Property Investment 2026: Is Negative Gearing Still a Valid Strategy?

Imagine pouring your hard-earned KiwiSaver savings into a rental property, only to watch interest rates climb and rents lag behind. For years, negative gearing offered a tax lifeline, letting you offs...

The Lifetimes NZ editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes NZ readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Imagine pouring your hard-earned KiwiSaver savings into a rental property, only to watch interest rates climb and rents lag behind. For years, negative gearing offered a tax lifeline, letting you offset those losses against your salary. But in 2026, with New Zealand's ring-fencing rules fully entrenched, is this strategy still worth pursuing? Let's dive into whether property investment remains viable without the old tax perks.

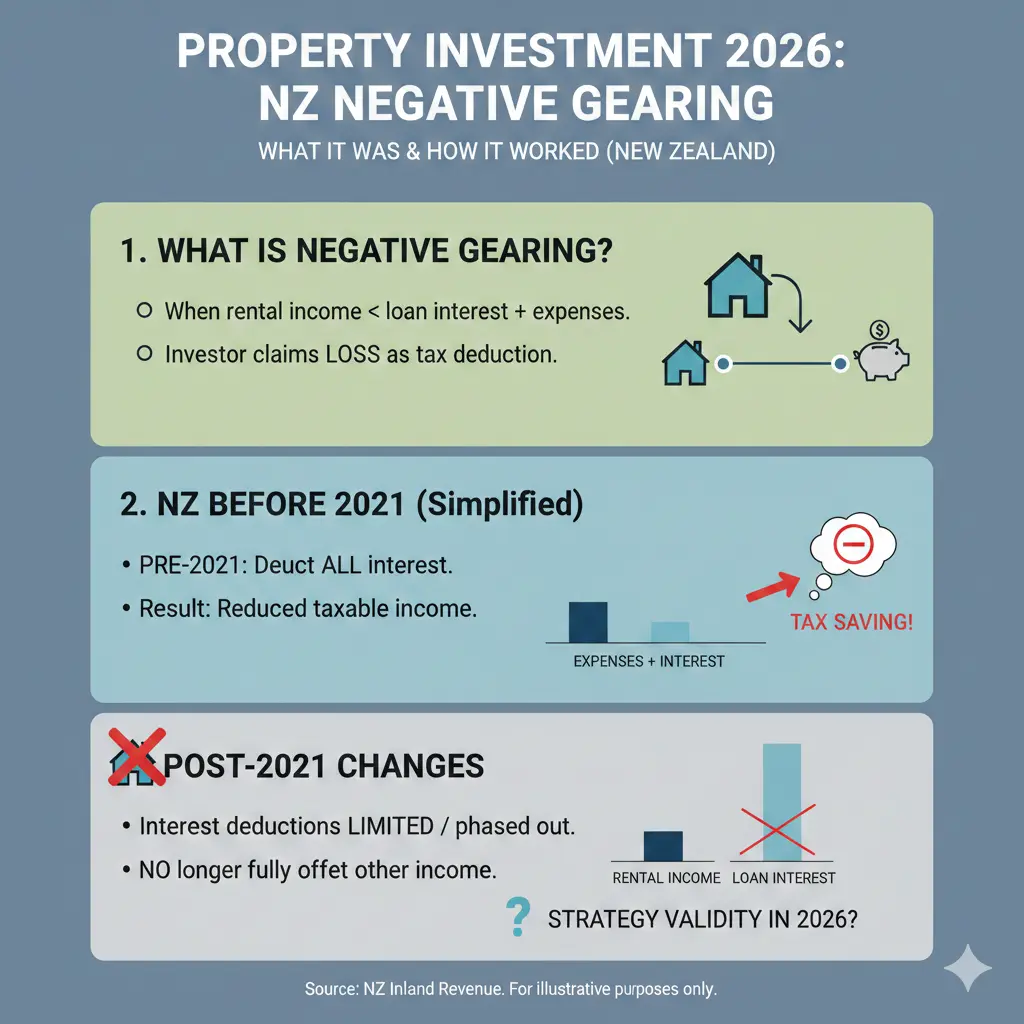

What is Negative Gearing and How Did It Work in New Zealand?

Negative gearing occurs when the costs of owning an investment property—think mortgage interest, rates, insurance, and maintenance—exceed the rental income it generates. Investors borrowed to buy properties, claiming the shortfall as a tax deduction against other income like wages, effectively reducing their overall tax bill.

In the past, this was a popular tactic for Kiwis building wealth through property. A working couple might buy a rental in Auckland, gear it negatively, and deduct losses from their PAYE income, boosting cash flow via tax refunds. But governments grew concerned it favoured investors over first-home buyers, inflating house prices.

The Shift: Ring-Fencing Rules Explained

New Zealand phased out unrestricted negative gearing through ring-fencing, starting in 2019 and fully implemented by April 2025. Now, any rental losses are "fenced off" and can only offset future residential property income—not your salary or business earnings.

Under IRD rules, deductions are limited to market-rate rental income. If your property runs at a loss, that shortfall carries forward to future years' property profits, not other income sources. This levels the playing field, aiming to cool investor demand for existing homes and encourage new builds.

