Buying Your First Home in 2026: A Step-by-Step NZ Checklist

Imagine standing in your own Kiwi bach or cosy family home, keys in hand, after years of renting. In 2026, with interest rates stabilising and first-home schemes still strong, buying your first home i...

James writes about the New Zealand property market, renting, home ownership, and housing costs. He breaks down complex property topics into practical advice for renters and buyers.

Imagine standing in your own Kiwi bach or cosy family home, keys in hand, after years of renting. In 2026, with interest rates stabilising and first-home schemes still strong, buying your first home in New Zealand is more achievable than you might think—but it takes a solid plan. This step-by-step checklist breaks it down into practical actions tailored for Kiwis, from budgeting to settlement, so you can navigate the process with confidence.

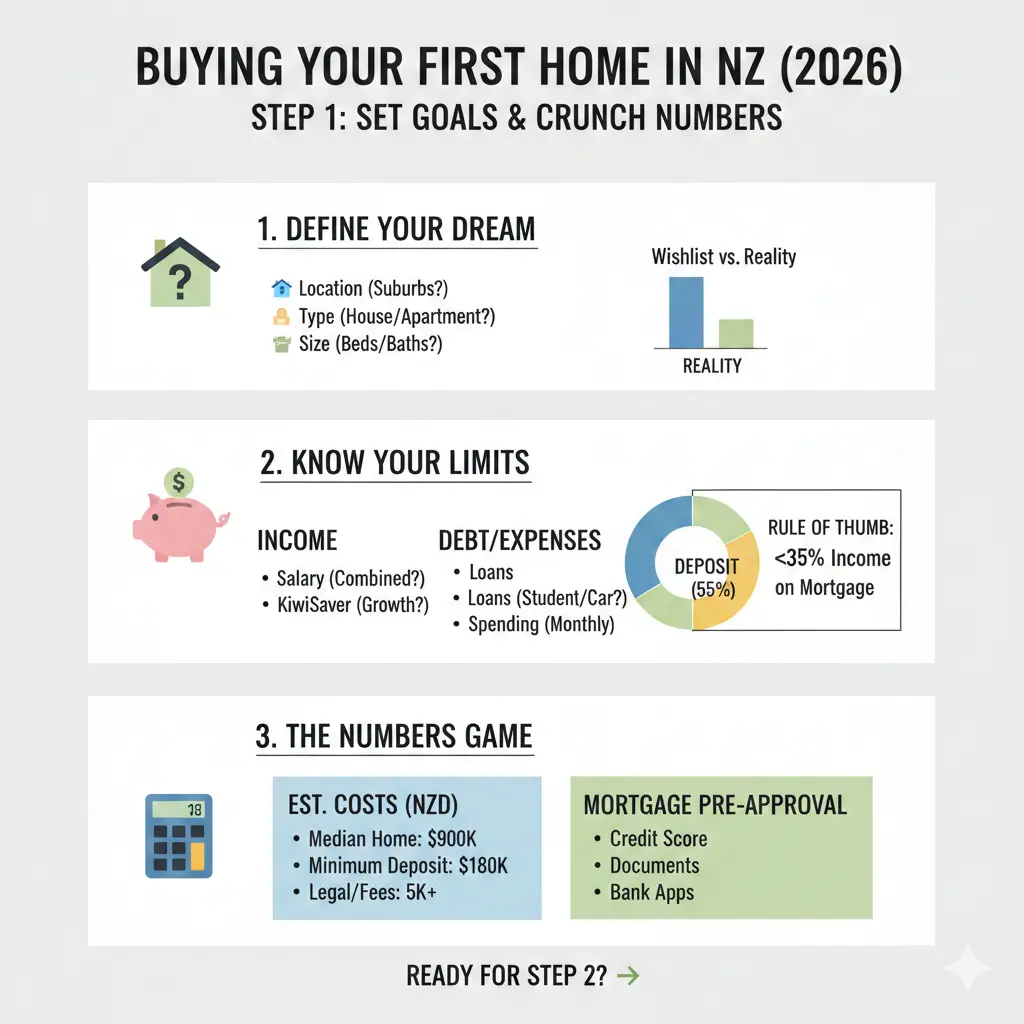

Step 1: Set Your Goals and Crunch the Numbers

Before diving into listings on Trade Me or realestate.co.nz, get crystal clear on what you want long-term. Do you dream of a sunny villa in Auckland's suburbs, a modern unit in Wellington, or something rural near Christchurch? Factor in your lifestyle, family plans, and commute.

Build a Realistic Budget

Review your finances thoroughly. Calculate your income, expenses, debts, and savings. Aim for a deposit of at least 20% to avoid costly Lenders Mortgage Insurance (LMI), but know options exist for as low as 5%. Use free online calculators from banks like ANZ to estimate borrowing power based on your situation.

- List all monthly costs: rent, groceries, power bills, KiwiSaver contributions, and fun stuff like footy tickets.

- Track spending for three months using apps like PocketSmith or a simple spreadsheet.

- Factor in ongoing homeownership costs: council rates (around $2,000–$4,000/year), insurance ($1,500+), and maintenance (1–2% of home value annually).

Pro tip: Stress-test your budget for interest rate rises. In 2026, floating rates hover around 6–7%, but fixed options start from 5.5%.

Maximise Your Deposit with KiwiSaver

KiwiSaver is a first-home buyer's best mate. If you've been contributing for at least three years, you can withdraw your savings (and government contributions) for a deposit, plus an extra $10,000 per person from the First Home Withdrawal scheme. First-home buyers withdrew over $1.2 billion in 2025 alone—don't leave yours sitting there.

