Shares vs Property NZ: Building Long-Term Wealth

For many Kiwis, building long-term wealth boils down to one big question: should you pour your hard-earned savings into shares or sink them into property? In New Zealand's evolving market, where high...

Sarah covers personal finance, tax, and KiwiSaver topics for Lifetimes NZ. She focuses on making money management straightforward and practical for everyday Kiwis.

For many Kiwis, building long-term wealth boils down to one big question: should you pour your hard-earned savings into shares or sink them into property? In New Zealand's evolving market, where high interest rates, regulatory changes, and affordability challenges are reshaping opportunities, understanding the shares vs property NZ debate is crucial for smart decision-making.

Property has long been the go-to for generations of New Zealanders, offering tangible assets and leveraged growth. Yet shares—through KiwiSaver, ETFs, and index funds—are gaining traction for their accessibility, liquidity, and competitive returns. This guide breaks it down with current 2026 insights, helping you weigh risks, returns, and real-world Kiwi considerations to build lasting wealth.

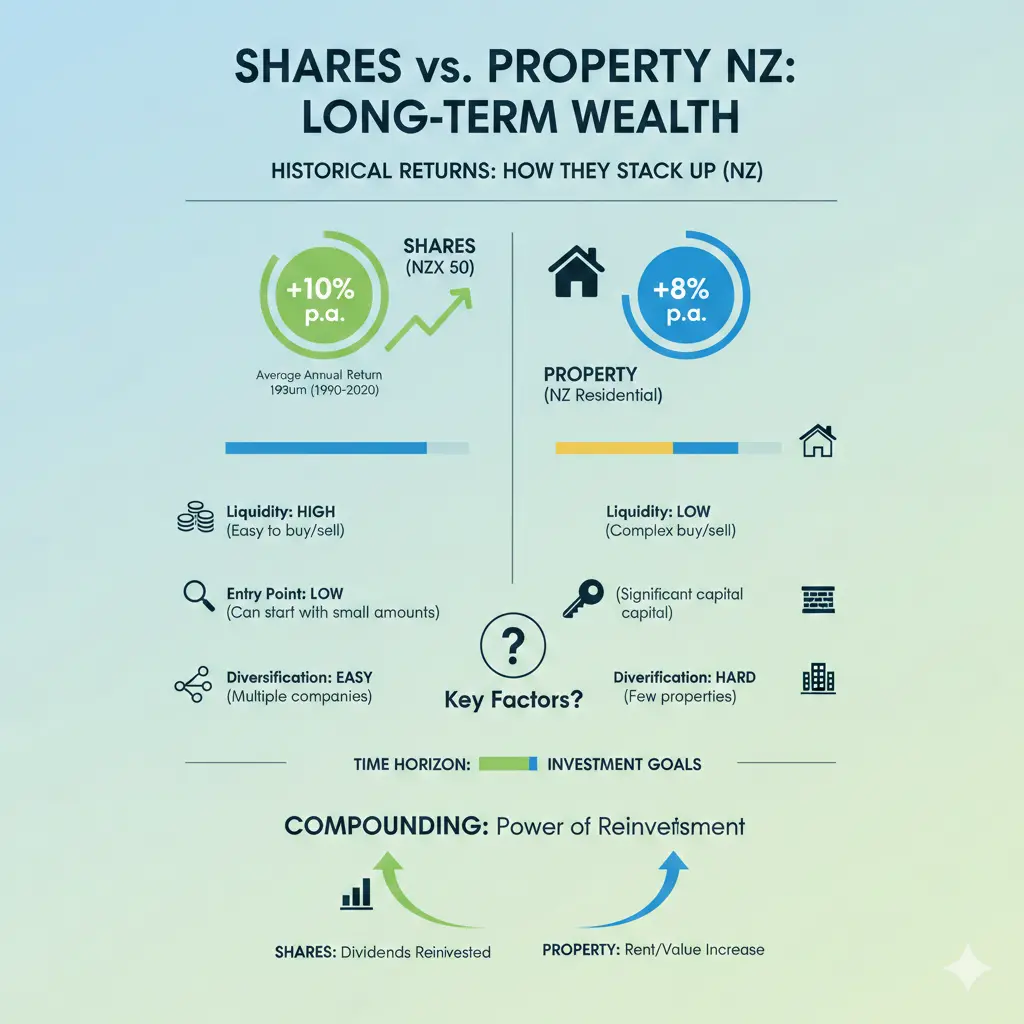

Historical Returns: How Shares and Property Stack Up in NZ

Over the long term, both assets have built wealth, but their performance varies. Auckland house prices grew at an average of 5.83% annually from 2003-2023, though this slowed to just 0.5% in 2023 amid higher rates and tighter lending. Nationally, NZ house prices have averaged 5.8% annual growth since 1990.

Shares tell a different story. The S&P 500 has delivered around 10% average annual returns over the past 30 years, outpacing NZ property. Global index funds have also beaten Auckland property over the last 20 years (9.8% vs 5.83%). KiwiSaver, with over three million participants since 2007, has proven shares' potential for steady wealth accumulation despite volatility.

2026 Outlook: Why Shares May Edge Ahead

Heading into 2026, property faces headwinds like steady buyer caution, increased stock listings post-summer, and policy shifts around taxes and immigration. High interest rates continue to squeeze cash flow, with many rentals remaining negative after costs. Shares, meanwhile, benefit from diversified global exposure and lower entry barriers, making them resilient in a high-rate environment.

| Feature | Shares & Funds | Investment Property |

|---|---|---|

| Historical Returns | 7–10% annually | 5–6% (leveraged, capital gains) |

| Auckland Property (2003-2023) | N/A | 5.83% annually |

| S&P 500 (30 years) | ~10% | N/A |

Costs and Accessibility: Getting Started in NZ

The barrier to entry is a game-changer in the shares vs property NZ matchup. You can start investing in shares with as little as $1 via platforms like InvestNow or Kernel. Property demands a hefty 20-40% deposit—think $150,000–$400,000 for a $1 million Auckland home—plus strict bank lending criteria. Entry-level rentals in major cities now hit $600,000–$800,000, requiring 35%+ deposits.

