Capital Gains: What's Taxable in NZ (Even Without CGT)

Imagine selling your investment property after years of holding it, only to discover a hefty tax bill waiting because of rules that treat your profit as income. Even without a full capital gains tax (...

The Lifetimes NZ editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes NZ readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Imagine selling your investment property after years of holding it, only to discover a hefty tax bill waiting because of rules that treat your profit as income. Even without a full capital gains tax (CGT) in New Zealand, certain capital gains are taxable right now—and proposed changes could reshape the landscape for Kiwis in 2026 and beyond.

We've all heard the debates: New Zealand lacks a comprehensive CGT like Australia or the UK, letting most asset sale profits go untaxed. But don't get too comfortable. The bright-line test and other IRD rules mean some gains are taxed as income at your personal rate—up to 39% in 2026. With talks of a new 28% CGT on investment properties from July 2027, understanding what's taxable today is crucial for protecting your wealth.

This guide breaks it down: what counts as taxable, real Kiwi examples, and steps to stay compliant. Whether you're flipping houses, trading shares, or holding crypto, here's what you need to know for 2026.

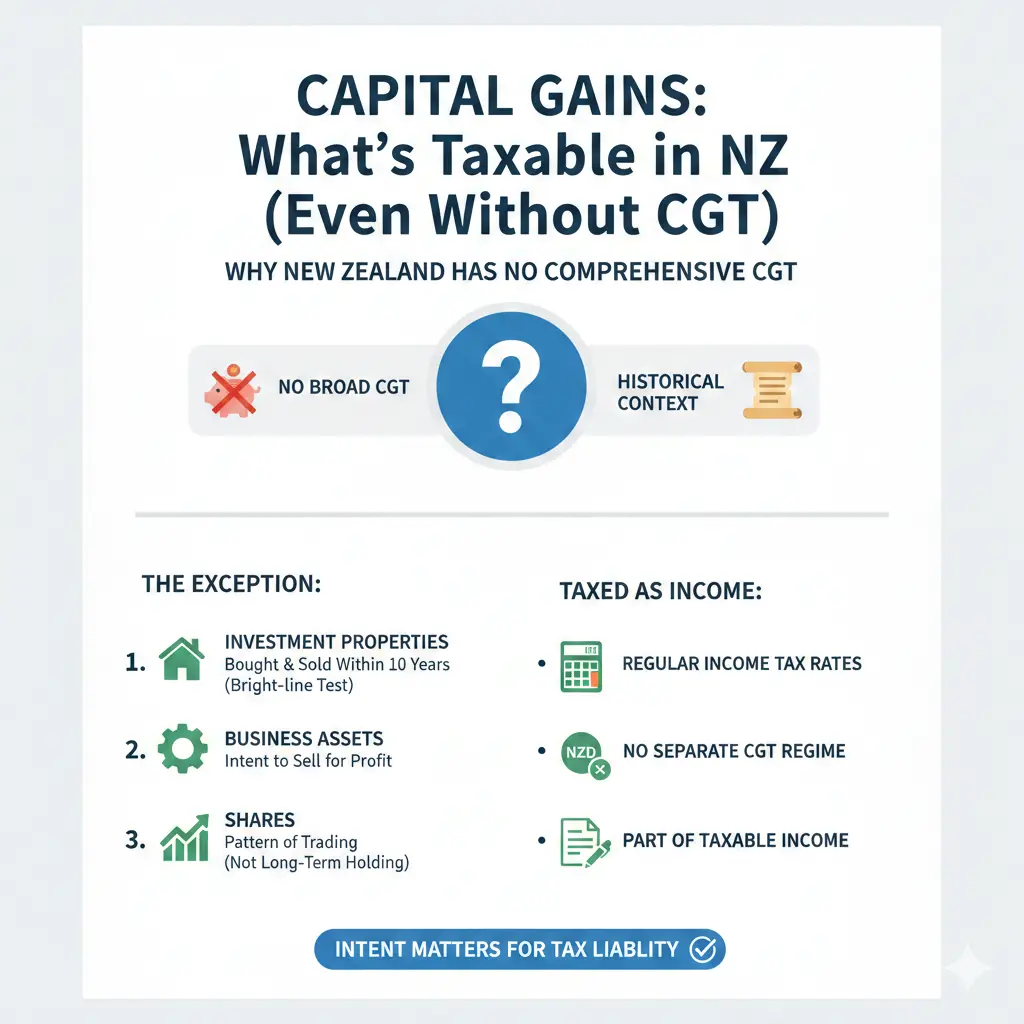

Why New Zealand Has No Comprehensive CGT—But Taxes Some Gains Anyway

New Zealand stands out globally: no broad CGT means you can buy assets like shares, art, or classic cars, sell for a profit, and keep it all—unless specific rules apply. Profits from asset sales are not automatically income; they're capital gains, untaxed by default.

But the IRD draws a line. If your activity looks like a business—frequent buying/selling, short holds, or profit intent—gains become taxable income. This distinction trips up many Kiwis.

Profits vs Capital Gains: The Key Difference

- Profits (taxed): From business activity, like a property flipper selling multiple homes yearly. Taxed at your marginal rate: 10.5% to 39%.

- Capital gains (untaxed): One-off sale of a long-held family bach or shares in a KiwiSaver fund. No CGT applies.

For instance, dividends from NZ shares are taxed at PIE rates (10.5%, 17.5%, 28%), but gains on local shares under $50,000 are tax-free. Foreign shares over $50,000 fall under FIF rules, taxing gains.