- Check your balance via your provider's app or myIR.

- Get free financial advice from Sorted.org.nz.

- Combine with family gifts (up to $500,000 tax-free under gifting rules).

Step 2: Get Pre-Approved and Explore Schemes

Pre-approval from a bank or broker like Squirrel gives you a clear spending limit and bargaining power at auctions—essential in NZ's fast market. You'll need to show income proof, three months' bank statements, and your deposit.

Government Help from Kāinga Ora

If equity is tight, Kāinga Ora's First Home Loan lets you buy with just 5% deposit—they underwrite the risk for participating banks. Eligibility: NZ citizen/permanent resident, income under $95,000 individual or $150,000 household, and first-time buyer.

For Māori, the Kāinga Whenua Loan supports buying or building on Māori land. Kāinga Ora tenants might snag a $20,000 grant to buy their rental. Note: First Home Partner is closed, but check kaingaora.govt.nz for updates.

| Scheme | Min Deposit | Income Cap | Best For |

|---|---|---|---|

| First Home Loan | 5% | $95k/$150k | Low-equity buyers |

| KiwiSaver Withdrawal | Varies | None | Savers |

| Kāinga Whenua | Low | Varies | Māori land |

Step 3: House Hunting Like a Pro

With pre-approval in hand, hit the open homes. Prioritise location over perfection—buy the worst house on the best street for future growth. In 2026, Auckland median prices sit around $1.05 million, Wellington $850,000, Christchurch $750,000 (Stats NZ estimates).

Key Checks Before Viewing

- Aspect and sun: North-facing for warmth in our climate.

- Neighbours and noise: Chat with locals, visit at night.

- Schools and transport: Use school zones via education.govt.nz.

- LIM and PIM reports: Free from council, reveal consents, hazards.

Budget $600–$1,000 for a building inspection—crucial to spot leaky homes or weathertightness issues. Get a free ANZ Property Insights Report for value checks.

Step 4: Making an Offer and Navigating Sales

NZ sales happen via auction (fast, unconditional), tender (confidential), or negotiation. Auctions dominate—practice bidding and set a strict limit.

Legal Must-Dos

- Hire a conveyancing lawyer ($2,000–$4,000).

- Review the sale agreement carefully.

- Pay 10% deposit on auction win.

- Conditions: Finance, inspection, title search.

Avoid pitfalls like skipping due diligence—10 common mistakes include ignoring body corporate fees or overbidding emotionally.

Step 5: Settlement and Moving In

Settlement is typically 20–90 days post-agreement. Confirm insurance (day one coverage), utilities transfer, and KiwiSaver top-ups if needed.

- Organise removals early—budget $1,000–$3,000.

- Update address with IRD, WINZ, banks.

- Check for chattels (curtains, stoves) in the agreement.

Congrats—you're a homeowner! Budget for rates, ACC levies, and power (EECA grants for insulation upgrades).

Practical Tips to Save Time and Money in 2026

- Use whānau co-ownership for bigger deposits.

- Shop brokers for best rates—Squirrel or ANZ toolkit.

- Watch webinars like ANZ's Property Unlocked.

- Avoid overseas buyer traps if applicable (OIO rules).

Your Next Steps to Homeownership

Grab your coffee, pull out your KiwiSaver statement, and book a free broker chat today. Download Kainga Ora's guide or ANZ's handbook, run the numbers, and start viewing. In 2026, persistence pays off—your slice of NZ paradise awaits. Head to lifetimes.co.nz for more tools, job listings, and local ads to support your journey.

Frequently Asked Questions

Sources & References

-

1

Guide to buying a home - Kainga Ora — kaingaora.govt.nz

-

2

The ultimate guide to buying your first house in NZ - Squirrel — www.squirrel.co.nz

-

3

Buying your first home | Home Buyers Handbook - ANZ — www.anz.co.nz

-

4

40 Must-Know House Buying Tips - MoneyHub — www.moneyhub.co.nz

-

5

Buying property in New Zealand in 2026 - Smart Currency Exchange — www.smartcurrencyexchange.com

- 6

-

7

5 Things First Home Buyers Can Do to Buy in 2026 — www.thefirsthomebuyersclub.co.nz

-

8

Buying Your First Home in NZ in 2026? Watch This First - Spotify — open.spotify.com

-

9

Buying Your First Home in NZ in 2026? Watch This First - YouTube — www.youtube.com

Related Articles

First Home Grant NZ: How to Get Up to $10000

Buying your first home is one of the biggest financial decisions you'll make, and the New Zealand government wants to help. The First Home Grant puts up to $10,000 directly towards your deposit, makin...

Why 2026 is the Hardest Year to Buy a Home (and How to Beat the Odds)

Imagine standing at the edge of the property ladder in 2026, eyeing your dream home while prices hover stubbornly high, listings pile up, and buyer confidence wavers. For Kiwis, this year feels toughe...

Selling Your Home? 10 Low-Cost Renovations That Add $50k in Value

If you're planning to sell your home in New Zealand, you don't need to break the bank with a complete renovation to attract buyers and boost your sale price. The good news? Some of the most effective...

Tiny Homes in NZ: Legal Hurdles and Living Realities

Imagine downsizing your life into a cosy 70-square-metre haven on your own section, free from the hassle of building consents and council red tape. For Kiwis grappling with sky-high housing costs, tin...