Ongoing Costs: Hidden Drains on Wealth

Property isn't set-and-forget. Expect maintenance, tenant management, compliance with Healthy Homes standards (2022 updates), and potential cash top-ups since rents often fall short of mortgage repayments. Shares keep it simple: low platform fees, no repairs, and passive management via ETFs or funds.

- Property extras: Rates, insurance, vacancies, and Healthy Homes upgrades.

- Shares perks: Automatic dividends, no tenant hassles.

For hands-off Kiwis, shares win on convenience, freeing you to focus on your job or family.

Risks and Volatility: Protecting Your Nest Egg

Property feels solid, but it's not immune to bubbles, corrections, or interest rate hikes—key risks amplified by leverage. Shares fluctuate daily, yet long-term holders weather storms better, with global diversification reducing NZ-specific risks.

Leverage: Double-Edged Sword

Banks lend 60-80% LVR for investment properties, supercharging gains but demanding top-ups if rates rise. Tax-deductible interest (reinstated 2023) helps, but cash flow stays tight. Shares offer margin loans or leveraged ETFs (e.g., 3x S&P 500 via Tiger Brokers), but volatility triggers margin calls.

Tip: Use an offset account on your mortgage to minimise interest while investing equity in shares.

Liquidity and Diversification: Flexibility Matters

Sell shares in 1-2 days; properties take weeks to months with hefty fees. Shares shine in diversification—spread across global markets via one ETF. Property ties you to one asset, often in a single suburb.

Hybrid Options for Kiwis

- REITs: Property exposure with share-like liquidity—perfect for real estate fans without the hassle.

- Equity release: Tap home equity for shares, diversifying without selling.

- KiwiSaver boost: Max contributions for tax perks and employer matches while building a share-heavy portfolio.

Tax Rules: NZ-Specific Traps and Tips (2026)

Navigate IRD rules carefully. Property gains are tax-free outside the bright-line test (2 years for investments), but interest deductibility is back—yet doesn't fix negative cash flow. Shares face FIF tax (5% on foreign holdings over $50,000), eased by PIE funds.

| Asset | Key Tax Rule |

|---|---|

| Property | Bright-line 2 years; interest deductible (2023+) |

| Shares | FIF 5% (>$50k foreign); PIEs simplify |

Actionable advice: Consult IRD.govt.nz or a tax advisor. PIE funds via platforms like Kernel minimise headaches.

Practical Strategies for Building Wealth in 2026

Don't choose—combine. Start with $500 in a global index fund, add $100 monthly at 8% growth: that's ~$28,000 in 10 years. Meanwhile, save for property without waiting.

- Assess your risk: Conservative? Mix property with REITs. Growth-focused? Shares via KiwiSaver.

- Start small: Use Sharesies or Hatch for micro-investments.

- Leverage wisely: Offset mortgages, avoid over-borrowing amid 2026 rate stability.

- Monitor markets: Watch OCR decisions and election-year policies.

For families, shares fund education via StudyLink savings; property builds legacy but locks capital.

"Global index funds have outperformed New Zealand property over the past 20 years... By investing in shares and funds, you're adapting to today's market conditions."

Next Steps to Build Your Wealth

Review your finances: Calculate your risk tolerance and cash flow. Open a low-fee platform like InvestNow, max KiwiSaver, and model scenarios using sorted.org.nz tools. For property, check realestate.co.nz listings against your deposit. Diversify across shares and property for resilience.

Disclaimer: This is general information, not personalised advice. Consult a licensed financial adviser, IRD, or accountant before investing. Markets fluctuate, and past performance isn't a guarantee.

Frequently Asked Questions

Sources & References

-

1

Shares vs Property Investment - MoneyHub NZ — www.moneyhub.co.nz

-

2

Could shares now outperform housing for long-term wealth? - NZ Herald — www.nzherald.co.nz

-

3

Property vs. Shares: What's The Better Option? - Finsol — www.finsol.co.nz

-

4

Which is best for 2026 - property or shares? - YouTube — www.youtube.com

-

5

New Zealand Housing Market 2026: What Property Investors Should Watch - Najib Real Estate — www.najibrealestate.co.nz

-

6

Property vs shares vs managed funds - What's riskier? - Opes Partners — www.opespartners.co.nz

Related Articles

Industry Bodies and Professional Associations NZ

Whether you're launching a business, advancing your career, or navigating financial regulations, industry bodies and professional associations in New Zealand offer invaluable support. These organisati...

Emergency Benefit NZ: When You Have No Other Options

When you're struggling financially and don't qualify for other benefits, the Emergency Benefit might be your lifeline. It's a discretionary payment designed for Kiwis in genuine hardship who've exhaus...

Unpaid Internships NZ: Are They Legal?

Unpaid internships are a common pathway for students and graduates to gain work experience in New Zealand, but there's often confusion about whether they're actually legal. The short answer is: unpaid...

Estate Administration NZ: Managing Someone's Affairs After Death

Losing a loved one is one of life's toughest challenges, and stepping in to manage their estate can feel overwhelming. In New Zealand, estate administration—the process of handling someone's affairs a...