LVR Rules NZ Explained: Loan-to-Value Ratio Requirements

If you're thinking about buying a home or investment property in New Zealand, you've probably heard the term "LVR" thrown around by banks and mortgage brokers. But what does it actually mean, and how...

Sarah covers personal finance, tax, and KiwiSaver topics for Lifetimes NZ. She focuses on making money management straightforward and practical for everyday Kiwis.

If you're thinking about buying a home or investment property in New Zealand, you've probably heard the term "LVR" thrown around by banks and mortgage brokers. But what does it actually mean, and how does it affect your ability to get a mortgage? Understanding Loan-to-Value Ratio (LVR) rules is essential for anyone planning to borrow money to purchase property, because these Reserve Bank restrictions directly determine how much deposit you'll need and whether a bank will lend to you at all.

What Is LVR and Why Does It Matter?

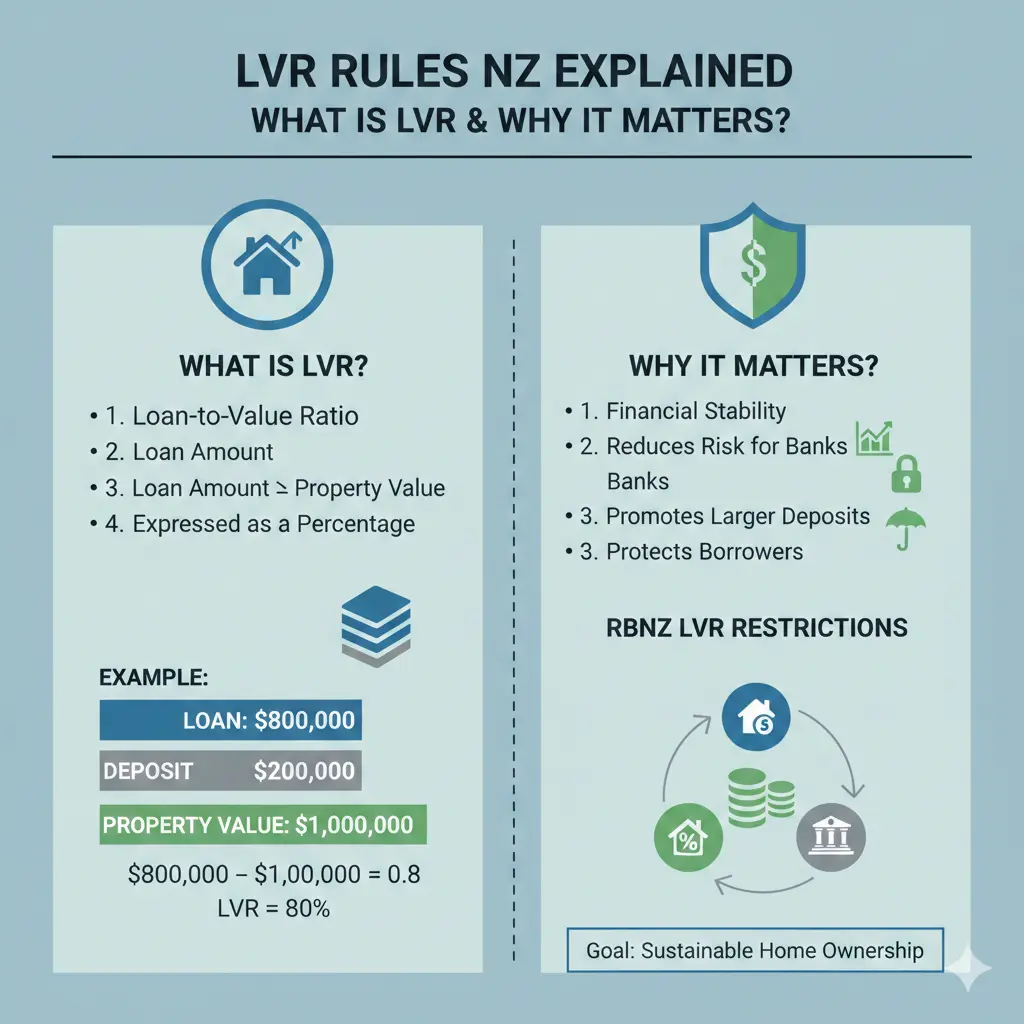

The Loan-to-Value Ratio is simply the percentage of your mortgage compared to the value of your property. The Reserve Bank of New Zealand sets LVR restrictions to decide the minimum deposit you need to get a mortgage and to keep our financial system stable.

