Bright-Line Test Explained: Tax on Property Sales

Ever flipped a property for a quick profit or held onto an investment longer than planned? In New Zealand, the Bright-Line Test could mean the difference between keeping your gains or handing a chunk...

Sarah covers personal finance, tax, and KiwiSaver topics for Lifetimes NZ. She focuses on making money management straightforward and practical for everyday Kiwis.

Ever flipped a property for a quick profit or held onto an investment longer than planned? In New Zealand, the Bright-Line Test could mean the difference between keeping your gains or handing a chunk over to IRD. With the rules simplifying to a two-year window since July 2024, understanding this tax on property sales is crucial for every Kiwi investor, first-home buyer, or family upgrading their home.

Whether you're eyeing a reno project in Auckland or a lifestyle block in Waikato, this guide breaks down the Bright-Line Test explained: tax on property sales with 2026 updates, real examples, and steps to stay compliant. Let's dive in so you can plan your next move confidently.

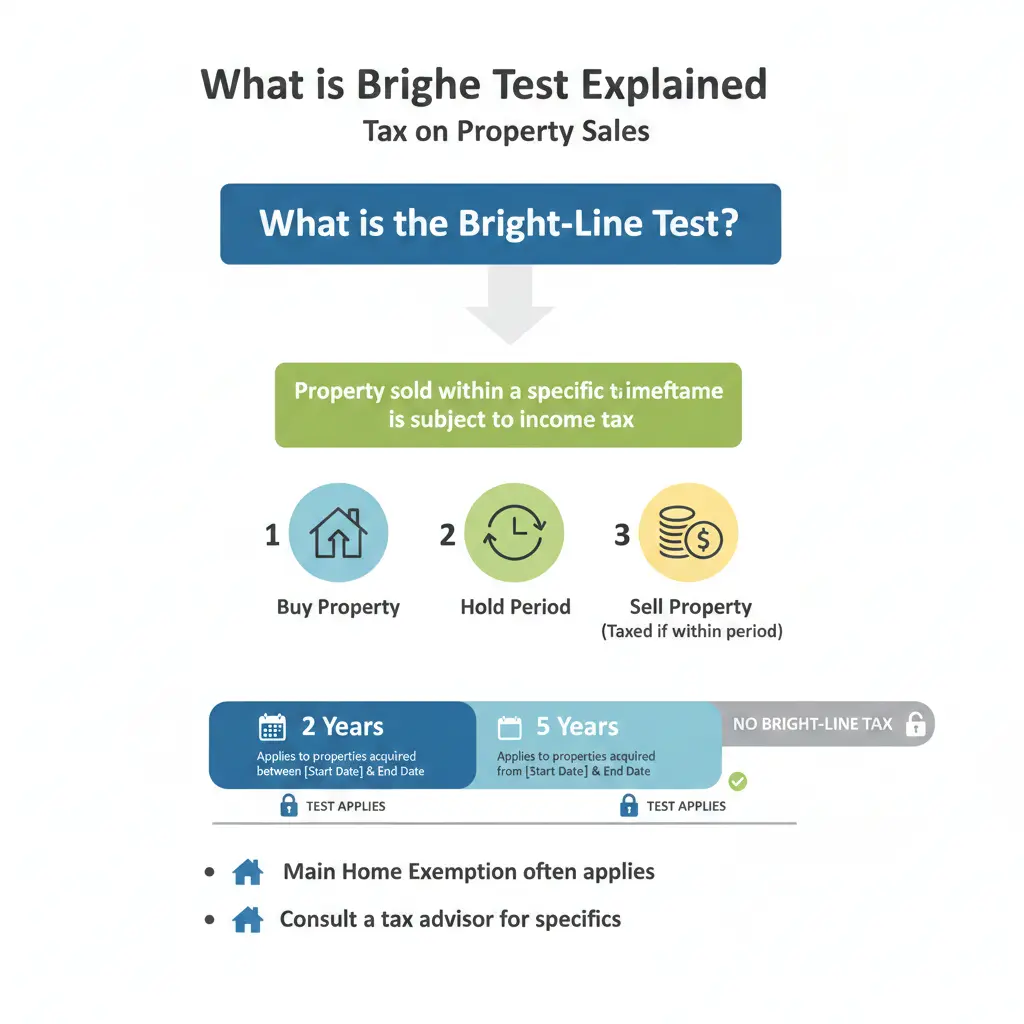

What is the Bright-Line Test?

The Bright-Line Test is an IRD rule that taxes profits from selling residential property if you sell within a specific timeframe, called the bright-line period. It's designed to target speculators flipping houses for profit, treating those gains as taxable income rather than capital gains.

Unlike a full capital gains tax, it only kicks in for sales within the bright-line period. Profits are added to your personal income and taxed at your marginal rate – which could be up to 39% for higher earners. This applies to Kiwi tax residents, even for overseas residential properties.

Key point: Properties acquired before 1 October 2015 are exempt entirely. If you're dealing with older holdings, breathe easy – no bright-line worries there.

How the Bright-Line Period Works in 2026

As of 1 July 2024, the bright-line period shortened dramatically to 2 years for properties sold on or after that date. This applies if your binding sale and purchase agreement is entered into after 1 July 2024.

- Bright-line start date: Usually the settlement date when the title transfers to you. For off-the-plan buys, it might differ.

- Bright-line end date: When you sign a binding agreement to sell.

Before July 2024, periods varied: 5 or 10 years depending on acquisition date and new build status. The acquisition date locks in your rules – so check yours via IRD's Property Tax Decision Tool.

