Mortgage Refinancing: When Does It Make Sense?

Imagine shaving thousands off your mortgage interest while unlocking cash for that home reno or debt consolidation you've been dreaming about. For Kiwis with home loans, mortgage refinancing can be a...

Sarah covers personal finance, tax, and KiwiSaver topics for Lifetimes NZ. She focuses on making money management straightforward and practical for everyday Kiwis.

Imagine shaving thousands off your mortgage interest while unlocking cash for that home reno or debt consolidation you've been dreaming about. For Kiwis with home loans, mortgage refinancing can be a game-changer—but only if the timing and numbers stack up right. With interest rates fluctuating in 2026, understanding when it truly makes sense is key to avoiding costly pitfalls and maximising savings.

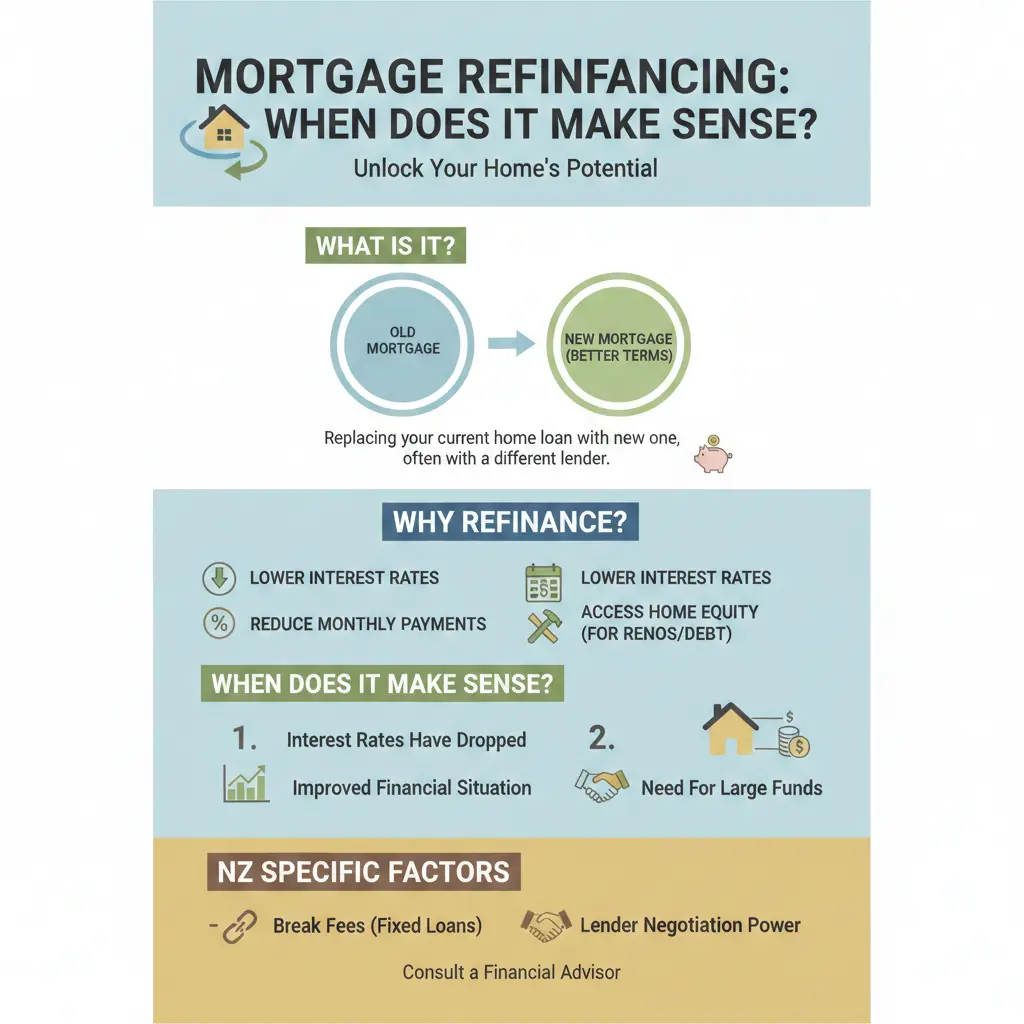

What is Mortgage Refinancing in New Zealand?

Refinancing your mortgage means replacing your existing home loan with a new one, often from a different lender, to snag better terms like lower interest rates, flexible features, or access to equity built up in your property. It's not the same as simply refixing with your current bank—that's more like renewing your fixed term without switching lenders.

In Aotearoa, where home ownership is a cornerstone for many families, refinancing lets you consolidate high-interest debts (think credit cards at 20%+), restructure repayments for better cashflow, or tap into your home's value for investments like a KiwiSaver top-up or property upgrades. But it's not free—expect fresh credit checks, valuations, and legal fees, so it's worth crunching the numbers first.

Refinancing vs Refixing: Key Differences

- Refixing: Sticking with your current lender, just picking a new rate or term at the end of your fixed period. Minimal hassle, no break fees.

- Refinancing: A full new loan application, potentially with a new bank. More work, but access to competitive deals and cashback incentives.

