ETFs vs Managed Funds: Which is Better for Kiwi Investors?

When you're ready to invest your money, you'll likely come across two main options: exchange-traded funds (ETFs) and managed funds. Both offer diversification and professional management, but they wor...

The Lifetimes NZ editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes NZ readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

When you're ready to invest your money, you'll likely come across two main options: exchange-traded funds (ETFs) and managed funds. Both offer diversification and professional management, but they work quite differently—and the choice between them can significantly impact your returns over time. For Kiwi investors, understanding these differences is crucial because the fees you pay, the tax treatment, and how easily you can buy and sell your investments all play a role in building wealth.

What Are ETFs and Managed Funds?

Both ETFs and managed funds are investment vehicles that pool money from multiple investors to purchase a diversified portfolio of assets. However, they operate in fundamentally different ways.

Exchange-Traded Funds (ETFs)

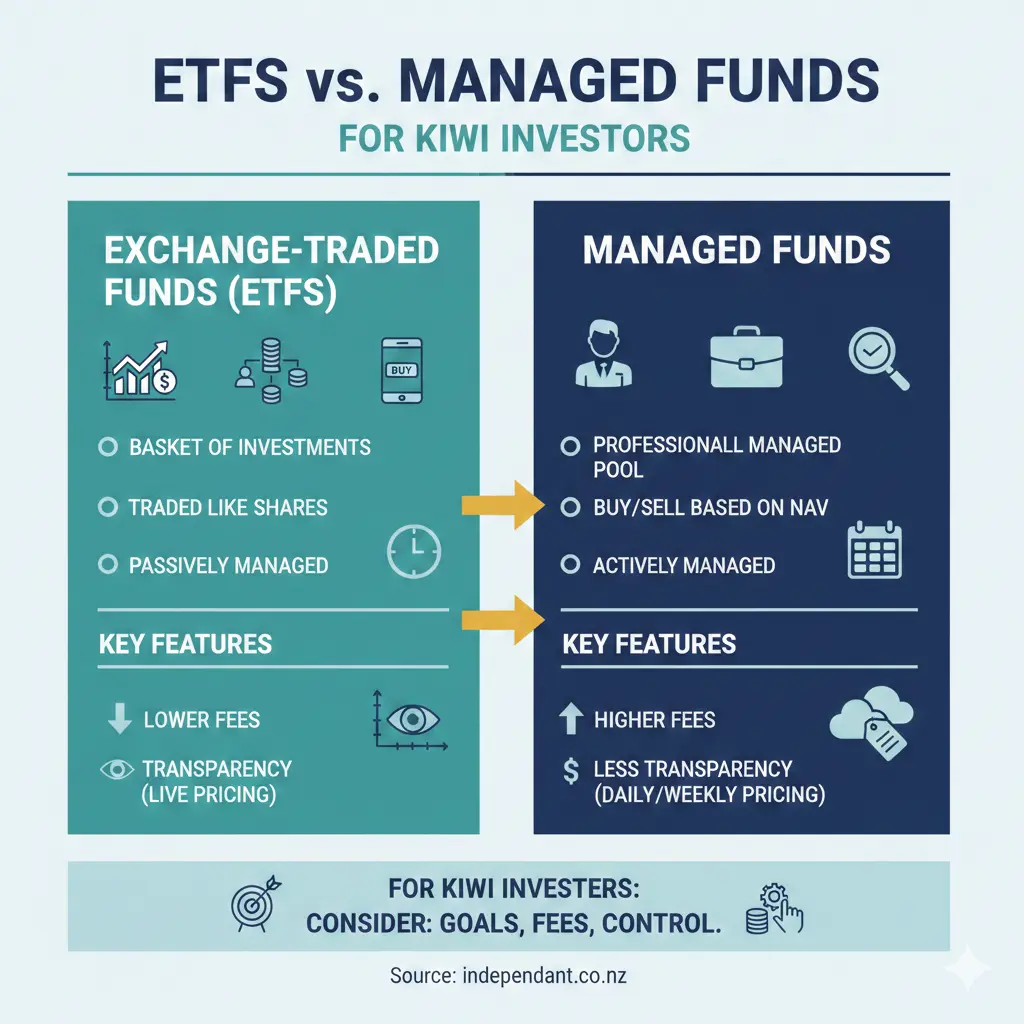

ETFs are funds that trade on a stock exchange—in New Zealand, that's the NZX (New Zealand Stock Exchange). You buy and sell ETF units just like you'd buy shares, through a brokerage platform or investment app. Most ETFs offered in New Zealand are passive investments, meaning they track a market index and aim to match its performance rather than beat it. For example, an ETF might track the NZX 50 or the S&P 500. There are some active ETFs available, but they're less common.

