Fixed vs Floating Rates: Which Is Right for You?

Imagine locking in your mortgage payments today, only to watch interest rates plummet tomorrow—or the opposite, seeing your repayments soar unexpectedly. For Kiwis navigating home loans in 2026, this...

Sarah covers personal finance, tax, and KiwiSaver topics for Lifetimes NZ. She focuses on making money management straightforward and practical for everyday Kiwis.

Imagine locking in your mortgage payments today, only to watch interest rates plummet tomorrow—or the opposite, seeing your repayments soar unexpectedly. For Kiwis navigating home loans in 2026, this is the real-world dilemma of choosing between fixed vs floating mortgage NZ options. With the Official Cash Rate (OCR) influencing market shifts and banks like ANZ tweaking rates as recently as January, understanding these choices is crucial for your financial peace of mind.

In this guide, we'll break down the differences, weigh the pros and cons, and share practical tips tailored to New Zealand homeowners. Whether you're a first-home buyer in Auckland or refinancing in Christchurch, you'll find actionable advice to decide what's right for you.

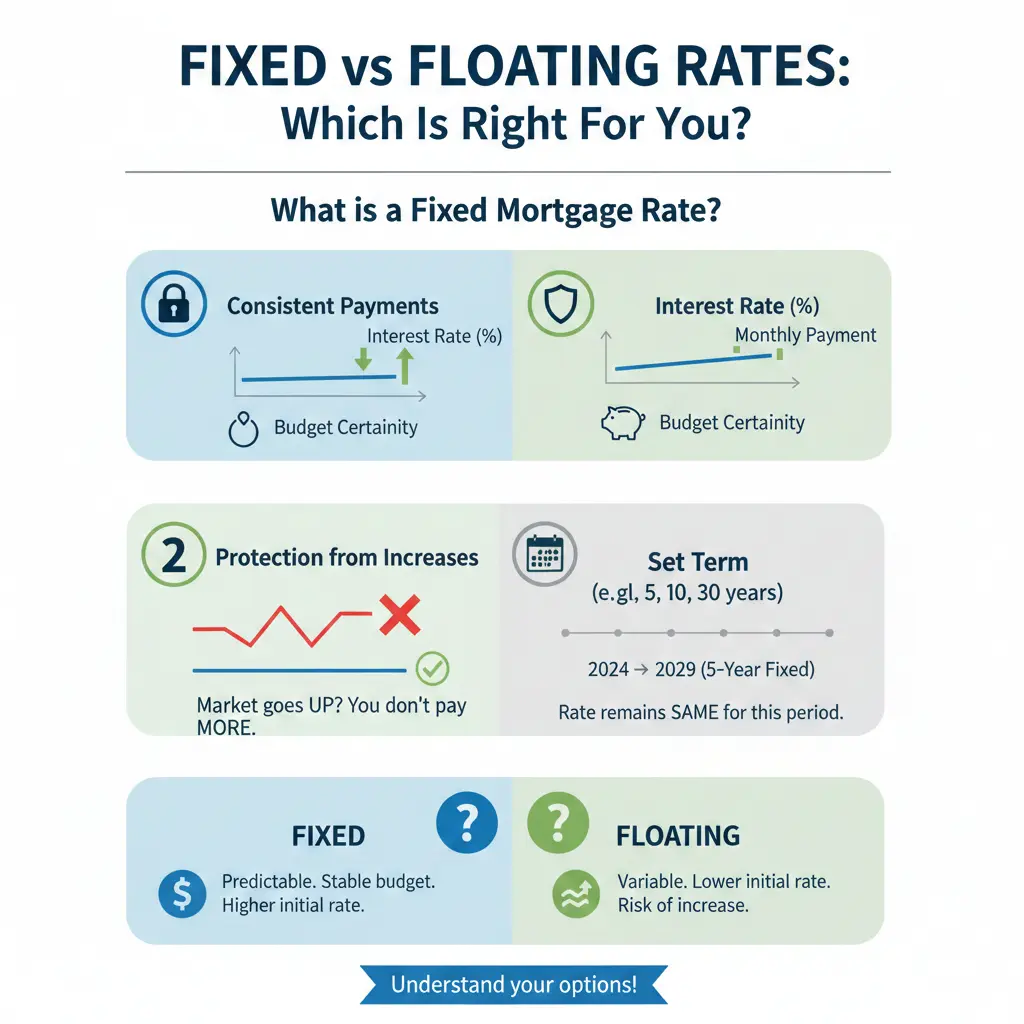

What is a Fixed Mortgage Rate?

A fixed mortgage rate locks your interest rate for a set period, usually 6 months to 5 years. Your repayments stay the same, no matter what happens to market rates. This predictability is a big draw for many Kiwis who value stable budgeting.

Benefits of Fixed Rates

- Predictability: Know exactly what you'll pay each month, making it easier to plan family budgets or savings.

- Protection from rises: If rates climb, you're shielded during your fixed term.

- Peace of mind: Ideal for long-term planning, like saving for kids' education or renovations.

Drawbacks of Fixed Rates

- Less flexibility: Breaking early for refinancing or extra repayments can trigger hefty break fees.

- Missed opportunities: If rates drop, you won't benefit until the term ends.

