Mortgage Break Fees NZ: How Much Will It Cost to Switch?

Ever stared at your mortgage statement, dreaming of switching to a lower rate but frozen by the dreaded words "break fee"? You're not alone—thousands of Kiwis face this dilemma every year as interest...

Sarah covers personal finance, tax, and KiwiSaver topics for Lifetimes NZ. She focuses on making money management straightforward and practical for everyday Kiwis.

Ever stared at your mortgage statement, dreaming of switching to a lower rate but frozen by the dreaded words "break fee"? You're not alone—thousands of Kiwis face this dilemma every year as interest rates shift. In 2026, with the RBNZ OCR hovering around neutral levels and mortgage rates settling between 4.5% and 5%, breaking your fixed-term mortgage to switch lenders could save you thousands in interest, but only if the break fee doesn't wipe out those gains. This guide breaks down everything you need to know about mortgage break fees NZ, how much it might cost to switch, and practical steps to make the smartest move for your home loan.

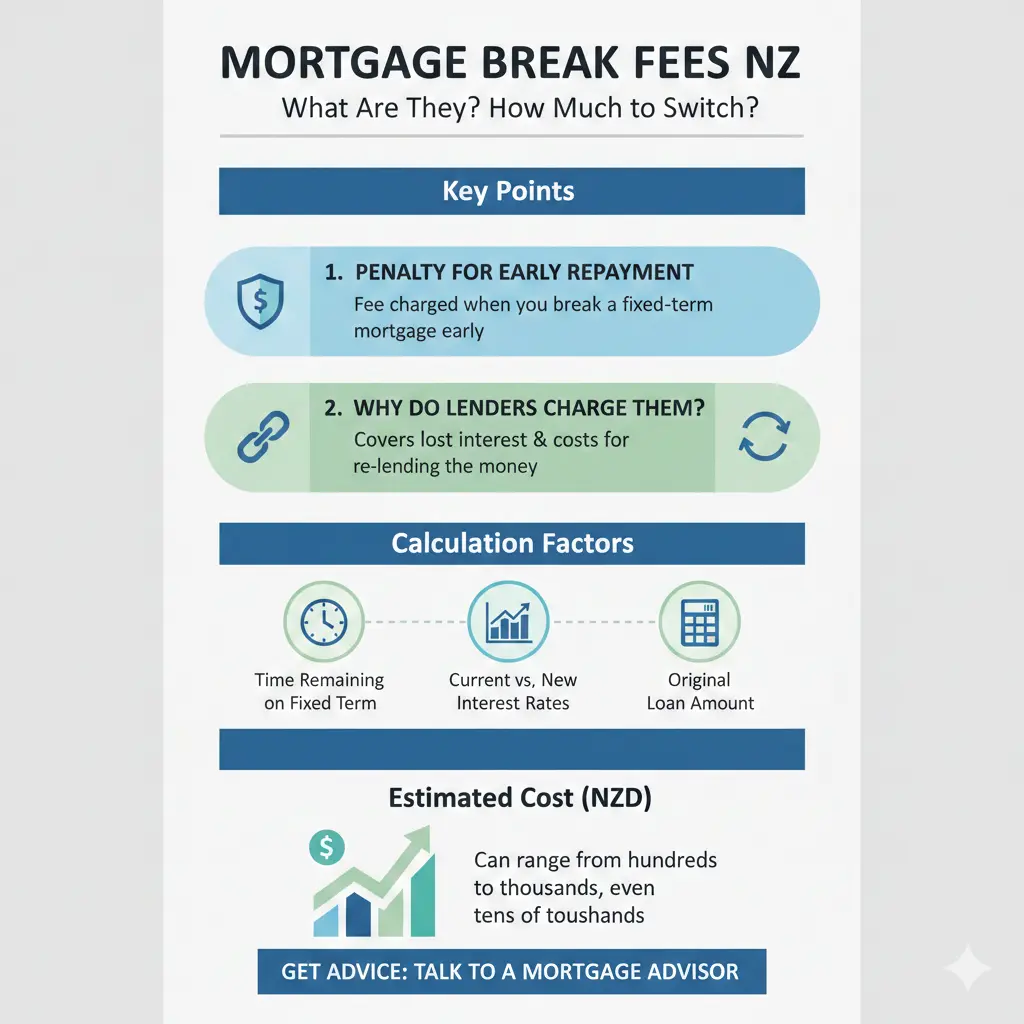

What Are Mortgage Break Fees in New Zealand?