Managed Funds

Managed funds are typically actively managed, which means a professional fund manager makes decisions about which investments to buy and sell to try to outperform a benchmark index. When you invest in a managed fund through platforms like Sharesies, you're buying units directly from the fund provider, not from other investors on an exchange.

The Fee Difference: Where Your Money Actually Goes

One of the biggest differences between ETFs and managed funds comes down to cost, and this is where the maths gets really interesting for your long-term wealth.

How Managed Funds Charge You

Managed funds typically charge significantly higher fees than ETFs. A standard actively managed fund in New Zealand might charge between 1–2% per year in management fees. Some managed funds also charge performance fees when they outperform a benchmark—meaning you pay extra if the manager does well.

How ETFs Charge You

ETFs charge much lower management fees because they're mostly passive—they're simply tracking an index, not paying for active decision-making. For example, a broad market Australian shares ETF might charge just 0.07% per year. When you buy or sell ETF units, you'll also pay brokerage fees through your broker, but there are no ongoing fees just for holding them.

The Long-Term Impact

The difference in fees might not sound huge, but over decades, it compounds dramatically. Consider this example: if you invested $10,000 with a 5% annual return, assuming a low-fee ETF charging 0.04% annually versus an actively managed fund charging 1.26% annually, after 40 years the ETF would be worth around $69,335, while the managed fund would be worth $43,436. That's a difference of nearly $26,000—or 59% more wealth—simply because of lower fees.

Pricing, Liquidity, and Transparency

Real-Time Pricing vs. Delayed Pricing

ETFs trade on the stock exchange during trading hours, so you can see the exact price of your investment at any moment during the trading day. You know exactly what you're buying or selling and at what price. Managed funds, by contrast, typically update their pricing daily, weekly, or even monthly. This means you might not know the exact value of your investment for days after you've tried to buy or sell.

Buying and Selling

ETFs offer high liquidity because they're traded on an exchange and have dedicated market makers who ensure there's always someone willing to buy or sell. You can typically buy or sell at any time during the trading day. Managed funds usually only allow you to buy or sell at the end of each day or less frequently, and some have minimum investment amounts that can be quite large.

Transparency

With ETFs, you can see exactly what's in the fund's portfolio on any given day. Managed funds are often less transparent—you might not know the exact holdings or how frequently they're updated.

New Zealand-Specific Advantages for ETFs

If you're investing in New Zealand assets through ETFs, there's a significant tax advantage. New Zealand-listed ETFs are classified as Listed PIEs (Portfolio Investment Entities), which means investment returns are taxed at a fixed rate of 28%. This benefits top-rate taxpayers who would normally pay 33% tax on investment income, potentially saving you money on your tax bill each year.

ETFs are also incredibly accessible for Kiwi investors. Platforms like Sharesies, Hatch, and Stake allow you to buy ETFs for as little as a few dollars, with no minimum investment requirement (other than what your broker sets). This makes it easy to start investing even if you don't have a large lump sum.

When Might Managed Funds Make Sense?

While ETFs have clear advantages in terms of fees and transparency, managed funds aren't entirely without merit. Here are situations where they might be worth considering:

- Active management strategy: If you believe a skilled fund manager can genuinely outperform the market over time, an actively managed fund might appeal to you. However, research suggests most active managers don't consistently beat index returns after fees.

- Hands-off investing: Managed funds require less involvement from you—you simply invest and let the manager handle everything. ETFs, while still passive, require you to decide when to buy and sell.

- Specific investment objectives: Some managed funds target very specific strategies or sectors that might not be available as ETFs.

