Life Insurance NZ: Are You Overpaying for Cover You Don't Need?

Ever signed up for life insurance without a second thought, only to watch your premiums climb year after year? You're not alone—many Kiwis are paying for life insurance NZ cover they don't actually ne...

Sarah covers personal finance, tax, and KiwiSaver topics for Lifetimes NZ. She focuses on making money management straightforward and practical for everyday Kiwis.

Ever signed up for life insurance without a second thought, only to watch your premiums climb year after year? You're not alone—many Kiwis are paying for life insurance NZ cover they don't actually need, leaving money on the table that could go towards family holidays or KiwiSaver top-ups.

In today's fast-changing financial landscape, with market consolidation and new laws like the Contracts of Insurance Act 2024 rolling out, it's time to check if your policy still fits. This guide breaks down how to spot if you're overpaying, what cover you truly need, and practical steps to save without skimping on protection.

Understanding Life Insurance in New Zealand

Life insurance in NZ provides a payout to your family or dependants if you pass away or suffer a covered event like critical illness. It's not one-size-fits-all—policies range from basic death cover to comprehensive plans bundling trauma, income protection, and disability. But with Kiwis increasingly favouring flexible, comprehensive options, it's easy to end up with extras that overlap with what you already have.

The market is valued at around $3.9 billion in 2025, with modest 0.5% growth that year after a -3.8% CAGR dip from 2020-2025. Competition is fierce, especially post-consolidation where big players like AMI, State, and OnePath exited, boosting specialist insurers. Premiums are GST-exempt, and upcoming regs will hike the probate-free payout limit to $40,000.

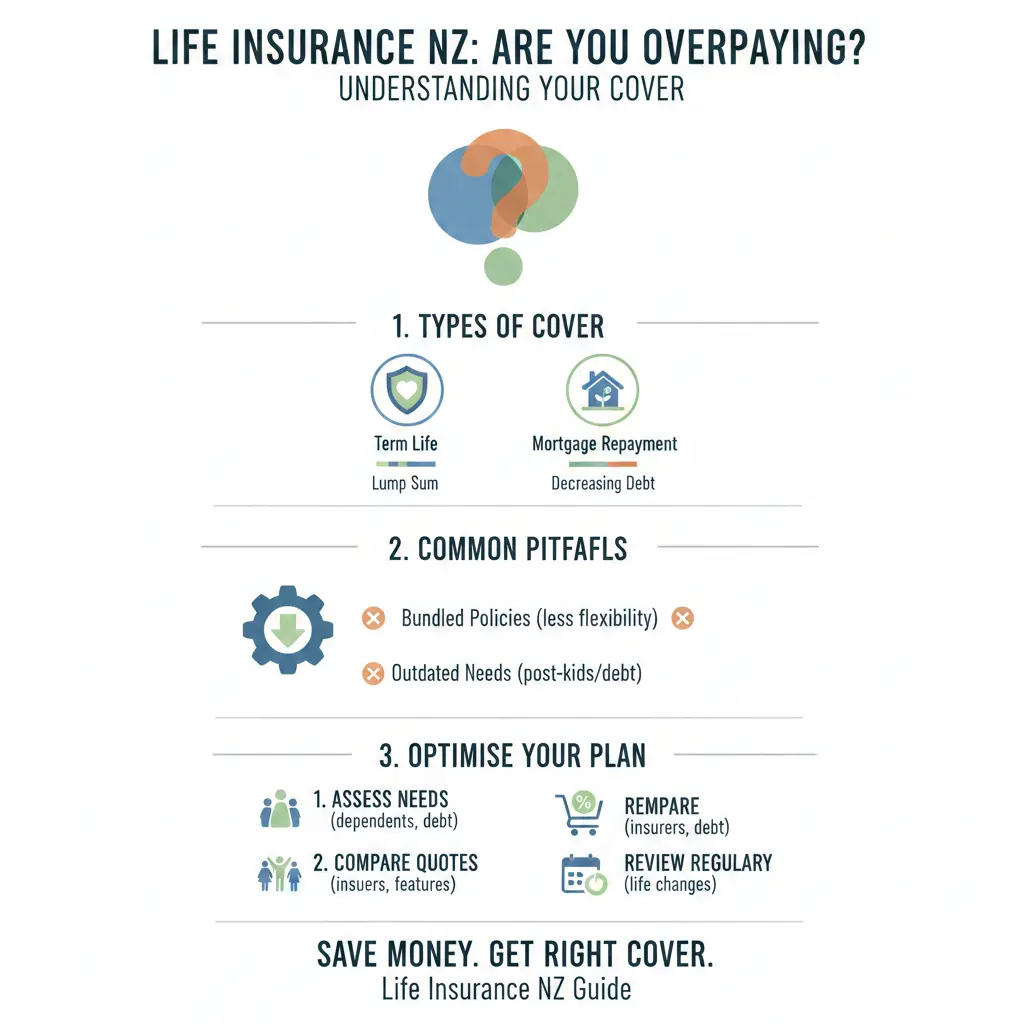

Types of Life Insurance Policies Available

- Term Life: Covers you for a set period (e.g., until mortgage paid off). Cheapest option, pure death benefit.

- Whole of Life: Lifetime cover, builds cash value—pricier but guarantees payout.