Mortgage break fees—also called early repayment recovery or prepayment costs—are penalties charged by your bank when you end a fixed-rate mortgage term early. They kick in if you pay off the loan in full, make a large lump-sum repayment, refinance with another lender, or switch banks before the fixed period ends.

These fees compensate the lender for lost interest income and the cost of breaking their own wholesale funding arrangements. Banks like ANZ, Westpac, Kiwibank, and TSB all use similar logic: when you fixed your rate, they locked in funding from wholesale markets at a set rate. If rates drop and you break early, they pass on their penalty to you—no discounts.

When Do Break Fees Apply?

- Full repayment: Selling your home and paying off the mortgage.

- Refinancing or switching lenders: Moving to a better deal elsewhere.

- Large extra repayments: Paying more than allowed under your contract (often over 5-20% of the balance annually, depending on the bank).

- Restructure: Changing terms, like splitting a fixed loan into floating portions.

Variable or floating-rate mortgages usually don't attract break fees, as there's no fixed term to break.

How Are Mortgage Break Fees Calculated in NZ?

Unlike a simple flat percentage, break fees use a formula based on wholesale swap rates—the rate banks pay to fund your loan. It's not your mortgage rate that matters, but the bank's borrowing cost at the start versus now.

The Standard Break Fee Formula

Banks follow a four-step process, often outlined vaguely in lengthy terms (like Kiwibank's 30+ page PDF). Here's how it typically works:

- Difference in rates: Original wholesale rate minus current wholesale rate.

- Apply to balance: Rate difference x remaining mortgage balance.

- Multiply by time: Result x remaining months/years on the fixed term (often in whole years).

- Add bank fees: Admin or processing costs.

Example from Squirrel: You fixed at 4.00% wholesale with $600,000 left and 4 years remaining. Rates drop to 2.75%.

(4.00% - 2.75%) x $600,000 = $7,500

$7,500 x 4 years = $30,000 total break fee.

Plug your numbers into free tools like Interest.co.nz's mortgage break fee estimator for a bank-specific quote—it factors in swap rates and known formulas, though only your bank gives the exact figure.

Simple Percentage Estimate

For a rough guide, fees often range from 2% to 10%+ of the remaining balance, higher with longer terms left. Formula: Break fee = Remaining balance x percentage. E.g., $200,000 balance at 5% = $10,000.

| Remaining Term | Typical Fee Range (% of Balance) | Example ($500k Balance) |

|---|---|---|

| 1 year | 1-3% | $5,000-$15,000 |

| 2-3 years | 3-7% | $15,000-$35,000 |

| 4+ years | 5-10%+ | $25,000-$50,000+ |

Note: These are estimates—actual costs depend on rate movements. Always get a quote.

How Much Will It Cost You to Switch in 2026?

In today's market, with OCR cuts pushing rates down (another 0.50% expected by year-end, more in 2025), break fees can sting but switching often pays off. A $30,000 fee on a $600k loan might be worth it if you save 1% interest annually—that's $6,000/year.

Real Kiwi Examples

- Auckland family: $800k mortgage, 3 years left at 5.5%. New rate: 4.5%. Fee: ~$24,000. Savings: $9,600/year. Payback in under 3 years.

- Wellington couple: $400k, 5 years fixed. Rates drop—fee hits $28,000. But refixing shorter-term avoids it next cycle.

Higher balances amplify costs: on $1m, a 4-year break could exceed $50,000 if rates plunge. Use the formula above or calculators to crunch your scenario.

