Debt Consolidation: Does It Make Sense in NZ?

Struggling with multiple debts piling up? You're not alone—New Zealanders owe a staggering $608.7 billion in total debt as of late 2025, with personal consumer debt hitting $14.7 billion on credit car...

Sarah covers personal finance, tax, and KiwiSaver topics for Lifetimes NZ. She focuses on making money management straightforward and practical for everyday Kiwis.

Struggling with multiple debts piling up? You're not alone—New Zealanders owe a staggering $608.7 billion in total debt as of late 2025, with personal consumer debt hitting $14.7 billion on credit cards, car loans, and personal loans. If high-interest credit card balances, personal loans, and buy-now-pay-later schemes are overwhelming your budget, debt consolidation in NZ might offer a lifeline by combining them into one lower-rate loan.

This approach can simplify payments and potentially save on interest, but it's not a magic fix. With current 2026 rates like Westpac's special 11.95% p.a. debt consolidation loan, it's worth exploring if it fits your situation. Let's break down how it works, when it makes sense, and practical steps for Kiwis facing post-holiday or everyday debt stress.

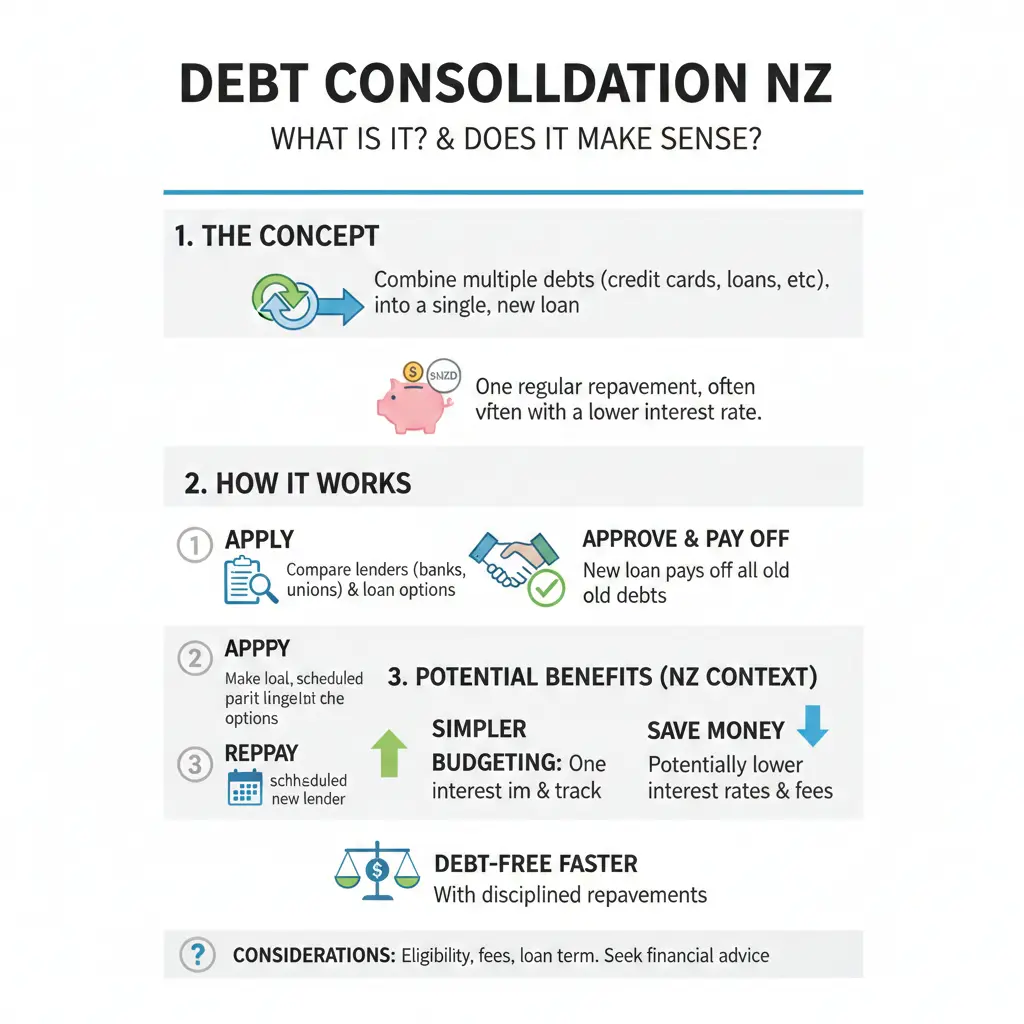

What is Debt Consolidation in New Zealand?

Debt consolidation involves taking out a single new loan to pay off multiple existing debts, such as credit cards at 19.7% interest or personal loans. The goal? Replace high-interest debts with one manageable payment at a lower rate, often from banks like Westpac, ANZ, or BNZ.

In NZ, these are typically unsecured personal loans up to $70,000, though secured options using your home equity exist if you own property. Unlike the US, our lenders follow strict Credit Contracts and Consumer Finance Act (CCCFA) rules, ensuring transparency on total costs and no hidden fees.

How Debt Consolidation Loans Work

- Assess your debts: Add up credit cards, overdrafts, car loans—anything non-mortgage.

- Apply for a loan: Banks check your credit score via Equifax and income stability.

- Pay off debts: The new loan funds clear your old ones directly.