Pro tip: If your fixed term is ending soon, that's prime time to explore both options without penalties.

When Does Mortgage Refinancing Make Sense for Kiwis?

Refinancing shines when the benefits outweigh the costs—typically saving you enough on interest to recoup fees within 2-3 years (your break-even point). Here's when Kiwis are refinancing successfully in 2026:

1. Your Fixed Term is Expiring

The sweet spot? Right before or at the end of your fixed-rate term. No break fees, and you can shop around while your current bank woos you with specials. In 2026, with OCR predictions hinting at steady or slightly falling rates, locking in now could protect against hikes.

2. Interest Rates Have Dropped Significantly

If market rates dip below your current rate by 0.5% or more on a $500,000 loan, you could save $100+ monthly. Calculate your break-even: Divide total refinancing costs by monthly savings. Banks are offering cashbacks of 0.60%-1.00% of your loan value to lure switchers—up to $5,000 on a $500k mortgage.

3. You Need to Access Equity or Consolidate Debt

With NZ house prices rebounding in key centres like Auckland and Christchurch, many homeowners have equity to refinance for renovations, investments, or paying off pricey personal loans. Consolidating $20,000 credit card debt at 18% into your mortgage at 5-6% could save thousands in interest.

4. Better Loan Features or Shorter Term

Switch to offset accounts, revolving credit, or split fixed/floating structures for flexibility. Boost repayments by 5% annually (matching wage growth) to shave years off your term—e.g., a 30-year loan becomes 16 years.

It makes sense if savings exceed costs within your planned ownership timeline.

Costs of Refinancing: What Kiwis Need to Budget For

Refinancing isn't cost-free. Here's the 2026 breakdown for a typical switch:

| Cost Type | Estimated Amount | Notes |

|---|---|---|

| Break Fees (if fixed term not expired) | $1,000 - $10,000+ | Covers lender's lost interest; avoid by waiting for term end. |

| Legal Fees | $1,500 - $2,000 | Some banks cover; includes discharge and new mortgage registration with LINZ. |

| Valuation Fee | $500 - $1,000 | New lender may require a registered val. |

| Incentive Clawback | Varies | Repay cashbacks or rewards if within loyalty period. |

| Application/Other Fees | $200 - $500 | Credit checks, etc. |

Total: Often $3,000-$5,000. Use a mortgage calculator to check if a lower rate offsets this.

Step-by-Step Guide to Refinancing Your Mortgage in NZ

- Review Your Current Loan: Check fixed term end date, repayments, and documents. Chat with your bank about retention offers.

- Compare Deals: Use a broker for access to all banks. Look at rates, fees, cashbacks, and features.

- Get Pre-Approval: Gather payslips, bank statements, and budget. New lender assesses credit and income.

- Engage a Lawyer: They'll handle discharge, new docs, settlement, and LINZ registration.

- Settle: New funds repay old loan; contribute cash if borrowing less. Update Will, EPOA, and insurance.

- Post-Settlement: Confirm registration and start new repayments.

Timeline: 4-6 weeks. Start 2-3 months before fixed term ends.

Practical Tips for Kiwi Homeowners

- Negotiate Hard: Mention competitor offers—banks hate losing customers.

- Use a Broker: Free service, wider deals, no loyalty bias.

- Avoid Common Mistakes: Don't fixate on rate alone; budget all costs; don't over-borrow.

- Under Pressure? Talk to your bank early, trim spending, split loan types.

- 2026 Trend: Focus on break-even timing amid stable rates—refinance if savings hit 2 years or less.

Real Kiwi Examples: When It Worked (and When It Didn't)

Auckland couple on a $600k mortgage at 6.5% fixed (ending 2026) refinanced to 5.2% with $4,000 cashback. Costs: $2,500. Break-even: 18 months. Saved $15k over 5 years.

Christchurch family broke fixed early for debt consolidation—break fee $3k, but saved $500/month. Worth it. But a Dunedin homeowner ignored clawback, adding $2k unexpectedly.

"The best time is usually when your fixed-term rate is about to expire, as this avoids any break fees." — Blueprint Finance

Frequently Asked Questions

Related Articles

Using the NZ Mortgage Calculator to Plan Your House Hunt

Imagine spotting your dream home in Auckland or Christchurch, but wondering if you can actually afford it. That's where the NZ Mortgage Calculator comes in—your essential tool for turning house-huntin...

Mortgage Refixing Guide: How to Negotiate the Best Rate with Your Bank

Imagine slashing hundreds of dollars off your weekly mortgage payments just by knowing when and how to refix. With interest rates easing in 2026, thousands of Kiwis are facing refix decisions that cou...

How to Pay Off Your Mortgage Faster (NZ Strategies)

Imagine owning your home outright years earlier than planned, freeing up thousands in interest payments and giving you financial freedom sooner. For Kiwis with mortgages, paying off your home loan fas...

Mortgage Break Fees NZ: How Much Will It Cost to Switch?

Ever stared at your mortgage statement, dreaming of switching to a lower rate but frozen by the dreaded words "break fee"? You're not alone—thousands of Kiwis face this dilemma every year as interest...