Interest Deductibility for Rental Properties NZ

Imagine pouring your hard-earned cash into a rental property, only to watch a big chunk of your mortgage interest payments get clawed back by the IRD come tax time. For years, that's been the reality...

James writes about the New Zealand property market, renting, home ownership, and housing costs. He breaks down complex property topics into practical advice for renters and buyers.

Imagine pouring your hard-earned cash into a rental property, only to watch a big chunk of your mortgage interest payments get clawed back by the IRD come tax time. For years, that's been the reality for many Kiwi landlords. But here's the good news: interest deductibility for rental properties NZ is back in full force as of 1 April 2025, letting you claim 100% of that interest against your rental income. This game-changing reversal means lower tax bills and healthier cash flow for property investors across the country.

In this guide, we'll break down everything you need to know about the reinstated rules, from how they work to who qualifies and practical tips for maximising your deductions. Whether you're a seasoned investor with a portfolio or dipping your toes into the rental market, understanding these changes is key to making smarter financial decisions in today's market.

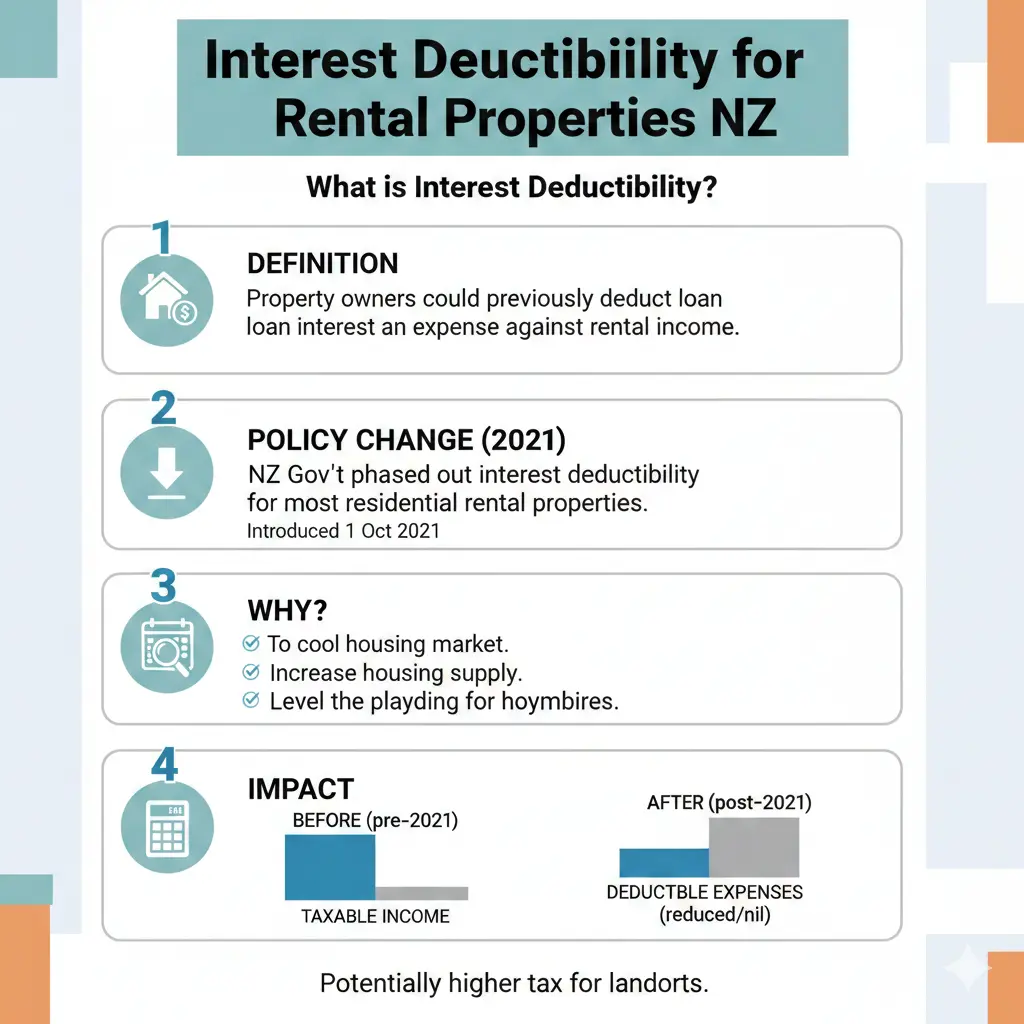

What is Interest Deductibility for Rental Properties?

At its core, interest deductibility allows you to subtract the interest you pay on loans for your rental property from your rental income before calculating tax. This reduces your taxable income, potentially saving you thousands each year. For example, if your rental brings in $30,000 annually but you pay $25,000 in mortgage interest, you'd only pay tax on $5,000 (minus other expenses) instead of the full rent.

Before 2021, this was straightforward—most investors claimed 100% of their interest. But Labour's policy changes phased it out to curb housing speculation, hitting existing owners with a gradual reduction and banning it entirely for properties bought after 27 March 2021 (with exceptions for new builds). The tide turned with the new government's election promise, restoring deductibility in phases.

Why It Matters for Kiwi Investors

- Cash flow boost: Lower taxes mean more money in your pocket to service debt or reinvest.

- Portfolio growth: Investors can now scale up without the drag of non-deductible interest.

- Fairer tax treatment: You're taxed on actual profit, not inflated rental income.

One investor shared how the old rules forced them to pay tax on gross rent despite negative cash flow—now, they're saving over $110,000 in tax over 15 years.