- Mortgage Protection: Repays your home loan on death—often decreasing cover, but beware overlaps with full life policies.

- Trauma/Critical Illness: Lump sum for serious conditions like cancer.

- Income Protection: Replaces earnings if illness or injury sidelines you.

Many Kiwis mix these, but bundling can lead to over-insuring if your needs change—like kids leaving home or mortgage nearing end.

Signs You're Overpaying for Life Insurance NZ

If your premiums feel like a growing burden, dig deeper. Here are red flags that scream "cover you don't need":

1. Premiums Rising Faster Than Expected

Stepped premiums start low but jump 2-15% yearly with age. A 35-year-old pays ~$400/year for $500k cover, ballooning to $970 by 65. Level premiums lock in rates (e.g., $800/year fixed), better for long-term but higher upfront. If you're on stepped and nearing retirement, switch to avoid shocks.

2. Cover Exceeds Your Real Needs

Calculate your sum assured: mortgage balance + 10x annual income - liquid assets like KiwiSaver. Got $1m cover but only $300k debt and $200k savings? You're overpaying. Tools from Financial Services Providers (FSPs) help assess this.

3. Duplicate Coverage from Group Schemes

Workplace or KiwiSaver life cover (often 3-4x salary via default providers) plus personal policy? That's overlap. Check your employer's scheme first—it's cheaper but may lapse if you leave.

4. Lifestyle Changes Ignored

Divorced? Kids independent? Mortgage halved? Policies don't auto-adjust. With NZ's housing market stabilising in 2026, many are still paying for yesterday's needs.

5. Not Shopping Around in a Competitive Market

Prices are at all-time lows thanks to comparison sites and specialist insurers gaining share post-2025 mergers. Smokers/vapers pay 3-4x more (~$1,500/year for 50-year-old on $500k), but quitting drops rates fast.

How Much Life Insurance Do Kiwis Really Need?

Rule of thumb: Enough to clear debts, replace income for 5-10 years, and fund education. For a family of four with $800k mortgage and $100k income:

| Age | Recommended Cover ($500k Example) | Annual Premium (Non-Smoker) |

|---|---|---|

| 30 | $400 | |

| 50 | $1,500 | |

| 55 | $2,000 |

Adjust for ACC (covers accidents, not illness) and WINZ benefits. Use online calculators from sites like MoneyHub, but consult an authorised adviser registered with the Financial Markets Authority (FMA).

Practical Tips to Avoid Overpaying

- Review Annually: Life changes—reassess cover. With Contracts of Insurance Act 2024 implementation in 2026, disclosure duties simplify claims.

- Compare Quotes: Use sites comparing AIA, Fidelity Life, and nib. Save 20-30% switching.

- Choose Level Over Stepped for Long-Term: Locks costs, ideal until kids fly the nest.

- Leverage Health Discounts: Non-smoker? Gym-goer? Many offer 10-20% off.

- Bundle Smartly: Combine with trauma if needed, but ditch mortgage-only if you have full term life.

- Check Exclusions: Pre-existing conditions? Ensure policy aligns—declined claims rose recently.

Pro tip: RBNZ-licensed insurers must meet governance standards—stick to them for security.

New Zealand-Specific Considerations

Our no-fault ACC system covers accidental death/injury, so life insurance fills gaps for illness. KiwiSaver often includes free death benefit—don't double up. Post-2026, new regs standardise policyholder duties and boost consumer protections. For Māori or Pasifika families, culturally sensitive advice from community providers can tailor cover.

Next Steps: Take Control Today

Grab your policy docs, tally debts/income, and get 3+ quotes. Chat with an FMA-registered adviser (free initial consults common) or use comparison tools. In 2026's stable market (AM Best outlook steady), trimming excess cover could save hundreds yearly—money better spent on whānau.

Don't let overpayment steal your future security. Act now for peace of mind.

Frequently Asked Questions

Sources & References

-

1

Life insurance - New Zealand | Statista Market Forecast — www.statista.com

-

2

Life Insurance in New Zealand Market Size Statistics - IBISWorld — www.ibisworld.com

-

3

Insurance & Reinsurance 2026 - New Zealand — practiceguides.chambers.com

-

4

Compare Life Insurance NZ 2025: Best Policies, Quotes & ... — www.moneyhub.co.nz

-

5

Market Segment Outlook: New Zealand Life Insurance - AM Best — www3.ambest.com

Related Articles

Health Insurance NZ: Complete Guide to Going Private

Imagine facing a sudden health scare in New Zealand—long public hospital waits could stretch weeks or months, but with private health insurance, you could access top specialists and private rooms swif...

Travel Insurance NZ: What to Look For Before You Go

Picture this: you're hiking the Tongariro Crossing, the mist rolling off the emerald lakes, when a sudden twist of ankle leaves you stranded. No worries if you've got the right travel insurance NZ—but...

Pet Insurance NZ 2025: Is It Worth the Cost?

Imagine coming home to your loyal labrador, only to find them limping after a sudden accident. A trip to the vet reveals surgery costs over $5,000—money you hadn't budgeted for. This scenario plays ou...

Landlord Insurance NZ: Protecting Your Investment Property

Imagine coming home to discover your prized investment property in Auckland has been trashed by tenants—walls punched, carpets ruined, and worst of all, no rent coming in for months while you foot the...