Recent Changes: Why the 2-Year Rule Matters Now

The National Government rolled back the extended periods to boost housing supply and ease investor burdens. No more 10-year overhang for most sales post-July 2024.

For example:

- Buy a house in August 2024, sell in September 2026? Within 2 years – taxable unless excluded.

- Sell in October 2026? Outside 2 years – no bright-line tax.

This shift favours genuine investors over short-term flippers. But other property taxes like the general income test (if you're in the business of buying/selling) might still apply.

Calculating Your Tax Under the Bright-Line Test

Taxable profit = Sale price minus (purchase price + allowable costs like agent fees, legal costs, and improvements). You'll report this on your IR3 return or complete an IR833 form post-sale for your lawyer or accountant to calculate.

Practical tip: Keep meticulous records. Receipts for renovations can reduce your taxable gain significantly. Use apps like Xero or consult an accountant early.

Example Calculation

Jane buys a Whangārei fixer-upper for $600,000 in September 2024 (settlement). She spends $50,000 on renos, $10,000 on agents/lawyers. Sells for $800,000 in June 2026 (within 2 years).

Profit: $800,000 - ($600,000 + $50,000 + $10,000) = $140,000 taxable at Jane's rate (say 33% = $46,200 tax).

If sold in August 2026? No bright-line tax.

Main Home Exclusion: Your Biggest Shield

The main home exclusion is a game-changer – no bright-line tax if the property was your main home for the majority of ownership.

To qualify:

- It's where you and your whānau live, keep belongings, and have social ties.

- At least 50% of the ownership period (excluding construction) used as main home.

Construction periods don't count against you. Picture this Kiwi scenario: You buy a vacant section in Christchurch ($400k), it's empty 3 months, build for 13 months, live there 6 months, then sell. Ignore build time – 6 months occupied vs 3 months vacant = over 50%, excluded.

First-home buyers get extra leeway – their family home is exempt regardless of holding period.

Other Key Exclusions and Reliefs

Not every sale triggers tax. Common exemptions include:

- Inherited property: Executors or inheritors can sell without bright-line tax.

- Farmland or lifestyle blocks: If used or usable as farmland, exempt. Check dominant use.

- Business premises: Over 50% business use? No tax.

- Rollover relief: Family transfers (e.g., to spouse or trust) can defer tax.

- Weather events: North Island 2023 events – sales to Crown/local authority exempt.

New builds: Pre-2024 rules had shorter periods, but now all align at 2 years post-July 2024.

Special Situations Kiwis Face

Off-the-Plan and New Builds

For pre-construction buys, start date might be contract signing, not settlement. Always verify with IRD.

Overseas Properties

Kiwi tax residents: Same 2-year rule applies to Aussie holiday homes or UK rentals.

Companies and Trusts

If held personally, profits hit your income. Trusts/companies have different rules – seek advice.

Practical Tips to Minimise or Avoid Bright-Line Tax

- Hold longer: Wait out the 2 years from settlement.

- Make it your main home: Live there predominantly.

- Track costs: Log every expense to lower gains.

- Use the IRD tool: Free Property Tax Decision Tool on ird.govt.nz.

- Get pro help: Accountants or lawyers specialising in property (e.g., via CAANZ directory).

- Plan transfers: Rollover for family gifting.

In a hot 2026 market, with Auckland medians around $1.1m and regional growth, timing sales smartly saves thousands.

Next Steps for Smart Property Moves

Ready to buy, sell, or hold? Start with IRD's Property Tax Decision Tool today. Chat with a tax advisor for personalised advice – especially if mixing main home with rentals. Track KiwiSaver impacts too, as property profits affect contributions.

Stay ahead in NZ's property game: Plan with the 2-year rule in mind, claim exclusions confidently, and keep records squeaky clean. Your profit – and peace of mind – depends on it.

Frequently Asked Questions

Sources & References

-

1

IRD: The Bright-Line Test — www.ird.govt.nz

-

2

Baker Tilly: Understanding New Zealand's Bright-Line Rules — bakertillysr.nz

-

3

MoneyHub: Bright-Line Test for NZ Property Sales — www.moneyhub.co.nz

-

4

BusinessLike: Bright-Line Test Explained for Property Owners — businesslike.co.nz

-

5

Ross Holmes Lawyers: Understanding the Bright-Line Test — rossholmeslawyers.com

-

6

Willis Legal: What the Brightline Test Changes Mean for You — www.willislegal.co.nz

-

7

Gilligan Sheppard: Land and the Bright-Line Test — gilligansheppard.co.nz

Useful Tools

Related Articles

Buying Off-Plan: How to Avoid the Common 2026 Construction Pitfalls

Picture this: you've spotted the perfect off-plan apartment in Auckland's bustling Wynyard Quarter, visions of harbour views and modern living dancing in your head. But months turn into years, costs b...

Property Investment 2026: Is Negative Gearing Still a Valid Strategy?

Imagine pouring your hard-earned KiwiSaver savings into a rental property, only to watch interest rates climb and rents lag behind. For years, negative gearing offered a tax lifeline, letting you offs...

Interest Deductibility for Rental Properties NZ

Imagine pouring your hard-earned cash into a rental property, only to watch a big chunk of your mortgage interest payments get clawed back by the IRD come tax time. For years, that's been the reality...

Being a Landlord in NZ: Complete Legal Guide

Ever wondered if property investment could be your ticket to financial freedom, but the legal maze of being a landlord in New Zealand has you hesitating? You're not alone—thousands of Kiwis dip their...