New Zealand's Property Market in 2026: A Cautious Outlook

Heading into 2026, the market tells a story of moderation. Bank economists forecast 2-5% house price growth, down from overly optimistic 7-10% predictions for 2025 that didn't materialise. Regional differences are stark: Auckland and Wellington lag, while Canterbury, Otago, and Southland see modest gains.

Housing inventory hits a 10-year high, creating buyer's markets in many areas. Ownership costs—council rates, insurance, maintenance—rise faster than wages, squeezing cash flows. Debt-to-income (DTI) limits, volatile migration, and a flood of townhouses/apartments curb the leverage-driven booms of 2012-2021.

Impact of Ring-Fencing on Investors

Without offsetting losses against wages, negative gearing's appeal has waned. Crockers notes investors can no longer boost returns via tax deductions from other income, potentially discouraging new builds as predicted by the Property Investors Federation.

Yet, some adapt: properties may turn positively geared over time as rents rise with inflation. Focus shifts to cash-flow positive buys or value-add strategies like renovations.

Is Negative Gearing Still a Valid Strategy in 2026?

Short answer: No, not in its classic form. Ring-fencing has neutered the wage-offset benefit, making high-leverage, loss-making investments riskier amid high interest rates and stagnant rents.

But property investment isn't dead. Capital growth remains the draw—house prices are still projected to edge up, albeit slowly. Without a comprehensive capital gains tax (CGT) in NZ, gains on sales (except bright-line breaches) stay tax-free, unlike Australia where CGT discounts fuel debate.

Pros and Cons in the Current Landscape

- Pros: Long-term appreciation possible in growth areas like Otago; tax-free capital gains; KiwiSaver integration for deposits; ring-fenced losses usable against future property income.

- Cons: No wage deductions; high holding costs; DTI caps limit borrowing; market stagnation risks.

Alternative Strategies for Kiwi Property Investors in 2026

Ditch pure negative gearing for resilient approaches. Here's practical advice tailored to NZ:

1. Target Cash-Flow Positive Properties

Seek rentals where income covers expenses. In regional spots like Southland, lower purchase prices and steady rents make this feasible. Use tools like IRD's rental income calculator to verify market rates.

2. Focus on New Builds and Developments

Bright-line test exemptions for new builds (if held over 10 years) pair with potential Healthy Homes compliance perks. Government incentives via Kāinga Ora may support supply.

3. Diversify Beyond Residential

Consider commercial property or syndicates, where ring-fencing is less restrictive. Or blend with KiwiSaver property funds for lower-risk exposure.

4. Leverage Financing Wisely

With DTI limits, aim for 60-70% LVR. Shop banks for investor mortgages; compare via Canstar or interest.co.nz. Build a cash buffer for rate hikes.

Tip: Consult a licensed financial adviser and accountant familiar with IRD rules—deductions like depreciation still apply if claims are valid.

Tax Implications and IRD Compliance

No CGT means investment returns hinge on growth and yield, not tax plays. Watch the bright-line test: properties sold within 10 years (5 for new builds pre-2024) trigger income tax on gains.

Track expenses meticulously via apps like Landed or Xero. Ring-fenced losses? Log them on your IR3 return for carry-forward.

Next Steps for Smart Investing

Crunch your numbers: Use MoneyHub's calculators or consult IRD's property guide. Stress-test for 8% rates and 3% vacancy. Network via NZ Property Investors Federation meetups. If negative gearing's gone, pivot to sustainable strategies—NZ's market rewards patient, cash-savvy Kiwis. Start with a free IRD webinar or adviser chat today.

Frequently Asked Questions

Sources & References

-

1

Ring-fencing | Tax NZ | How does it affect you? - Crockers — www.crockers.co.nz

-

2

Negative gearing - Wikipedia — en.wikipedia.org

-

3

House Price Predictions 2026 & 2027 - MoneyHub NZ — www.moneyhub.co.nz

-

4

Why Most Investors Are About to Lose Everything in 2026 - YouTube — www.youtube.com

-

5

How cutting the CGT discount could help rebalance housing market — www.firstlinks.com.au

-

6

Does New Zealand Have a Capital Gains Tax? [2026] | Opes Partners — www.opespartners.co.nz

-

7

Tax Breaks Double Investor Home Purchases Over First-Timers — www.miragenews.com

Related Articles

Buying Off-Plan: How to Avoid the Common 2026 Construction Pitfalls

Picture this: you've spotted the perfect off-plan apartment in Auckland's bustling Wynyard Quarter, visions of harbour views and modern living dancing in your head. But months turn into years, costs b...

Bright-Line Test Explained: Tax on Property Sales

Ever flipped a property for a quick profit or held onto an investment longer than planned? In New Zealand, the Bright-Line Test could mean the difference between keeping your gains or handing a chunk...

Interest Deductibility for Rental Properties NZ

Imagine pouring your hard-earned cash into a rental property, only to watch a big chunk of your mortgage interest payments get clawed back by the IRD come tax time. For years, that's been the reality...

Being a Landlord in NZ: Complete Legal Guide

Ever wondered if property investment could be your ticket to financial freedom, but the legal maze of being a landlord in New Zealand has you hesitating? You're not alone—thousands of Kiwis dip their...