For example, as of late January 2026, the average 1-year fixed rate sits at around 4.67%, compared to floating at 5.65%—a 0.98% gap that tempts many to fix for short terms.

What is a Floating Mortgage Rate?

A floating (or variable) mortgage rate fluctuates with the market, tied closely to the Reserve Bank of New Zealand's OCR and bank policies. Repayments can rise or fall, offering flexibility but less certainty.

Benefits of Floating Rates

- Flexibility: Make lump-sum repayments or switch without penalties—perfect for aggressive debt payoff.

- Potential savings: If rates drop, your payments decrease automatically.

- Suits short-term needs: Great for bridging finance or if you expect to sell soon.

Drawbacks of Floating Rates

- Unpredictability: Payments could jump if rates rise, complicating budgets.

- Usually higher: Often 1-2% above fixed rates currently.

Recent changes highlight this: ANZ raised its floating home loan rate to 5.79% effective 29 January 2026, up 0.10%. Yet, floating averaged 5.65% recently, still above 1-year fixed at 4.67%.

Fixed vs Floating: Key Differences at a Glance

To help you compare, here's a quick table of fixed vs floating mortgage NZ options based on current 2026 trends:

| Feature | Fixed Rate | Floating Rate |

|---|---|---|

| Rate Stability | Locked for term (e.g., 1-5 years) | Changes with market/OCR |

| Current Average (Jan 2026) | 4.67% (1-year) | 5.65% |

| Flexibility | Limited; break fees apply | High; extra repayments free |

| Best For | Budget certainty | Rate drops, quick payoff |

Current Mortgage Rates in New Zealand (2026)

As of January 2026, fixed rates remain attractive for short terms. The 1-year fixed is about 0.98% lower than floating, at 4.67% vs 5.65%. Banks vary: ANZ's floating is now 5.79% post a recent hike, while wholesale rates hint at possible softening later in 2026 due to economic recovery and OCR cuts.

Longer fixes (over 2 years) may rise, per RNZ analysis, amid global influences. Always compare across ASB, BNZ, Kiwibank, and Westpac—rates differ by lender.

Which is Right for You? Scenarios for Kiwis

No one-size-fits-all, but here's how to choose based on your situation:

Choose Fixed If:

- You're a first-home buyer needing stable payments.

- Rates seem poised to rise (watch OCR announcements from rbnz.govt.nz).

- You prioritise budgeting over flexibility.

Choose Floating If:

- You plan extra repayments via revolving credit.

- Economists predict drops (e.g., slow NZ recovery).

- You're selling soon or have budget buffer.

The Smart Split Option

Many Kiwis split their mortgage—say, 70% fixed for stability, 30% floating for flexibility. This hedges risks and captures upsides. Chat to a broker to structure it right.

Factors Influencing Your Decision

Reserve Bank of New Zealand's OCR

The OCR drives floating rates and influences fixes. Drops can lower floating quickly; competition among banks may follow.

Economic Outlook for 2026

Experts foresee slight drops through 2026, but no return to sub-3% anytime soon. Watch inflation risks from global tariffs.

Your Financial Profile

- High income, low debt: Floating's fine.

- Tight budget: Fix for peace.

- Investors: Short fixes or splits to pivot.

Pro tip: Use tools like MoneyHub's fixed vs floating calculator to model scenarios with your balance and term.

Practical Tips for Switching or Refixing

- Get broker advice: Free from advisors registered with the Financial Markets Authority (fma.govt.nz).

- Compare rates weekly: Sites like interest.co.nz or canstar.co.nz aggregate NZ bank offers.

- Time your fix: 1-year often beats 6-month unless big drops expected.

- Consider breaks: Weigh fees vs savings if switching early.

- Review annually: Refix before term ends to avoid default floating.

"If she chose the floating rate she'd have to pay a higher rate (+1.22%). But she had flexibility to take advantage of lower interest rates... especially if she pays off her mortgage aggressively."

Next Steps: Take Control of Your Mortgage

Ready to decide? Start by checking your current rate against bank specials, run numbers with an online calculator, and book a free chat with a mortgage broker. Monitor RBNZ updates and economic news—small choices now can save thousands. Whether fixed, floating, or split, the right pick aligns with your goals and Kiwi lifestyle.

Frequently Asked Questions

Sources & References

-

1

Current mortgage interest rates in NZ [2026] - Opes Partners — www.opespartners.co.nz

-

2

Fixed vs Floating Mortgage Rate Calculator - MoneyHub — www.moneyhub.co.nz

-

3

Fixed vs Floating Mortgage Rates in New Zealand: Which One's Right for You? - Lenda Mortgages — lendalmortgages.co.nz

-

4

Fixed vs Floating Mortgage: What's Better in NZ This Year? - Look Ahead — www.lookahead.co.nz

-

5

Fixed vs Floating: Your Mortgage Strategy for 2025-2026 - Velocity Financial — www.velocityfinancial.co.nz

-

6

Changes to ANZ rates, fees and agreements - ANZ — www.anz.co.nz

-

7

2026 Mortgage Rate Outlook: Scenarios, No Certainties! - New Zealand Mortgages — www.newzealandmortgages.co.nz

- 8