Landlord Insurance NZ: Protecting Your Investment Property

Imagine coming home to discover your prized investment property in Auckland has been trashed by tenants—walls punched, carpets ruined, and worst of all, no rent coming in for months while you foot the...

Sarah covers personal finance, tax, and KiwiSaver topics for Lifetimes NZ. She focuses on making money management straightforward and practical for everyday Kiwis.

Imagine coming home to discover your prized investment property in Auckland has been trashed by tenants—walls punched, carpets ruined, and worst of all, no rent coming in for months while you foot the repair bills. For Kiwi landlords, this nightmare is all too real, but landlord insurance NZ can be your safety net, protecting your investment property from financial disaster.

With New Zealand's rental market booming—over 40% of Kiwis rent, according to Stats NZ—more people are turning to property investment.Landlord insurance NZ: protecting your investment property isn't just a nice-to-have; it's essential cover tailored for when your home is tenanted. Unlike standard home insurance, it tackles unique risks like loss of rent, tenant damage, and meth contamination. In this guide, we'll break down what you need to know for 2026, including key covers, top providers, and practical tips to keep your policy valid.

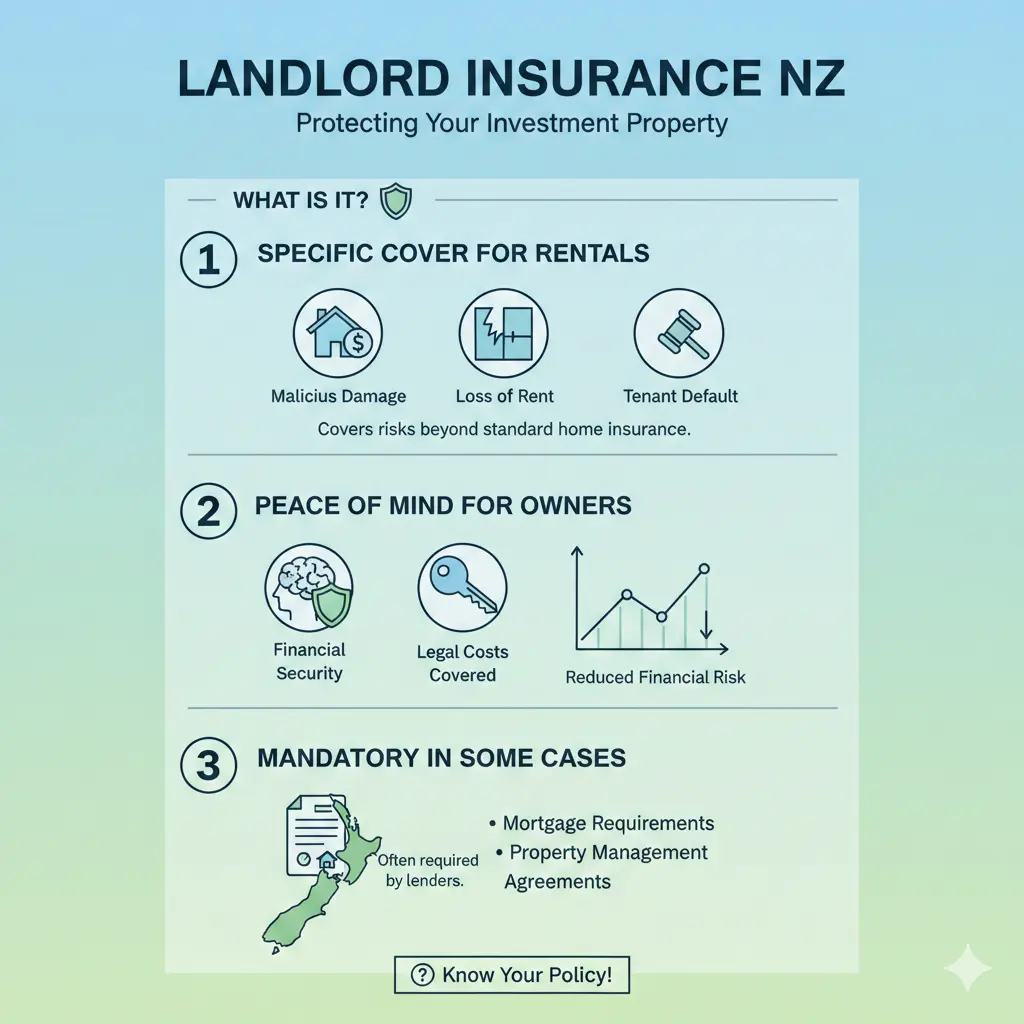

What is Landlord Insurance in New Zealand?

Landlord insurance is specialist cover designed for property owners renting out their homes. It protects the building, any landlord-provided contents like whiteware or curtains, and your income stream from rent. Standard home insurance often excludes tenant-related risks, leaving you exposed if disaster strikes.

Under the Residential Tenancies Act 1986 (updated in recent years), landlords must maintain habitable properties, but tenants can still cause issues. Landlord policies step in where tenancy laws don't, covering events like fires, floods, or deliberate damage. Most insurers require you to select tenants carefully, reference-check them, and lodge a bond with Tenancy Services to keep cover active.

Key Differences from Standard Home Insurance

- Loss of rent: Pays if your property becomes uninhabitable—up to 12 months or $40,000 with some providers.

- Tenant damage: Covers malicious acts by tenants or guests, often up to $30,000.

- Landlord contents: Protects appliances and fittings you supply, typically $5,000–$20,000.

- Meth contamination: Clean-up costs up to $50,000 while tenanted.

- Liability: Up to $20 million for injuries or damage under the Health and Safety at Work Act 2015.