- Fractional units: Managed funds allow you to buy fractional units, which means advisers can size trades more precisely. ETFs only allow whole unit purchases.

The Practical Comparison for Kiwis

| Feature | ETFs | Managed Funds |

|---|---|---|

| Management fees | Typically 0.04–0.20% p.a. | Typically 1–2% p.a. (plus possible performance fees) |

| How you buy/sell | Through a brokerage or investment app on the stock exchange | Directly from the fund provider |

| Pricing | Real-time, during trading hours | Daily, weekly, or monthly |

| Liquidity | High—can buy/sell during trading hours | Lower—usually only daily or less frequent |

| Transparency | Portfolio visible daily | Often opaque or updated infrequently |

| Minimum investment | None (or very low, depending on platform) | Often $500–$5,000 or more |

| Tax advantage (NZ assets) | Listed PIE status = 28% fixed tax rate | Varies depending on structure |

| Diversification | Generally high, tracking broad indices | Varies—can be concentrated |

Getting Started: Practical Steps for Kiwi Investors

Choose Your Platform

Popular investment platforms for Kiwis include Sharesies, Hatch, and Stake. Each offers different ETFs and managed funds, so compare their offerings and fees before deciding.

Understand Your Risk Tolerance

Whether you choose ETFs or managed funds, your first step should be understanding how much risk you're comfortable with. Are you investing for the long term (10+ years)? Can you handle market fluctuations? Your answers will guide which funds to choose.

Consider Your Tax Situation

If you're a top-rate taxpayer and investing in New Zealand assets, the 28% PIE tax rate for ETFs could save you money. Factor this into your decision.

Start Small and Learn

You don't need a large amount to start. Many platforms let you invest a few dollars at a time, so you can begin learning how ETFs or managed funds work without risking significant money.

Making Your Decision

For most Kiwi investors, ETFs offer a compelling case: lower fees, greater transparency, real-time pricing, and easier access. Over decades, the fee savings alone can mean tens of thousands of dollars more in your pocket. The 28% PIE tax rate for New Zealand-listed ETFs adds another advantage for top-rate taxpayers.

Managed funds still have a place, particularly if you genuinely believe a skilled manager can outperform the market and you're willing to pay for that potential outperformance. However, the burden of proof is on the fund manager—they need to consistently beat the index by more than their fees, which many don't.

The best investment is the one you'll stick with long-term. If you're just starting out, begin with a simple, low-cost ETF through a platform like Sharesies or Hatch. As your knowledge grows and your portfolio expands, you can always explore managed funds or build a more complex strategy. Remember: time in the market beats timing the market, and lower fees mean more of your money stays invested and working for you.

Frequently Asked Questions

Sources & References

-

1

ETF vs Managed Fund - Betashares — www.betashares.com.au

-

2

Exchange-traded funds | Financial Markets Authority — www.fma.govt.nz

-

3

Index Funds vs ETFs - MoneyHub NZ — www.moneyhub.co.nz

-

4

Making managed funds manageable—Sharesies New Zealand — www.sharesies.nz

-

5

ETFs vs Managed Funds - The Tradeoffs between Structures — www.dimensional.com

-

6

ETFs vs Shares vs Unlisted Funds: Which is Right for You? — kernelwealth.co.nz

Related Articles

Ethical Investing in NZ: Top 5 Sustainable Funds for Kiwis

Ever wondered if you can grow your KiwiSaver or investments while doing good for the planet and people? Ethical investing in New Zealand is booming, with Kiwis pouring billions into funds that priorit...

Beginner's Guide to Investing in New Zealand

Getting started with investing in New Zealand doesn't have to be complicated. Whether you're looking to grow your wealth, save for retirement, or build financial security, there are plenty of accessib...

How to Buy Shares in New Zealand: Step-by-Step Guide

Ever wondered how to dip your toes into share investing without getting overwhelmed? Whether you're saving for a house deposit, retirement, or just want to grow your hard-earned cash, buying shares in...

Index Funds NZ: The Simple Way to Invest

Ever wondered how to grow your hard-earned KiwiSaver or savings without spending hours picking stocks or paying sky-high fees? Index funds offer a straightforward path to building wealth, tracking mar...