Buying Off-Plan: How to Avoid the Common 2026 Construction Pitfalls

Picture this: you've spotted the perfect off-plan apartment in Auckland's bustling Wynyard Quarter, visions of harbour views and modern living dancing in your head. But months turn into years, costs b...

James writes about the New Zealand property market, renting, home ownership, and housing costs. He breaks down complex property topics into practical advice for renters and buyers.

Picture this: you've spotted the perfect off-plan apartment in Auckland's bustling Wynyard Quarter, visions of harbour views and modern living dancing in your head. But months turn into years, costs balloon, and what was meant to be your dream home becomes a construction nightmare. In 2026, with New Zealand's property market stabilising after years of ups and downs, buying off-plan remains a popular path for Kiwis chasing new builds—yet it's riddled with pitfalls like delays, rising prices, and quality issues. This guide arms you with practical strategies to sidestep those common traps and secure a smart investment.

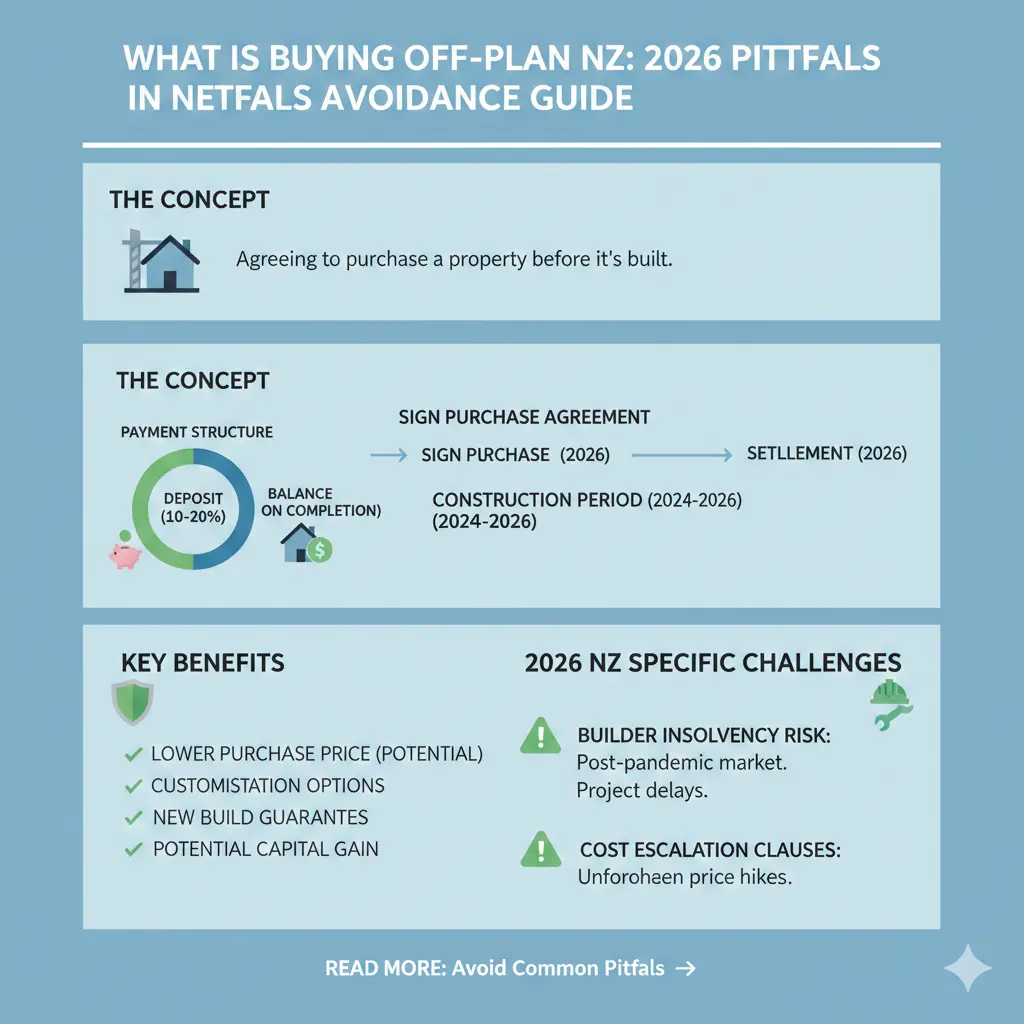

What is Buying Off-Plan in New Zealand?

Buying off-plan means committing to purchase a property—often an apartment, townhouse, or house—before it's built, typically from plans and renders provided by the developer. It's a staple in Kiwi property investment, especially in high-demand areas like Auckland, Christchurch, and Wellington, where new developments promise modern features and potential capital growth.

In 2026, off-plan sales are thriving amid increased housing supply and moderating interest rates, with the Reserve Bank holding the Official Cash Rate at 2.25% after cuts in late 2025. Buyers love the chance to lock in today's prices for tomorrow's home, but a 2025 Squirrel report shows 89% of potential buyers favour completed new builds over off-plan due to fears of delays and cost overruns.

Why Kiwis are Drawn to Off-Plan in 2026

- Lower entry deposits: New builds dodge LVR restrictions, letting you buy investment properties with just 20% down—ideal for spreading funds across Auckland and Christchurch townhouses.

- Tax perks: Full interest deductibility on new builds makes them cashflow-friendly for investors.

- Market timing: Softer house prices and buyer power in 2026 give you negotiation leverage.

Common 2026 Construction Pitfalls—and How to Avoid Them

New Zealand's construction sector faces unique challenges in 2026: labour shortages, material cost spikes from global inflation, and an oversupply of unsold townhouses sitting for 2-3 years. Here's how to dodge the biggest headaches.

