Mortgage Top-Ups: Using Your Home Equity for Other Purposes

Imagine transforming your Kiwi dream home with a sleek new kitchen or a sunlit extension—all funded without the hassle of a new loan application. That's the power of mortgage top-ups, letting you tap...

Sarah covers personal finance, tax, and KiwiSaver topics for Lifetimes NZ. She focuses on making money management straightforward and practical for everyday Kiwis.

Imagine transforming your Kiwi dream home with a sleek new kitchen or a sunlit extension—all funded without the hassle of a new loan application. That's the power of mortgage top-ups, letting you tap into your home's equity for renovations, debt consolidation, or big life goals. In New Zealand's dynamic property market, where home values often outpace repayments, this strategy offers flexibility and lower rates than unsecured borrowing.

As we navigate 2026's improving interest rates and relaxed lending rules, more homeowners are unlocking equity built over years of ownership.Mortgage top-ups: using your home equity for other purposes has never been more accessible, but it demands smart planning to avoid stretching your finances thin. This guide breaks it down with practical steps, lender insights, and Kiwi-specific tips to help you decide if it's right for you.

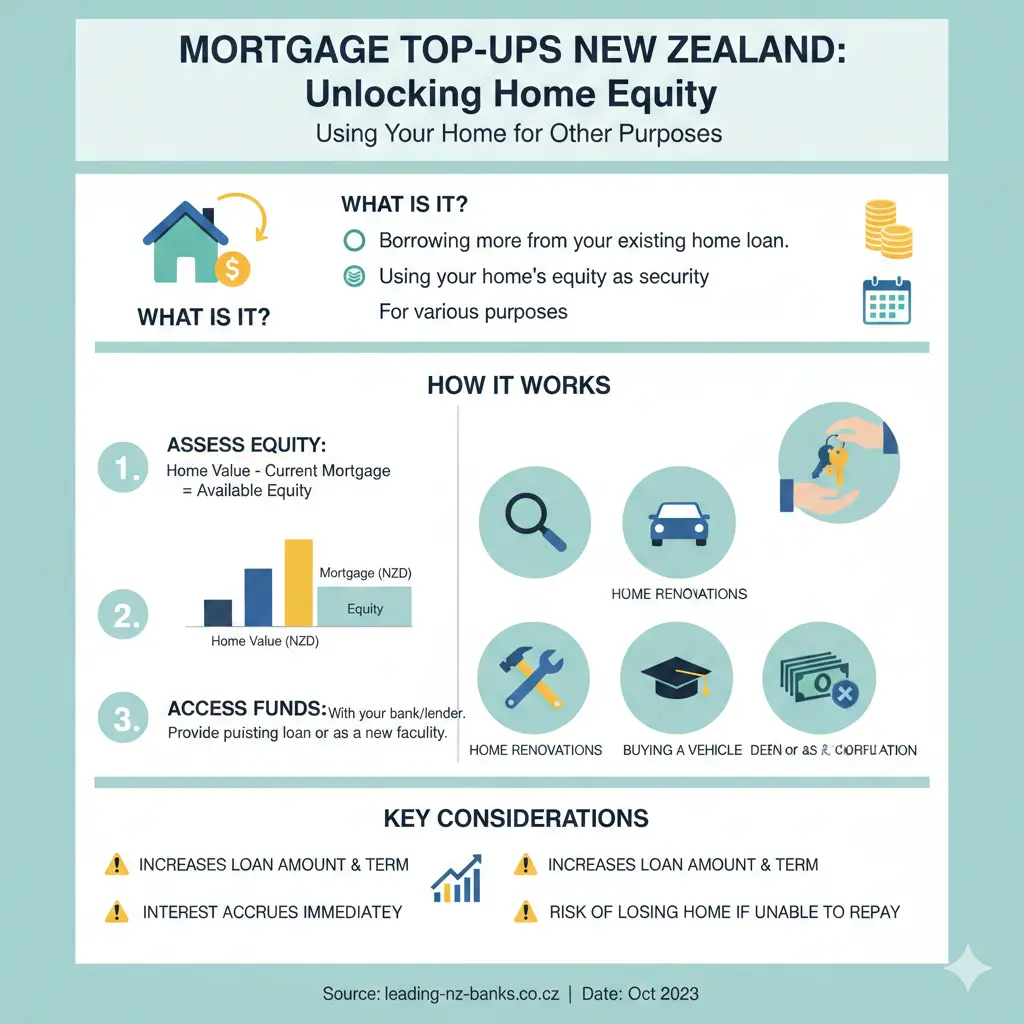

What Is a Mortgage Top-Up in New Zealand?

A mortgage top-up is an additional borrowing option that lets homeowners increase their existing home loan to access extra funds, secured against their property's equity. Unlike starting a new loan, it extends your current mortgage, often at competitive rates because it's backed by your home's value.

In New Zealand, equity builds as property values rise—think Auckland's steady appreciation or regional booms in Canterbury—and you pay down principal. If your home is now worth $1 million with $600,000 owing, you've got $400,000 in equity. Lenders typically let you borrow up to 80-90% of that value, minus your current loan, subject to affordability checks.

Common uses include home renovations that boost value, consolidating high-interest debts like credit cards (averaging 20%+ interest), or funding education via KiwiSaver withdrawals paired with a top-up. It's not free money— you're adding to your mortgage, so repayments rise—but with OCR cuts in 2026, timing could be ideal.

Key Benefits of Using Home Equity This Way

