How to Create a Realistic Budget for Your NZ Household

Ever stared at your bank balance mid-month, wondering where all your hard-earned cash disappeared to? You're not alone—many Kiwi households struggle to make ends meet amid rising costs for rent, groce...

Sarah covers personal finance, tax, and KiwiSaver topics for Lifetimes NZ. She focuses on making money management straightforward and practical for everyday Kiwis.

Ever stared at your bank balance mid-month, wondering where all your hard-earned cash disappeared to? You're not alone—many Kiwi households struggle to make ends meet amid rising costs for rent, groceries, and power in 2026.Creating a realistic budget for your NZ household is the game-changer that puts you back in control, helping you cover essentials, stash away savings, and even enjoy the odd treat without the stress.

In this guide, we'll walk you through practical steps tailored to New Zealand life, from tracking Auckland rents to savvy shopping at Pak'nSave. Whether you're flatting in Wellington, raising a whānau in Christchurch, or buying your first home, these tips draw on real 2026 costs and official resources to build a budget that works for you.

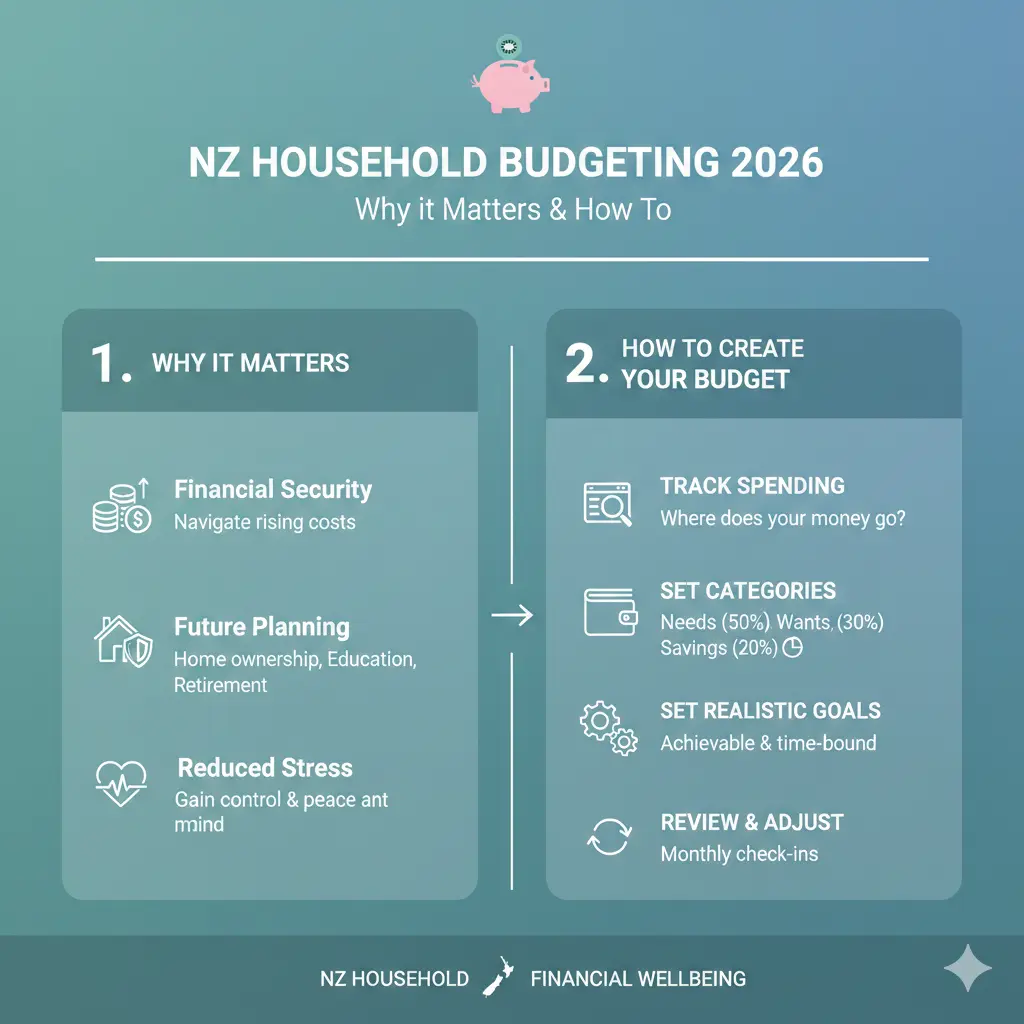

Why Budgeting Matters for Kiwi Households in 2026

With living costs climbing—think weekly rents hitting $550-$600 in central Auckland (that's $2,300-$2,600 monthly)—a solid budget isn't optional; it's essential.Budgeting your NZ household lets you spot leaks like impulse coffee runs or forgotten subscriptions, freeing up cash for KiwiSaver or family holidays.

According to financial experts, reviewing your spending via bank statements reveals patterns in routine expenses, making it easier to trim fat and boost savings.Pay yourself first by directing surplus straight to savings or investments.

Plus, in 2026, tools like Sorted's free budget planner make it dead simple to map your incomings and outgoings, adapting to everything from hall-of-residence life to family setups.

Step 1: Calculate Your Total Household Income

Start with the basics: list every dollar coming in. For most NZ households, this means wages, but don't overlook benefits, side hustles, or rental income.