Pitfall 1: Endless Delays

Extended build timelines are the top gripe, with off-plan townhouses often hit hardest as buyers crave move-in-ready certainty. Weather disruptions, supply chain hiccups, and contractor shortages exacerbate this in our variable climate.

Avoid it:

- Scrutinise the developer's track record—check past projects on the Building Performance website for completion dates and disputes.

- Negotiate milestone penalties in your sale agreement: e.g., $500/week delay compensation after 6 months overdue.

- Build in a 20% buffer to your settlement timeline.

Pitfall 2: Sneaky Price Hikes

Inflation-driven cost increases can add 10-20% to your bill, turning a $850,000 Auckland townhouse into a budget-buster. Fixed-price contracts are rare; variations for "unforeseen site conditions" are common.

Avoid it:

- Insist on a fixed-price contract with caps on variations (e.g., no more than 5% without your approval).

- Include an escalation clause tied to the Producers Price Index, reviewed quarterly.

- Get independent quantity surveyor quotes pre-contract to benchmark costs.

Pitfall 3: Leaky Buildings and Weathertightness Woes

Our history of leaky homes haunts off-plan buys—despite stricter Building Code updates, monoclint brick and aluminium issues persist in rushed jobs. In 2026, with medium-density housing booming, quality control is key.

Avoid it:

- Mandate a Clause 7.2.1 producer statement from engineers confirming weathertightness compliance.

- Commission a specialist pre-construction weathertightness review.

- Budget $5,000-10,000 for a post-handover building survey by a Licensed Building Practitioner (LBP).

Pitfall 4: Overseas Investment Rules Snags

If you're not a Kiwi citizen or ordinarily resident, off-plan exemptions apply mainly to large apartment blocks (20+ units) with OIO certificates—but you can't always live there yourself. Signing without checking risks massive fines.

Avoid it:

- Apply for OIO pre-approval (valid up to a year) via Toitū Te Whenua before offers.

- Verify residential land status on Quotable Value NZ—avoid sensitive sites near beaches needing extra consent.

- For Aussies/Singaporeans, holiday homes may qualify under exemptions.

Pitfall 5: Oversupply and Resale Risks

Townhouse glut in 2026 means thousands unsold, suppressing prices while quality standalone homes hold value. Off-plan buyers risk buying into a stagnant pocket.

Avoid it:

- Analyse suburb data for growth and yields via Opes Partners tools or CoreLogic reports.

- Prioritise school zones and energy-efficient designs buyers crave.

- Opt for mixed-use developments with retail below for rental appeal.

Step-by-Step Guide to Safe Off-Plan Buying in 2026

- Get pre-approved: Secure finance early—auctions demand it, and new-build exemptions ease deposits.

- Due diligence dive: Review LIM reports, resource consents, and geotech surveys from council portals.

- Hire pros: Engage a property lawyer specialising in off-plan (e.g., via NZ Law Society), plus a buyer's agent.

- Sign smart: Use ADLS/REINZ sale agreement with custom off-plan clauses.

- Monitor progress: Quarterly site visits and progress reports.

- Handover check: Full Code Compliance Certificate (CCC) before settlement, plus LBP inspection.

Financing Your Off-Plan Purchase

Banks love new builds for lower risk, but progressive drawdowns mean staged payments. In 2026's buyer-friendly market, shop rates—expect 5-6% fixed. KiwiSaver withdrawals and First Home Grants apply to new builds via Kāinga Ora.

Pro tip: Hedge NZD volatility with forward contracts if transferring funds.

Next Steps for Your Off-Plan Journey

Start by listing must-haves: location, budget, timeline. Contact a REINZ agent for current off-plan listings, run OIO pre-checks if needed, and book a lawyer consult. In 2026's balanced market, patience pays—secure your future without the pitfalls. Visit lifetimes.co.nz for more Kiwi property guides and connect with local experts today.

Frequently Asked Questions

Sources & References

-

1

Buying property in New Zealand in 2026 - Smart Currency Exchange — www.smartcurrencyexchange.com

-

2

Buying residential property to live in - Overseas investment - LINZ — www.linz.govt.nz

-

3

Top property trends buyers are craving in 2026 — www.propertybrokers.co.nz

-

4

NZ Property Investment (2026): A Step-by-Step Guide | Opes Partners — www.opespartners.co.nz

-

5

Property Investing New Zealand: The Ultimate Guide for Beginners — property-ceo.com

-

6

House Price Predictions 2026 & 2027 - MoneyHub NZ — www.moneyhub.co.nz

Related Articles

Property Investment 2026: Is Negative Gearing Still a Valid Strategy?

Imagine pouring your hard-earned KiwiSaver savings into a rental property, only to watch interest rates climb and rents lag behind. For years, negative gearing offered a tax lifeline, letting you offs...

Bright-Line Test Explained: Tax on Property Sales

Ever flipped a property for a quick profit or held onto an investment longer than planned? In New Zealand, the Bright-Line Test could mean the difference between keeping your gains or handing a chunk...

Interest Deductibility for Rental Properties NZ

Imagine pouring your hard-earned cash into a rental property, only to watch a big chunk of your mortgage interest payments get clawed back by the IRD come tax time. For years, that's been the reality...

Being a Landlord in NZ: Complete Legal Guide

Ever wondered if property investment could be your ticket to financial freedom, but the legal maze of being a landlord in New Zealand has you hesitating? You're not alone—thousands of Kiwis dip their...