- Lower interest rates: Secured loans often sit at 5-6% in 2026, versus 10-20% for personal loans.

- Tax advantages: Interest on top-ups for income-producing investments may be deductible via IRD rules—check with an adviser.

- Simplicity: No new loan setup if with the same lender; faster approval than full applications.

- Flexibility: Funds for renovations that add value, like insulation upgrades qualifying for government grants.

Types of Mortgage Top-Ups for Kiwi Homeowners

New Zealand banks offer varied top-up structures to match your needs, from renovations to investments. Choosing the right type aligns with cash flow and goals.

Table Loans and Fixed Top-Ups

A table top-up adds a lump sum to your principal, repaid steadily like your original loan. Ideal for one-off renovations, say $50,000 for a bathroom reno. BNZ charges up to $100 for existing customers on standard loans.

Revolving Credit and Offset Options

Revolving credit lets you draw down and repay flexibly, suiting irregular renovation costs. Offset mortgages link a savings account to reduce interest—top up for a project, then offset with savings. Great for debt consolidation, paying off WINZ debts faster.

Specialised Renovation Finance

Some lenders offer staged releases for builds, tied to progress valuations. With RBNZ's 2026 LVR loosening—25% of owner-occupier lending now under 20% deposit—this eases top-ups for equity-rich homes.

Pro Tip: Compare via a broker; Westpac's 2026 commission changes mean upfront fees stabilise at 0.90% for new settlements.

Lender Criteria and Eligibility in 2026

Banks must follow responsible lending laws, scrutinising your finances thoroughly. Expect checks on income, debts, credit score, and debt-to-income (DTI) ratio—aim under 6x gross income.

What You'll Need to Apply

- Proof of income: 3 months' payslips, IRD tax summary.

- Bank statements: Last 6 months, showing spending habits.

- Property details: Recent valuation (lender may order one, ~$500).

- Purpose evidence: Builder quotes, plans for renos adding 10-20% value.

- Equity proof: At least 20% after top-up; low-equity margins (0.5-1% extra interest) may lift if values rose.

First-home buyers or recent purchasers benefit from 2026's 'Goldilocks' market—more low-deposit approvals spill over to top-ups. Investors note: High-LVR eased to 10% under 30% deposit.

Step-by-Step Process for a Mortgage Top-Up

Streamlined for existing customers, but plan 4-8 weeks.