The Bright-Line Test: NZ's Closest Thing to CGT

Introduced in 2015 and extended to 10 years in 2021, the bright-line test taxes gains on residential property sold within that period as income. It's not a true CGT—it's income tax at your rate—but it captures short-term flips.

How the Bright-Line Test Works in 2026

Your sale date determines the test period:

| Property Acquired | Bright-Line Period |

|---|---|

| Before 29 March 2018 | 2 years |

| 29 March 2018 – 26 March 2021 | 5 years |

| 27 March 2021 – current | 10 years |

Source: Adapted from IRD guidelines via MoneyHub.

Exemptions include your main home (if you live there), farmland, business premises, and new builds. Example: Buy an investment rental on 1 April 2026, sell after 8 years (2034)—gain taxed as income, added to your salary. If you earn $100,000 salary and make $400,000 gain:

- Total income: $500,000

- Tax calculation (2026 rates): Up to 39% on amounts over $180,000, totalling ~$151,200 or 37.8% effective on the gain.

Tip: Keep records of purchase costs, improvements, and holding periods. Use the IRD's myIR portal to check obligations.

Other Taxable Capital Gains in NZ

Beyond property, IRD targets 'professional' activity. Here's what's often taxed:

Share Trading and Investments

Buy/sell shares occasionally? Gains untaxed. Trade frequently? IRD may deem it a business, taxing profits. KiwiSaver gains are tax-free; only dividends/interest taxed at PIE rates.

- Local/NZ-Aus shares <$50k: No tax on gains.

- Foreign Investment Fund (FIF) rules: For overseas shares over $50k, gains taxed under fair dividend rate (5% of opening value).

Crypto follows similar rules: hodl long-term, untaxed; day-trade, taxed as income.

Property Flipping and Development

If IRD sees you as a 'property trader' (multiple sales, marketing as business), all gains taxed—bright-line or not. Recent example: A Kiwi developer sold three sections in Auckland within a year; full profits taxed at 33-39%.

Crypto, Art, and Other Assets

Racehorses, vintage cars, wine collections: Untaxed unless you're in the 'business' of trading them. Crypto gains taxed if frequent trading; otherwise, safe.

Proposed CGT Changes: What 2026 Means for Kiwis

As of February 2026, no CGT exists, but proposals heat up. A potential 28% flat CGT on investment property gains from July 2027—excluding family homes and farms.

Key Proposal Details

- Start date: 1 July 2027, non-retrospective. Value properties then; only future gains taxed.

- Rate: Flat 28%, vs bright-line's personal rates (up to 39%).

- Scope: Investment properties only. Losses offset future gains.

- Impact: Could raise $400m+ yearly, cooling speculation.

Critics note valuation costs and inflation issues—taxing nominal gains without adjustment. Political traction uncertain; past attempts (2006+) failed.

Actionable advice: If holding rentals, consider selling before 2027 or consult a tax advisor now. Refinance or restructure with lawyers for deductions.

Practical Tips to Minimise Tax on Capital Gains

- Hold Long-Term: Beat bright-line (10 years) or don't trigger business rules.

- Track Costs: Deduct purchase price, repairs, agent fees from gains.

- Use Exemptions: Live in the property briefly to qualify as main home (but beware intent rules).

- KiwiSaver Smart: Tax-free growth; max contributions for retirement.

- Get IRD Rulings: Apply for binding rulings on trader status via ird.govt.nz.

- Record-Keeping: Use apps like Xero; retain 7 years.

For property investors, offset losses against future gains under current rules. Always factor ACC levies and KiwiSaver withdrawals.

"Don't sell. Just make sure whatever you invest makes sense as a long-term hold. And if you don't sell, you won't pay capital gains tax. Full stop."

Next Steps: Protect Your Assets Today

Review your portfolio: Check bright-line dates on IRD's property sales tool. Consult a chartered accountant or visit ird.govt.nz for personalised advice. With CGT talks ramping up, structure investments wisely—consider trusts or long holds.

Disclaimer: This is general info, not advice. Tax rules change; seek professional financial advice tailored to your situation from an IRD-registered advisor.

Frequently Asked Questions

Sources & References

-

1

Capital Gains Tax in New Zealand - MoneyHub NZ — www.moneyhub.co.nz

- 2

-

3

What If NZ Introduced Capital Gains Tax in 2026 ft. Matthew Harris — lighthousefinancial.co.nz

-

4

28% Capital Gains Tax? + The Inflation U-Turn - YouTube — www.youtube.com

-

5

New Zealand - Individual - Income determination — taxsummaries.pwc.com

Related Articles

Working Multiple Jobs NZ: Tax and Legal Considerations

Juggling multiple jobs can boost your income, but it's crucial to understand the tax implications and legal requirements that come with working more than one role in Aotearoa. Whether you're a contrac...

Name Changes NZ: Legal Process and Costs

Considering a fresh start with a new name? Whether it's after marriage, divorce, or simply embracing a personal transformation, changing your name in New Zealand is straightforward but requires follow...

Holiday Home Tax Rules NZ: Private Use and Rental

Own a bach in Coromandel or a holiday home in Queenstown? You're not alone—many Kiwis cherish these escapes, but renting them out while enjoying personal use can trip you up on tax rules. Getting the...

Industry Bodies and Professional Associations NZ

Whether you're launching a business, advancing your career, or navigating financial regulations, industry bodies and professional associations in New Zealand offer invaluable support. These organisati...