Current Rules for Interest Deductibility (2026 Update)

By 2026, we're fully in the era of 100% deductibility. Here's the timeline that got us here:

| Period | Deductibility Rate | Key Notes |

|---|---|---|

| 1 April 2025 onwards (including 2026 tax year) | 100% | Full claim on all residential rental properties, regardless of purchase date. |

| 1 April 2024 – 31 March 2025 | 80% | Applies to all properties; transitional phase. |

| 1 April 2023 – 31 March 2024 | 50% (pre-27 March 2021 properties); 0% (post) | Phased-out rules now history. |

For the 2026 income year (1 April 2025 to 31 March 2026), you can deduct 100% of actual interest incurred on loans for residential rentals. This overrides previous limitations—no more worrying about when you bought the property or drew down the loan.

New Builds: Always a Winner

Properties with a Code Compliance Certificate (CCC) issued after 27 March 2020 qualify as new builds. These have enjoyed 100% deductibility throughout, and the new rules keep that perk intact. If you're investing in off-the-plan apartments or new subdivisions, this exemption stacks nicely with the restoration.

Who Qualifies for Full Interest Deductibility?

Pretty much every Kiwi landlord with a residential rental property. The rules apply broadly:

- All residential investment properties in New Zealand, including houses, flats, and units.

- Existing and new loans: Covers mortgages for purchase, renovations, or refinancing—as long as they're tied to rental use.

- No purchase date restrictions: Even if you bought post-2021, you're now covered.

Exceptions and caveats:

- Private use: Interest must be for income-producing purposes. If the property's partly your home, apportion accordingly.

- Companies: Most non-residential-focused companies are exempt from old limits, but close companies (five or fewer owners controlling 50%+) follow residential rules.

- Build-to-rent: Special exemptions may apply for larger projects.

Pro tip: Use the IRD's online tool to check if the rules apply to your specific property.

What Expenses Can You Claim?

Beyond interest, rental properties offer a range of deductions. With interest back online, bundle these for maximum effect:

- Mortgage interest: 100% from 1 April 2025.

- Renovations and maintenance: Roof repairs, insulation, heating—fully deductible if they keep the property rentable.

- Insurance, rates, and agent fees: Standard operating costs.

- Travel for inspections: Kilometre logs at IRD rates.

Remember: Keep receipts and records for at least seven years—IRD audits are no joke.

Related Tax Rules: Bright-Line Test

Don't forget the bright-line test, which taxes gains on residential properties sold within a set period. Updates align with deductibility changes:

- Properties sold after 1 July 2024: 2-year bright-line.

- Sold by 30 June 2024: 5 or 10 years depending on purchase date; new builds post-2021 get 5 years.

IRD gets automatic sales data, so track your ownership periods closely to avoid penalties.

Practical Tips for Claiming Deductions in 2026

- Review your 2025 tax return: If you filed under 80% rules, amend for full deductibility where possible.

- Refinance strategically: Shop for lower rates now that interest is fully deductible—savings compound.

- Track everything: Use apps like Xero or Propertrack for rental expenses.

- Consult a pro: Chat with your accountant or visit ird.govt.nz for personalised advice.

- Consider KiwiSaver or trusts: Structure investments tax-efficiently, especially for multiple properties.

- Monitor ring-fencing: Rental losses are still ring-fenced to offset future rental income only.

Example: Sarah owns a $800,000 rental in Auckland with $40,000 annual interest and $28,000 rent. Pre-restoration, she'd tax on ~$28,000 minus other costs. Now, it's $28,000 - $40,000 = loss, carried forward. Cash flow win!

Next Steps for Kiwi Property Investors

With interest deductibility for rental properties NZ fully restored, 2026 is a prime time to review your portfolio. Crunch the numbers on your next tax return, explore refinancing for better rates, and ensure your records are audit-ready. Head to ird.govt.nz/property-interest-rules for the official tool and guidance—it's free and tailored for Kiwis. If in doubt, book a session with an accountant specialising in property tax. Your rental empire just got a lot more profitable—make the most of it.

Frequently Asked Questions

Sources & References

-

1

Interest deductibility restored for residential properties — wolterskluwer.com — www.wolterskluwer.com

- 2

-

3

Residential Properties – Interest Deductibility & Bright-line — dbchartered.co.nz — www.dbchartered.co.nz

-

4

New Zealand - Corporate - Deductions — taxsummaries.pwc.com — taxsummaries.pwc.com

-

5

Interest Deductibility in NZ: 2025 Tax Rules — opespartners.co.nz — www.opespartners.co.nz

-

6

Interest Deductibility Returns: What Landlords Can and Can't Claim — angelpropertymanagers.co.nz — angelpropertymanagers.co.nz

-

7

Residential property interest limitation rules — ird.govt.nz — www.ird.govt.nz

-

8

Rental Property Tax Deductions Explained for NZ Investors — businesslike.co.nz — businesslike.co.nz

Useful Tools

Related Articles

Buying Off-Plan: How to Avoid the Common 2026 Construction Pitfalls

Picture this: you've spotted the perfect off-plan apartment in Auckland's bustling Wynyard Quarter, visions of harbour views and modern living dancing in your head. But months turn into years, costs b...

Property Investment 2026: Is Negative Gearing Still a Valid Strategy?

Imagine pouring your hard-earned KiwiSaver savings into a rental property, only to watch interest rates climb and rents lag behind. For years, negative gearing offered a tax lifeline, letting you offs...

Bright-Line Test Explained: Tax on Property Sales

Ever flipped a property for a quick profit or held onto an investment longer than planned? In New Zealand, the Bright-Line Test could mean the difference between keeping your gains or handing a chunk...

Being a Landlord in NZ: Complete Legal Guide

Ever wondered if property investment could be your ticket to financial freedom, but the legal maze of being a landlord in New Zealand has you hesitating? You're not alone—thousands of Kiwis dip their...