- Assess equity: Use online calculators or broker to estimate borrowing power.

- Gather docs: Financials and project plans.

- Contact lender/broker: Submit application; expect credit check.

- Valuation and approval: Lender appraises home; if reno boosts value, it strengthens case.

- Funds release: Lump sum or staged; sign docs, pay fees ($100-150).

- Repay: Integrated into mortgage; refix soon? Shop 2026 lows.

Costs, Risks, and Pitfalls to Avoid

Top-ups save on rates but add to total debt. Break fees apply if fixed-term; refixing in 2026 could hike payments $200-600/month on large loans.

Hidden Costs

- Fees: $100-150 top-up, $500+ valuation.

- Interest: Extra $10k borrowed at 5.5% adds ~$550/year initially.

- Low-equity premium: Negotiate removal if equity improved.

Risks and How to Mitigate

- Overborrowing: Stress-test at 7% rates; use IRD's loan calculator.

- Property dips: Equity buffer protects; don't top to 95% LVR.

- Life changes: ACC or job loss? Build emergency fund first.

- Pitfall: Renovations not adding value—get quotes showing ROI.

Disclaimer: This isn't personalised financial advice. Consult a licensed adviser or use sorted.org.nz for your situation.

Real Kiwi Examples: Mortgage Top-Ups in Action

In Auckland, Sarah topped up $80k for insulation and solar—value rose 15%, offsetting costs via energy savings and grants. A Canterbury couple consolidated $30k credit card debt, slashing interest from 19% to 5.7%, freeing cash for KiwiSaver boosts.

With 2026 refixes, proactive top-ups before rates drop maximise equity.

Next Steps to Unlock Your Home Equity

Ready to leverage your equity? Start with a free equity calculator on bank sites, then chat to a mortgage adviser via mortgages.co.nz. Review your finances holistically—factor KiwiSaver, IRD tax position, and ACC cover. Compare offers, stress-test repayments, and ensure the top-up aligns with long-term goals like retirement or family needs.

Smart use of mortgage top-ups: using your home equity for other purposes builds wealth; mismanaged, it risks stress. Seek professional advice tailored to you.

Frequently Asked Questions

Sources & References

-

1

Mortgage Top Ups: Renovation Finance for Kiwis — mortgagemanagers.co.nz

-

2

Westpac NZ confirms end to trail commissions next year — www.theadviser.com.au

-

3

New mortgage rules…what do they mean — castletrust.co.nz

-

4

Get your finances sorted in 2026: Manage your mortgage — www.rnz.co.nz

-

5

Why 2026 is a 'Goldilocks year' for first-home buyers — www.1news.co.nz

-

6

Better Future home loan top-ups - BNZ — www.bnz.co.nz

-

7

Mortgage Refix Shock NZ 2026 — Payments Could Jump $200–$600 a Month — www.artbeat.org.nz

-

8

The good news for mortgage holders — www.nzherald.co.nz

-

9

Refixing in 2026: A Decision Framework — www.newzealandmortgages.co.nz

Related Articles

Industry Bodies and Professional Associations NZ

Whether you're launching a business, advancing your career, or navigating financial regulations, industry bodies and professional associations in New Zealand offer invaluable support. These organisati...

Emergency Benefit NZ: When You Have No Other Options

When you're struggling financially and don't qualify for other benefits, the Emergency Benefit might be your lifeline. It's a discretionary payment designed for Kiwis in genuine hardship who've exhaus...

Unpaid Internships NZ: Are They Legal?

Unpaid internships are a common pathway for students and graduates to gain work experience in New Zealand, but there's often confusion about whether they're actually legal. The short answer is: unpaid...

Estate Administration NZ: Managing Someone's Affairs After Death

Losing a loved one is one of life's toughest challenges, and stepping in to manage their estate can feel overwhelming. In New Zealand, estate administration—the process of handling someone's affairs a...