ACC Levies for Businesses: Understanding Your Obligations

As a Kiwi business owner, few things hit your bottom line harder than unexpected ACC levy hikes—especially with the major changes rolling out in 2026. Whether you're running a tradie firm in Auckland,...

Sarah covers personal finance, tax, and KiwiSaver topics for Lifetimes NZ. She focuses on making money management straightforward and practical for everyday Kiwis.

As a Kiwi business owner, few things hit your bottom line harder than unexpected ACC levy hikes—especially with the major changes rolling out in 2026. Whether you're running a tradie firm in Auckland, a retail shop in Christchurch, or a tech startup in Wellington, understanding your ACC obligations ensures you're covered without nasty surprises come tax time.

ACC levies fund New Zealand's no-fault injury cover system, protecting workers (including you if you're self-employed) from work-related accidents. But from 2026, levy rates are rising, discounts are vanishing, and new rules apply—potentially adding thousands to your costs. This guide breaks it down, with practical steps to calculate, pay, and minimise your levies under the latest 2026 rules.

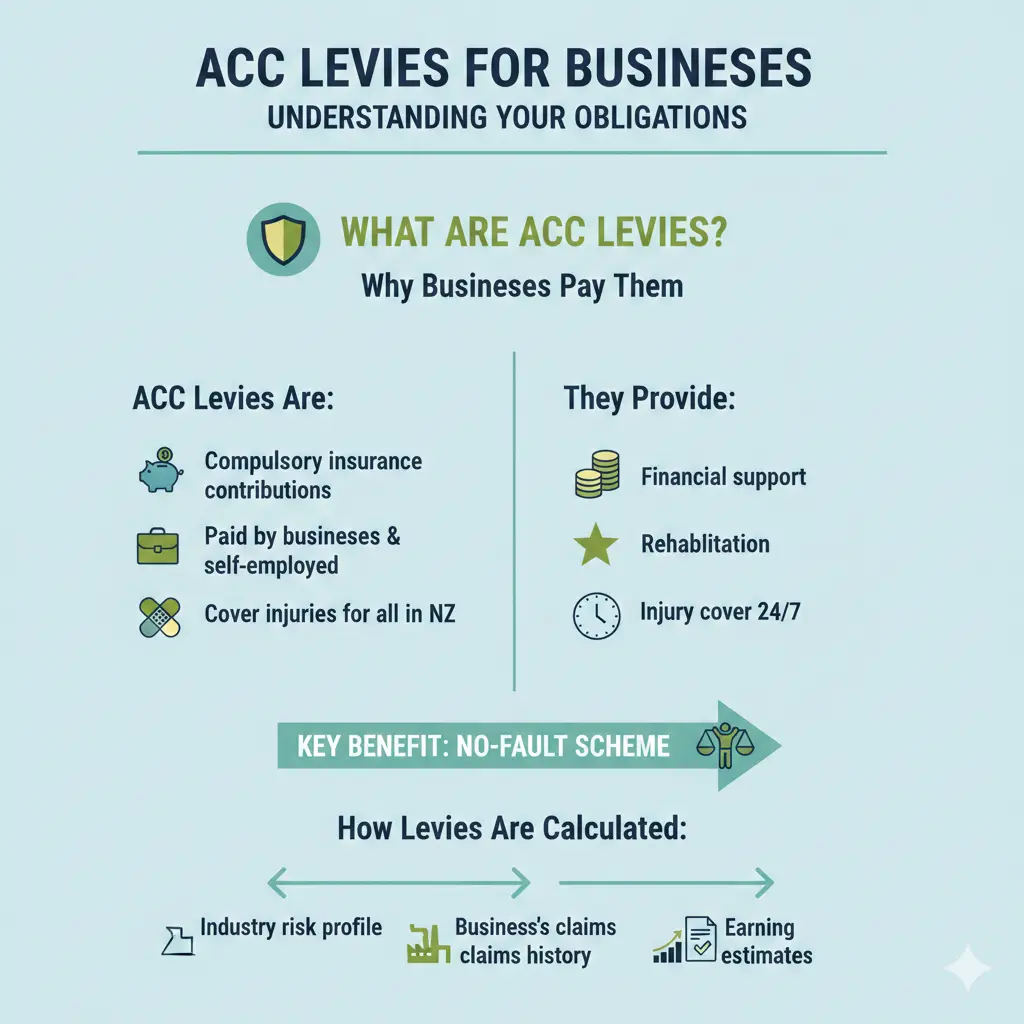

What Are ACC Levies and Why Do Businesses Pay Them?

