and earn $80,000 per year, your DTI ratio would be 6.875.

New Zealand's DTI Lending Rules (2024 Onwards)

On 1 July 2024, the Reserve Bank of New Zealand (RBNZ) introduced new DTI restrictions for residential lending. These rules apply to both owner-occupiers (people buying a home to live in) and investors (people buying rental properties).

What Are the New Limits?

The RBNZ set "speed limits" on how much high-DTI lending banks can do:

- Owner-occupiers: You'll generally need a DTI ratio of 6 or lower. However, banks can lend to 20% of new owner-occupier borrowers with a DTI ratio over 6.

- Investors: You'll generally need a DTI ratio of 7 or lower. Banks can lend to 20% of new investor borrowers with a DTI ratio over 7.

In practical terms, this means banks can approve some mortgages with higher DTI ratios, but they're limited in how many they can hand out. If you have a DTI ratio above these thresholds, you're not automatically rejected—you just fall into the "high-DTI" category, and your bank may have limited capacity to approve your application depending on how many other high-DTI loans they've already issued.

Why Did the RBNZ Introduce These Rules?

The DTI restrictions work alongside loan-to-value (LVR) restrictions to help protect New Zealand's financial stability. By limiting how much debt banks can take on relative to borrowers' incomes, the RBNZ aims to reduce the likelihood of a future housing-related downturn.

What Factors Do Lenders Consider Beyond DTI?

While your DTI ratio is important, it's not the only thing lenders look at. Banks will also consider:

- Your credit history and credit score

- Your employment history and job stability

- Your deposit size and assets

- The type of property you're buying

- Your overall financial situation

The good news is that a high DTI ratio doesn't automatically mean rejection. If you have a strong income, a solid credit history, or significant assets, these factors can help offset a higher DTI ratio.

Practical Tips for Improving Your DTI Ratio

If your DTI ratio is higher than ideal, here are some strategies to improve it before applying for a mortgage:

Reduce Your Debt

Pay down credit cards, car loans, and personal loans before applying. Even reducing your debt by $20,000–$30,000 can noticeably improve your ratio.

Increase Your Income

If you've recently received a pay rise or taken on additional income, this can help. Make sure you have documentation showing this income is stable and ongoing.

Avoid Taking on New Debt

Don't apply for new credit cards, car loans, or personal loans in the months before your mortgage application. Each new debt application can hurt your DTI ratio.

Talk to a Mortgage Broker

A mortgage broker can help you understand your DTI ratio, identify which lenders might be willing to work with you, and advise you on the best strategy for your situation.

DTI Ratios vs. Other Lending Criteria

New Zealand's DTI limits sit in the middle compared to other countries. Australia recently introduced similar rules (effective February 2026) with a 6 times income limit, while Ireland and Canada have much stricter limits of 3.5–4.5 times income. This means New Zealand's approach allows for more borrowing relative to income than some other countries.

Next Steps: Getting Ready to Apply

If you're thinking about applying for a mortgage, here's what you should do:

- Calculate your current DTI ratio using the formula above

- If your ratio is higher than 6 (or 7 if you're an investor), consider whether you can reduce debt or increase income before applying

- Check your credit report and fix any errors

- Gather documentation showing your income (payslips, tax returns, etc.)

- Talk to a mortgage broker who can help you navigate the process and explain how the DTI rules might affect your specific situation

Understanding your DTI ratio puts you in control of your mortgage application. By knowing where you stand and what lenders are looking for, you can make informed decisions about your home-buying journey. Remember, DTI is just one piece of the puzzle—your overall financial health, credit history, and personal circumstances all matter too.

Frequently Asked Questions

Sources & References

-

1

Debt to Income Ratios Explained — www.moneyhub.co.nz

-

2

Understanding debt-to-income ratios — www.kiwibank.co.nz

-

3

Here's what new debt-to-income home loan caps mean for banks and borrowers — executivewp.com.au

-

4

DTI Rules Explained: What They Mean for NZ First-Home Buyers — www.newzealandmortgages.co.nz

-

5

APRA's New 2026 Debt-to-Income Rules — www.camdenprofessionals.com.au

Useful Tools

Related Articles

First Home Grant NZ: How to Get Up to $10000

Buying your first home is one of the biggest financial decisions you'll make, and the New Zealand government wants to help. The First Home Grant puts up to $10,000 directly towards your deposit, makin...

Why 2026 is the Hardest Year to Buy a Home (and How to Beat the Odds)

Imagine standing at the edge of the property ladder in 2026, eyeing your dream home while prices hover stubbornly high, listings pile up, and buyer confidence wavers. For Kiwis, this year feels toughe...

Buying Your First Home in 2026: A Step-by-Step NZ Checklist

Imagine standing in your own Kiwi bach or cosy family home, keys in hand, after years of renting. In 2026, with interest rates stabilising and first-home schemes still strong, buying your first home i...

Selling Your Home? 10 Low-Cost Renovations That Add $50k in Value

If you're planning to sell your home in New Zealand, you don't need to break the bank with a complete renovation to attract buyers and boost your sale price. The good news? Some of the most effective...