- Repay monthly: Fixed terms from 1-7 years, with rates around 11-20% p.a. in 2026.

For example, Westpac's limited-time offer (January to April 2026) at 11.95% p.a. is fee-free for new applications, aimed at post-holiday stress where 28% of Kiwis worry about festive spending.

Current Debt Landscape in New Zealand (2026)

Our household debt averages $206,769, with personal debt at just 2.4% of the total pie but often the most painful due to high rates. Credit card debt lingers at 19.7%, while annual interest across all NZ debt tops $41 billion.

Post-Christmas blues hit hard: 23% of Westpac customers expect January/February bills like insurance (35%) and school supplies (14%) to add pressure, with 19% planning to use debt. Personal debt peaked at $16.8 billion in 2019 but sits at $14.7 billion now, thanks to tighter lending and buy-now-pay-later shifts—yet the remaining balances are high-cost.

Why Debt is Rising for Kiwis

- Housing dominance: $388.5 billion in mortgages (64% of debt), but consumer debt sneaks up on top.

- Cost of living: Inflation and rates have squeezed budgets since 2022.

- Holiday spending: 25% cite summer holidays as top January stress.

With net core Crown debt at 41.8% of GDP in 2024/25, government fiscal consolidation signals broader economic caution into 2026.

Pros and Cons of Debt Consolidation NZ

Does it make sense? It depends on your rates, discipline, and goals. Here's a balanced look:

| Pros | Cons |

|---|---|

| Lower interest: Swap 19.7% credit cards for 11.95% loans. | Longer terms could increase total interest paid. |

| One payment simplifies budgeting. | Temptation to re-accumulate debt on freed-up cards. |

| Potential credit score boost from closing accounts. | Fees and approval hurdles if credit is poor. |

| Fixed rates protect against hikes. | Not ideal for low-interest debts like mortgages. |

"Debt consolidation loans can help customers better manage their debt, reducing stress at a potentially difficult time of year."—Sarah Hearn, Westpac NZ Managing Director.

When Does Debt Consolidation Make Sense in NZ?

It shines if you have multiple high-interest debts (over 15%) and steady income. Prioritise: always tackle credit cards first over mortgages at 5-6%.

Ideal Scenarios

- Post-holiday overload: Consolidate $5,000 in cards at 20% into 11.95%—save hundreds yearly.

- 3+ debts: One repayment beats juggling due dates.

- Good credit: Secure rates under 13% p.a.

Warning Signs to Avoid It

- Poor credit: Rates could exceed current debts.

- Can't stop spending: You'll rack up new balances.

- Short-term debts: Pay off directly instead.

Calculate savings: For $10,000 at 19% over 3 years vs. 12% consolidated—use bank calculators. If total cost rises, skip it.

Steps to Consolidate Debt in New Zealand

Ready to act? Follow this Kiwi-focused plan:

Step 1: Get Your Free Credit Report

Check Equifax (equifax.co.nz) for errors—fix them to boost approval odds.

Step 2: List and Prioritise Debts

High-interest first. Use MoneyHub's debt calculator for insights.

Step 3: Shop Around Lenders

- Banks: Westpac (11.95% special to May 2026), ANZ, ASB.

- Non-banks: Harmoney, Lombard—often faster but higher rates.

- Credit unions: Lower fees for members.

Step 4: Apply and Compare Offers

Provide payslips, bank statements. CCCFA requires full disclosure of establishment fees (up to 5%) and rates.

Step 5: Cut Up Cards and Budget

Destroy old cards post-consolidation. Use Sorted.org.nz for free budgeting tools.

Alternatives if Consolidation Isn't Right

- No Interest Now (NINA): For essentials, 0% over 10 weeks.

- Debt helplines: MoneyTalks (0800 345 123) for free advice.

- Hardship plans: Negotiate with creditors under CCCFA.

- Financial Mentoring: Free via CAB (citizensadvicebureau.net.nz).

Real NZ Example: Sarah's Debt Consolidation Success

Sarah from Auckland had $15,000 across two credit cards (19.5%) and a car loan (14%). Monthly minimums ate 25% of her income. She consolidated into a Westpac loan at 12.5% over 4 years—payments dropped 30%, saving $2,800 in interest. With a strict no-card rule, she's debt-free by 2028.

(Based on typical 2026 scenarios; individual results vary.)

Next Steps to Tackle Your Debt

Don't let debt dominate 2026—start today. Pull your Equifax report, list debts, and compare lenders like Westpac's offer (ends May). Track spending with apps like PocketSmith, build an emergency fund, and consider free mentoring from CAB or Sorted.

If consolidation fits, you'll breathe easier with one payment and lower costs. If not, prioritise high-interest payoffs. You're in control—kiwis have reduced personal debt before, and 2026 can be your turnaround year.

Frequently Asked Questions

Sources & References

-

1

New Zealand Debt Statistics 2025 - $608.7 Billion Owed - MoneyHub — www.moneyhub.co.nz

- 2

-

3

Budget Policy Statement 2026 — www.treasury.govt.nz

-

4

Post-holiday debt? Westpac launches special consolidation interest rate — www.nzherald.co.nz

-

5

Get your finances sorted in 2026: Get rid of debt — www.rnz.co.nz

-

6

Global Credit Trends | Equifax New Zealand — www.equifax.co.nz