Here's a practical example: if you want to buy a home valued at $500,000 and the bank can lend you up to 80% of the property's value, that means the bank will lend you $400,000. The remaining $100,000 (20%) is your deposit.

These rules matter because they determine whether you can actually qualify for a mortgage and how much you'll need to save before you can buy. Without understanding LVR requirements, you might think you're ready to buy when you're actually short on your deposit.

Current LVR Requirements in 2026

The LVR landscape changed significantly on 1 December 2025, with the Reserve Bank relaxing some restrictions to help first-home buyers access the property market. Here's what you need to know about current requirements:

For Owner-Occupiers (Home Buyers)

If you're buying your own home, the standard requirement is straightforward:

- Existing property: 20% deposit required (bank lends 80%)

- New Build: 20% deposit required (bank lends 80%)

However, there's a small window for first-home buyers with smaller deposits. From 1 December 2025, banks can now lend up to 25% of their new home loans to owner-occupiers with deposits under 20%, up from the previous 20%. This means if you have a 10-15% deposit, you have a slightly better chance of being approved, though it's not guaranteed.

For Property Investors

Investors face stricter requirements than owner-occupiers:

- Existing property: 30% deposit required (bank lends 70%)

- New Build: 20% deposit required (bank lends 80%)

From 1 December 2025, the limit for low-deposit lending to investors also increased, from 5% to 10%. This means slightly more investors with deposits between 20-30% may now be approved.

The New Build Advantage

One significant difference exists for new builds: technically, no LVR restrictions apply to new builds. In practice, this means investors can buy a new investment property with just a 20% deposit instead of the usual 30% required for existing properties. This can make new builds considerably more attractive for property investors looking to expand their portfolio.

How LVR Restrictions Changed in 2025

The Reserve Bank made meaningful changes to LVR rules starting 1 December 2025. The key shift was moving from strict deposit requirements to a more flexible approach that focuses on how much of a bank's total lending can go to low-deposit borrowers.

This distinction is important: your personal deposit requirement hasn't changed dramatically, but more borrowers with smaller deposits now have a realistic chance of approval because banks have more "room" in their lending portfolios for low-deposit loans.

The change also preserves financial stability by maintaining strict debt-to-income (DTI) ratio restrictions. Even if you have a smaller deposit, banks will carefully assess whether you can actually afford the mortgage payments.

Calculating Your Purchasing Power Under LVR Rules

Understanding how much property you can actually afford requires a simple calculation. If you know your deposit amount, you can work out your maximum purchasing power using this formula:

Your Deposit ÷ Deposit Required % = Maximum Purchasing Power

Let's say you're an owner-occupier with a $150,000 deposit. You need a 20% deposit, so:

$150,000 ÷ 0.20 = $750,000 maximum purchasing power

This means you could potentially buy a property valued at up to $750,000, with the bank lending you $600,000 and you contributing your $150,000 deposit.

For an investor with the same $150,000 deposit wanting to buy an existing property, the calculation differs because you need a 30% deposit:

$150,000 ÷ 0.30 = $500,000 maximum purchasing power

The 10% difference in deposit requirements significantly reduces your purchasing power as an investor compared to an owner-occupier.

Special Circumstances and Exceptions

First-Home Buyers

First-home buyers have been given more flexibility since the December 2025 changes. While the typical 20% deposit is still preferred, banks now have greater capacity to approve first-home buyers with 10-15% deposits. However, this doesn't mean it's automatic—you'll still need to pass affordability checks under DTI rules.