ACC levies are mandatory contributions to the Accident Compensation Corporation (ACC), New Zealand's public injury insurer. They cover rehabilitation, treatment, and income support for work-related injuries, ensuring injured Kiwis get back on their feet without suing employers.

For businesses, levies split into key parts:

- Work Levy: Covers workplace injuries for employees and self-employed owners. Rated per $100 of liable earnings (wages, salaries, benefits).

- Earners' Levy: A flat rate on all liable earnings up to a maximum, deducted via PAYE or directly by self-employed.

- Working Safer Levy: Funds WorkSafe NZ's health and safety efforts, collected alongside Work Levy.

- Motor Vehicle Levy: Per vehicle, if your business uses company cars or utes.

Self-employed sole traders and partnerships pay on their own earnings too—no dodging this as a working owner. ACC sends a provisional invoice yearly (based on prior earnings estimates), followed by a year-end adjustment via IRD data.

How ACC Calculates Your Business Levies

Your levy depends on:

- Liable Earnings: Gross wages minus exemptions (e.g., overtime over 40 hours/week). Updated max/min thresholds for 2026/27: max $156,641, min $50,501.

- Classification Unit (CU): Industry-specific risk group (e.g., construction higher than offices). New 2026 CUs for home improvement stores and pro sports.

- Experience Rating (ER): For medium/large firms—rewards low claims with discounts, penalises high ones. Threshold for medical costs up from $500 to $750 in 2026.

Example: A Wellington cafe with $500,000 liable earnings in a low-risk CU at 2026/27 average Work Levy rate of $0.69/$100 pays $3,450 base Work Levy. Add ER adjustments, Earners' Levy, and GST—your invoice climbs fast.

Key ACC Levy Changes for Businesses in 2026

ACC levies reset every three years, with 2025/26–2027/28 confirmed by Cabinet in late 2024. Here's what hits businesses hardest from 1 April 2026.

Increased Levy Rates Across the Board

Average rates rise to balance ACC's accounts amid rising claims:

| Levy Type | 2024/25 Rate | 2026/27 Rate | Increase |

|---|---|---|---|

| Average Work Levy | $0.63/$100 earnings | $0.69/$100 | +9.5% over period |

| Earners' Levy | $1.67/$100 (Apr 2025–Mar 2026) | $1.75/$100 (Apr 2026–Mar 2027) | +4.8% |

| Motor Vehicle (average) | $113.94/vehicle | $131.94/vehicle | +15.8% |

Max Earners' Levy for 2026/27: $2,741.22 on $156,641 earnings. Provisional invoices from 2026 reflect these, with full adjustments later.

End of No Claims Discount and ER Cross-Subsidies

Big shift: The No Claims Discount ends 2026—no more free ride for claim-free businesses. Experience Rating (for firms with 50+ full-time equivalents or $900k+ earnings) goes self-funding from 2027 levies (billed 2026). Non-ER businesses stop subsidising it; ER firms pay extra 7.2% ER Programme rate on Work Levy.

Pro tip: Check your ER status via myACC for business. Low-claim ER firms might see levies drop long-term without subsidies.

New Rules for Payments, Sports, and Retail

- Instalment Interest: From 2026, interest (RBNZ 90-day rate) on all payment plans—no exceptions unless waived.

- Sports & Home Improvement: New CUs for pro sports/ballet (non-employers too) and hardware stores like Bunnings-style ops—expect higher rates.