Factors Affecting Your Cost

- Rate drop magnitude: Bigger drops = higher fees.

- Remaining term: Longer = pricier.

- Loan size: Scales linearly.

- Bank policy: ANZ bases on "economic loss"; Westpac on wholesale differences.

Is It Worth Paying the Break Fee to Switch?

Run the numbers: Compare break fee + new setup costs vs. interest savings over the term.

Break-Even Calculator Tips

- Get your break fee quote (free from bank).

- Estimate savings: (Old rate - new rate) x balance x years.

- Subtract fees, legal costs (~$1,000-$2,000 for switch).

- If savings > costs within 2-3 years, switch.

In 2026's falling rate environment, short fixes (6-12 months) minimise risk—fix short now, switch fee-free later.

Ways to Avoid or Reduce Mortgage Break Fees

Not all hope is lost. Here's how Kiwis dodge or lower costs:

1. Wait It Out

Fixed terms end naturally—no fee. With rates dropping, a 6-12 month fix lets you refix lower soon.

2. Negotiate a Waiver

Banks sometimes waive for hardship (job loss, medical issues, family changes). Contact your relationship manager early.

3. Use Contract Allowances

Most allow 5% extra repayments yearly without fees—chip away gradually.

4. Split Your Mortgage

Keep part fixed, float the rest for flexibility without full break.

5. Tax Deductibility

Break fees may be tax-deductible if linked to income-producing property (e.g., rentals). Check with IRD or an accountant.

Steps to Switch Mortgages Without Breaking the Bank

- Contact current bank: Request a break fee quote (takes 1-2 days).

- Shop rates: Use sites like Interest.co.nz or Canstar for top deals.

- Get pre-approval: From new lender—lock in the rate.

- Weigh costs: Use estimator tools.

- Legal conveyancing: Budget $1,500; use a lawyer experienced in refinances.

- Notify IRD if rental: Update for tax.

- Finalise: New bank pays out old loan, handles fee deduction.

Pro tip: Time your switch near term end to minimise fees.

Next Steps: Make Your Move Today

Don't let break fee fear trap you in a high-rate mortgage. Grab your loan docs, call your bank for a quote, and crunch numbers with a free calculator. Chat with a mortgage adviser (many offer no-fee initial consults) or use broker networks for the best switch deals. In 2026's market, the right move could save you tens of thousands—start today for a lighter financial load tomorrow.

Frequently Asked Questions

Sources & References

-

1

Mortgage Break Fees - MoneyHub NZ — www.moneyhub.co.nz

-

2

Break fees: Why caution is needed when fixing your mortgage - Squirrel — www.squirrel.co.nz

-

3

Home loan rates, fees and agreements - ANZ — www.anz.co.nz

-

4

Mortgage break fee calculator - Interest.co.nz — www.interest.co.nz

-

5

Breaking your fixed rate home loan - Westpac NZ — www.westpac.co.nz

-

6

Early Repayment fee for fixed rate home loans - TSB Bank — www.tsb.co.nz

Related Articles

Using the NZ Mortgage Calculator to Plan Your House Hunt

Imagine spotting your dream home in Auckland or Christchurch, but wondering if you can actually afford it. That's where the NZ Mortgage Calculator comes in—your essential tool for turning house-huntin...

Mortgage Refixing Guide: How to Negotiate the Best Rate with Your Bank

Imagine slashing hundreds of dollars off your weekly mortgage payments just by knowing when and how to refix. With interest rates easing in 2026, thousands of Kiwis are facing refix decisions that cou...

Mortgage Refinancing: When Does It Make Sense?

Imagine shaving thousands off your mortgage interest while unlocking cash for that home reno or debt consolidation you've been dreaming about. For Kiwis with home loans, mortgage refinancing can be a...

How to Pay Off Your Mortgage Faster (NZ Strategies)

Imagine owning your home outright years earlier than planned, freeing up thousands in interest payments and giving you financial freedom sooner. For Kiwis with mortgages, paying off your home loan fas...