Healthy Homes Act Requirements

There's an interesting exception for investors: if you're buying an existing rental property that doesn't meet Healthy Homes Act standards, your bank may lend you additional funds to bring the property up to code. This can help you avoid needing a larger deposit in the first place.

Moving to a New Home

If you're already a homeowner moving to a new property, you may be able to take your existing mortgage with you without triggering LVR restrictions, as long as you're moving to a new main residence. However, if you want to increase your loan amount and the increase would push your LVR above 80%, you'll face LVR restrictions on the additional borrowing.

Why the Reserve Bank Sets These Rules

LVR restrictions exist for a reason: they help keep New Zealand's financial system stable. By requiring borrowers to have "skin in the game" (a meaningful deposit), the Reserve Bank reduces the risk of widespread mortgage defaults during economic downturns.

The rules can change depending on economic conditions. For example, LVR restrictions were removed entirely in April 2020 during the COVID-19 pandemic response, but were brought back in March 2021 as house prices skyrocketed. The most recent changes in December 2025 reflect a deliberate policy decision to ease lending while maintaining financial stability through DTI restrictions.

Next Steps: Planning Your Property Purchase

Understanding LVR rules is just the first step. Here's what you should do next:

- Calculate your deposit: Work out how much you've currently saved and how much more you need to reach your target deposit percentage.

- Check your purchasing power: Use the formula above to understand what price range of property you can realistically afford given your deposit and LVR requirements.

- Get a mortgage pre-approval: Talk to a bank or mortgage broker to understand your personal borrowing capacity, including DTI assessments. This gives you a realistic picture before you start house hunting.

- Consider your property type: If you're an investor, weigh up whether a new build might offer better deposit terms than an existing property.

- Seek professional advice: A mortgage adviser or financial adviser can help you navigate the rules specific to your situation and ensure you're making the best decision for your circumstances.

The December 2025 changes to LVR rules represent a genuine easing of lending restrictions for first-home buyers and investors, but they don't mean you can skip saving for a deposit. Understanding these rules puts you in control of your property-buying journey and helps you plan realistically for one of New Zealand's biggest financial decisions.

Frequently Asked Questions

Sources & References

-

1

Loan-to-Value Ratio (LVR) Restrictions in New Zealand — www.opespartners.co.nz

-

2

Understanding different loan to value ratios - BNZ — www.bnz.co.nz

-

3

Bank Lending Rules Update 2025: Key Changes and Future Outlook — easymortgage.co.nz

-

4

News in Focus: What the New LVR Rules Mean for First-Home Buyers — blog.healthcareplus.org.nz

-

5

Loan-to-Value Ratio Explained: What LVR Means for Your Deposit — capitaladvice.co.nz

-

6

LVR Rules Explained: Deposits, Low-Equity Lending, and What Changed from 1 December 2025 — www.newzealandmortgages.co.nz

-

7

Loan-to-value ratios | Home loans — www.kiwibank.co.nz

Related Articles

Industry Bodies and Professional Associations NZ

Whether you're launching a business, advancing your career, or navigating financial regulations, industry bodies and professional associations in New Zealand offer invaluable support. These organisati...

Emergency Benefit NZ: When You Have No Other Options

When you're struggling financially and don't qualify for other benefits, the Emergency Benefit might be your lifeline. It's a discretionary payment designed for Kiwis in genuine hardship who've exhaus...

Unpaid Internships NZ: Are They Legal?

Unpaid internships are a common pathway for students and graduates to gain work experience in New Zealand, but there's often confusion about whether they're actually legal. The short answer is: unpaid...

Estate Administration NZ: Managing Someone's Affairs After Death

Losing a loved one is one of life's toughest challenges, and stepping in to manage their estate can feel overwhelming. In New Zealand, estate administration—the process of handling someone's affairs a...