- Moto Changes: 25% levy discount for advanced rider course completers; motorcyclists subsidised more (33% in 2026).

How to Calculate Your 2026 ACC Levies Step-by-Step

Don't guess—use ACC's online tools for accuracy.

- Estimate Liable Earnings: Total payroll + owner drawings (self-employed). Use IRD wage data for precision.

- Find Your CU Rate: Log into myACC business account or check ACC's CU finder. Average Work Levy $0.69/$100 for 2026/27.

- Add ER if Applicable: Calculate loading/discount via ACC's ER calculator. New $750 med threshold applies.

- Include Earners' & Vehicle Levies: $1.75/$100 up to max; per-vehicle rates via ACC.

- Apply GST & Adjustments: Provisional = estimate; year-end true-up.

Practical Example: Auckland construction firm, $1M earnings, high-risk CU ($1.20/$100 rate), ER discount -10%.

- Work Levy: $1M x 1.20% = $12,000 base; ER-adjusted $10,800.

- Earners' (10 staff avg $100k): ~$17,500.

- Total provisional: ~$30k+ GST. Budget 10% buffer for hikes.

Payment Options and Avoiding Penalties

ACC offers flexible payments, but 2026 tightens up:

- Provisional Invoice: Due July, based on prior year. Pay monthly/quarterly.

- Instalments: Interest from 2026—pay in full to avoid.

- Year-End Adjustment: IRD shares PAYE data; overpay gets credit, underpay invoices with late fees.

Tip: Link ACC to your IRD myIR account for seamless adjustments. Self-employed? Pay direct via ACC or bundle with provisional tax.

Tips to Minimise Your ACC Levies Legally

Lower risk, lower levies—here's how:

- Health & Safety: Implement WorkSafe plans to cut claims, boosting ER discounts.

- Accurate Classifications: Audit your CU yearly—misclassification overcharges.

- Vehicle Management: Choose low-risk vehicles; train riders for discounts.

- ER Optimisation: Track claims under $750 threshold.

- Payroll Tweaks: Maximise exemptions (e.g., KiwiSaver contributions not liable).

Consult an accountant familiar with IRD/ACC integration—saves more than fees.

Next Steps: Stay Compliant and Save

Log into myACC today to review your 2026 provisional invoice and CU. Budget for 5-10% hikes, audit payroll for accuracy, and prioritise safety to trim future levies. Pair this with KiwiSaver contributions and IRD tax planning for full financial cover.

Disclaimer: This is general info for 2026 rates. Levies vary by business—seek advice from an ACC-accredited adviser or accountant for personalised guidance.

Frequently Asked Questions

Sources & References

-

1

ACC Workplace Cover Levy Changes - NZQBA — nzqba.co.nz

-

2

Setting the average ACC levy rates for 2025/26, 2026/27, and 2027/28 — www.mbie.govt.nz

-

3

ACC earners' levy rates - Inland Revenue — www.ird.govt.nz

-

4

Medium and large business - ACC — www.acc.co.nz

- 5

-

6

ACC levies - Business.govt.nz — www.business.govt.nz

-

7

US Expat Taxes for Americans Living in New Zealand - A Guide — onlinetaxman.com

Related Articles

Industry Bodies and Professional Associations NZ

Whether you're launching a business, advancing your career, or navigating financial regulations, industry bodies and professional associations in New Zealand offer invaluable support. These organisati...

Emergency Benefit NZ: When You Have No Other Options

When you're struggling financially and don't qualify for other benefits, the Emergency Benefit might be your lifeline. It's a discretionary payment designed for Kiwis in genuine hardship who've exhaus...

Unpaid Internships NZ: Are They Legal?

Unpaid internships are a common pathway for students and graduates to gain work experience in New Zealand, but there's often confusion about whether they're actually legal. The short answer is: unpaid...

Estate Administration NZ: Managing Someone's Affairs After Death

Losing a loved one is one of life's toughest challenges, and stepping in to manage their estate can feel overwhelming. In New Zealand, estate administration—the process of handling someone's affairs a...