These features make landlord insurance vital for protecting your investment property in NZ's high-risk environment, from earthquakes to unruly tenants.

Essential Covers in Landlord Insurance NZ Policies

Choosing the right policy means matching cover to your risks. Here's what top 2026 policies offer.

Building and Natural Disaster Cover

Your rental's structure is covered for fire, storms, burglary, and natural hazards like earthquakes and floods. From 1 July 2024, the Natural Hazards Insurance Act 2023 means the Natural Hazards Commission (NHC) covers the first $345,000 (including GST) of qualifying damage. Landlord insurers like Initio provide top-up cover up to your sum insured.

Vero's Maxi + Landlord’s Extension includes natural hazards, while AA Insurance covers earthquakes, landslides, and tsunamis.

Loss of Rent Protection

If a covered event makes your property uninhabitable, expect payouts for lost rent:

- Vero: Up to 12 months, capped at $40,000 (Maxi) or $20,000 (Flexi).

- Tower: Up to 8 months if uninhabitable; 8 weeks for non-payment or eviction.

- Initio/MoneyHub quotes: Typically $20,000 cap, but Christchurch quakes and Cyclone Gabrielle showed repairs can take longer.

Non-payment cover often requires lawful eviction processes via the Tenancy Tribunal.

Tenant-Related Risks

Deliberate damage by tenants? Vero covers up to $30,000; Tower up to $20,000 per event (with $500 excess). Meth clean-up is crucial in NZ—Vero up to $50,000, Tower $30,000.

Contents and Liability

Landlord furnishings (whiteware, curtains) get $20,000 with Tower or Vero Maxi, $5,000 with Flexi. Public liability reaches $20 million, shielding you from lawsuits.

AMP adds gradual water damage and meth losses, plus optional SumExtra for rebuild cost hikes.

2026 Landlord Insurance Costs and Quotes

Premiums vary by location, property value, and excess. For a $1.3M Auckland property:

| Provider | Annual Premium | Excess | Rating |

|---|---|---|---|

| AA | $3,278.44 | $1,150 | Very Strong |

| Another | $4,669.78 | $1,000 | Strong |

| Initio | $2,656.29 | $650 | Best Value |

| Tower | $2,845.56 | Varies | Competitive |

MoneyHub's 2026 picks highlight Initio for value ($2,411–$3,704 across scenarios) with replacement value, $20,000 loss of rent, and contents. Shop via comparison sites for the best deal.

Good news: Premiums are tax-deductible as a rental business expense via IRD.

Common Exclusions and How to Avoid Claims Pitfalls

No policy covers everything. Watch for:

- Vacant properties: Most void cover after 60–90 days unoccupied. Update your insurer immediately—failure is "misrepresentation" under the Contracts of Insurance Act 2024.

- Tenant selection: No reference checks or bonds? Claims denied.

- Unreported changes: Tenants leave? Notify to avoid voids.

Practical Tips for Kiwi Landlords

- Download your insurer's landlord guide (e.g., Vero's) for obligations like regular inspections.

- Lodge bonds and use Tenancy Services for disputes.

- Choose higher excesses to lower premiums if you're low-risk.

- Bundle with KiwiSaver or bank insurance (ASB, BNZ updating for 2026).

- Review annually—rebuild costs rise with inflation.

Choosing the Best Landlord Insurance Provider in NZ

Compare Vero (comprehensive Maxi), Tower (forward-thinking with 20% fire extra), Initio (top-up natural hazards), and others like AA, AMP, ASB. Use MoneyHub for quotes from AMI, AMP, State, and more. Look for Financial Strength Ratings (AA Very Strong best).

Next Steps to Protect Your Investment

Don't leave your rental exposed—get quotes today from Initio, Tower, or Vero, compare via MoneyHub, and ensure you're compliant with tenancy checks. Contact Tenancy Services for bond lodgement and download a landlord guide. With the right landlord insurance NZ: protecting your investment property, you can sleep easy knowing your Kiwi dream home is secure. Start by reviewing your current cover or grabbing a free quote online.

Frequently Asked Questions

Sources & References

-

1

Landlord Insurance New Zealand - Tower Insurance — www.tower.co.nz

-

2

We've made landlord insurance simple | Vero — www.vero.co.nz

-

3

Buy Landlord Insurance Online Today — Initio — initio.co.nz

-

4

NZ Landlord Guide 2026: Navigating Vacant Property Insurance — quashed.co.nz

-

5

Compare Landlord Insurance - MoneyHub NZ — www.moneyhub.co.nz

- 6

-

7

Landlord Insurance - AA Insurance — www.aainsurance.co.nz

-

8

Landlord insurance - ASB Bank — www.asb.co.nz

-

9

Insurance cover for landlords - BNZ — www.bnz.co.nz

Useful Tools

Related Articles

Life Insurance NZ: Are You Overpaying for Cover You Don't Need?

Ever signed up for life insurance without a second thought, only to watch your premiums climb year after year? You're not alone—many Kiwis are paying for life insurance NZ cover they don't actually ne...

Health Insurance NZ: Complete Guide to Going Private

Imagine facing a sudden health scare in New Zealand—long public hospital waits could stretch weeks or months, but with private health insurance, you could access top specialists and private rooms swif...

Travel Insurance NZ: What to Look For Before You Go

Picture this: you're hiking the Tongariro Crossing, the mist rolling off the emerald lakes, when a sudden twist of ankle leaves you stranded. No worries if you've got the right travel insurance NZ—but...

Pet Insurance NZ 2025: Is It Worth the Cost?

Imagine coming home to your loyal labrador, only to find them limping after a sudden accident. A trip to the vet reveals surgery costs over $5,000—money you hadn't budgeted for. This scenario plays ou...