- Regular pay: After tax, via your payslip. Use IRD's tax calculator for accuracy.

- Benefits: Working for Families, Jobseeker, or Accommodation Supplement if eligible—check Work and Income.

- Other: Child support, investments, or KiwiSaver withdrawals (if over 65).

Average household income varies: a single flatmate might pull $800-$1,200 weekly post-tax, while a couple could hit $2,000+ combined. Be realistic—factor in KiwiSaver contributions (minimum 3%, voluntary up to 10%) and student loans if applicable.

Pro Tip: Account for Irregular Income

If you're gig-working or seasonal (think tourism in Queenstown), average the last 3-6 months. Tools like bank apps auto-track this for you.

Step 2: Track Your Fixed and Variable Expenses

Next, dissect your outgoings. Fixed costs are non-negotiables; variables offer wiggle room. Pull statements from the past 3 months and average them—power fluctuates seasonally, for instance.

Fixed Expenses: The Non-Negotiables

These hit like clockwork. Here's a 2026 NZ breakdown for a two-adult Auckland household:

| Category | Weekly Cost | Monthly Cost (x4.33) |

|---|---|---|

| Rent (central Auckland 2-bed) | $550-$600 | $2,300-$2,600 |

| Power & Gas | $25-$30 | $100-$130 |

| Internet/Wi-Fi | $20 | $80-$100 |

| Mobile Phones (x2) | $25-$30 | $110-$130 |

| Insurance (car/home) | Varies | $100-$200 |

Suburbs slash rent; bonds are 4 weeks' upfront. Don't forget credit card minimums or hire purchase.

Variable Expenses: Where Savings Hide

These flex—groceries for two: $150 weekly ($650 monthly), plus $80 cleaning supplies. Meat-heavy? Add $100. Transport: AT Hop card $44 weekly pass in Wellington, or fuel if driving.

- Groceries: Shop Pak'nSave/Countdown for $120-$175 weekly; Asian stores cut costs further.

- Eating Out: Cap at $50-$100 monthly to avoid budget busts.

- Transport: Public pass beats fuel/parking ($325+ monthly).

Step 3: Build Your 50/30/20 Budget Framework

Adapt the popular 50/30/20 rule for NZ: 50% needs (rent, bills), 30% wants (entertainment, dining), 20% savings/debt. For a $5,000 monthly household income:

- 50% Needs ($2,500): Housing, utilities, food basics, transport.

- 30% Wants ($1,500): Gym, streaming, hobbies—track via apps.

- 20% Savings ($1,000): Emergency fund (3-6 months' expenses), KiwiSaver, debt repayment.

Tweak for high-rent cities: Auckland couples might push needs to 60%. Use Sorted's planner to test scenarios.

NZ-Specific Adjustments

Factor ACC levies, student loans (repaid via PAYE), and rates if owning. Families: Add childcare ($200-$400 weekly).

Step 4: Cut Costs Without Sacrificing Lifestyle

Smart Kiwis save hundreds monthly:

- Switch providers: Compare power (Glide/Contacts), internet (2degrees).

- Meal plan: Batch-cook; buy specials at Countdown apps.

- Ditch car: Save $325+ on parking/fuel—use buses/trains.

- Subscriptions audit: Cancel unused Netflix/Spotify.

- Second-hand: TradeMe for furniture; setup costs $1,000-$1,500.

One Auckland couple trimmed groceries to $730 total by mixing supermarkets.

Tools and Apps for Effortless Budgeting

Leverage free NZ gems:

- Sorted Budget Planner: Custom charts for income/expenses.

- Bank apps (Westpac/ANZ): Auto-categorise spending.

- YNAB or PocketSmith: Envelope system for households.

Review monthly—adjust for inflation or windfalls.

Common Budgeting Mistakes to Avoid

Don't wing it: Ignoring averages leads to shortfalls. Skip one-offs like holidays ($2,000) in monthly views—park them separately. Overlook KiwiSaver? You're leaving free employer matches on the table.

Your Next Steps to a Stress-Free Budget

Grab a coffee (or make one at home), download Sorted's planner, and list your numbers today. Track for 30 days, then refine. In months, you'll have an emergency fund growing and guilt-free spends. Remember, a realistic budget for your NZ household builds security—start small, stay consistent, and watch your finances thrive.

Frequently Asked Questions

Sources & References

-

1

Couple Life in Auckland 2026: Full Monthly Cost Breakdown — www.youtube.com

-

2

How to create a budget and stick to it | Westpac NZ — www.westpac.co.nz

-

3

Money Matters 2026 - Victoria University of Wellington — www.wgtn.ac.nz

-

4

How Does it Cost to Travel New Zealand in 2026? - Nomadic Matt — www.nomadicmatt.com

-

5

Get your finances sorted in 2026: Set a budget | RNZ News — www.rnz.co.nz

-

6

10 Things to Do Differently with Money in 2026 - MoneyHub NZ — www.moneyhub.co.nz

-

7

How to Start Planning for 2026 | NZ Financial Guide — www.provincialwealth.co.nz

-

8

Budget Policy Statement 2026 - Budget 2025 — budget.govt.nz

-

9

Budget planner - Sorted — sorted.org.nz

-

10

Budget 2026 | The Treasury New Zealand — www.treasury.govt.nz