Offset Mortgages NZ: Are They Worth It?

Imagine slashing thousands off your mortgage interest without locking away a single dollar. That's the promise of offset mortgages NZ – a smart tool Kiwis are using to pay down their home loans faster...

Sarah covers personal finance, tax, and KiwiSaver topics for Lifetimes NZ. She focuses on making money management straightforward and practical for everyday Kiwis.

Imagine slashing thousands off your mortgage interest without locking away a single dollar. That's the promise of offset mortgages NZ – a smart tool Kiwis are using to pay down their home loans faster. But with floating rates often higher than fixed options, are offset mortgages NZ worth it for you? Let's dive in.

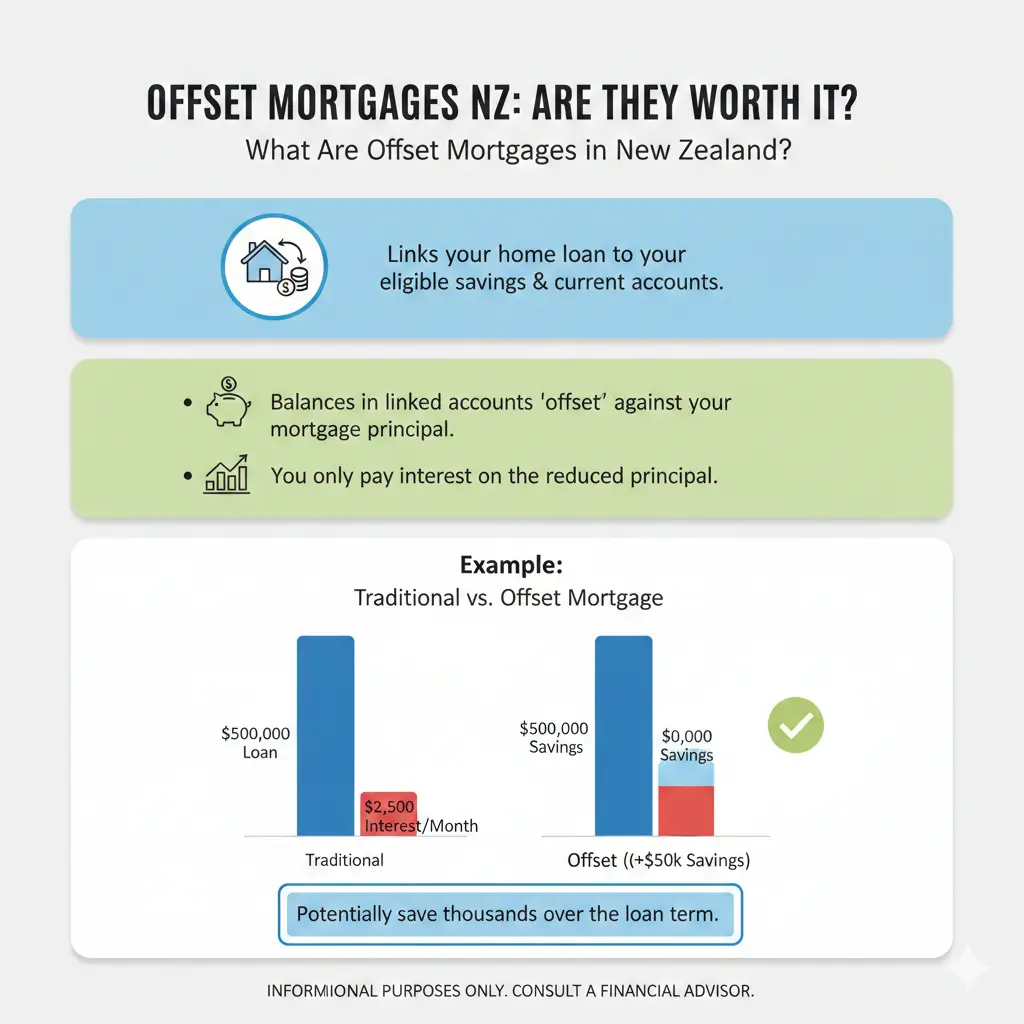

What Are Offset Mortgages in New Zealand?

Offset mortgages link your everyday transaction or savings accounts directly to your home loan. The balance in those accounts is subtracted from your mortgage principal when calculating daily interest, so you only pay interest on the net amount.

For instance, if your mortgage is $400,000 and you hold $50,000 across linked accounts, you'll pay interest on just $350,000. Unlike traditional savings where you'd earn low, taxable interest, your money works harder by directly reducing mortgage costs – and mortgage rates typically beat savings rates.

Only a handful of Kiwi banks offer them: Kiwibank, Westpac, and BNZ. They're usually floating-rate loans, giving you flexibility but exposing you to rate changes.

How Offset Mortgages Work Day-to-Day

Your linked accounts act like a spending hub: salary in, bills out, and the daily closing balance offsets your loan. Interest is calculated daily, so maintaining higher balances amplifies savings.

- Full access: Withdraw anytime – no penalties for using your own money.

- No credit interest: Linked accounts earn zero interest, but you avoid tax on savings income.

- Multiple accounts: Link several, including family members' in some cases (BNZ allows up to 50!).

A $300,000 Westpac loan offset by $25,000 at 4.59% p.a. over 30 years could save over $78,000 in interest and shave nearly 4 years off the term.

Pros and Cons of Offset Mortgages NZ

Offset mortgages shine for disciplined savers, but they're not for everyone. Here's a balanced look:

| Feature | Offset Mortgage | Standard Mortgage (Fixed/Floating) |

|---|---|---|

| Interest Calculation | On mortgage minus savings | On full mortgage balance |

| Access to Savings | Yes, full access | N/A |

| Interest on Savings | No (but tax-free savings) | Yes (taxable at your rate) |

| Loan Type | Floating | Fixed or Floating |

| Flexibility | High (extra repayments free) | Varies (fixed may have penalties) |

Key Benefits

- Massive interest savings: The more you offset, the less interest accrues – ideal for lump sums like bonuses or KiwiSaver withdrawals.

- Faster payoff: More of your repayments hit principal, shortening the loan term.

- Family strategy: Pool balances from partners, kids, or parents to maximise offset (check bank rules).

- No early repayment fees: Make extras or lump sums freely.

- Tax efficiency: Avoid PIR-taxed savings interest; savings are tax-free when offsetting.

Potential Drawbacks

- Higher base rate: Offset loans often sit 0.5-1% above best fixed rates, so low savings mean higher costs.

- Discipline required: Spendthrift habits erode benefits – treat it like a transaction account, not a piggy bank.

- Limited availability: Only three major banks; shop around for rates.

- No interest earned: If rates spike or you have minimal balances, a high-interest savings account might outperform.

Offset Mortgages vs Other Home Loan Options in NZ

In 2026, with OCR steady and floating rates around 5-6%, offsets compete against fixed deals. Fixed loans offer rate certainty but less flexibility; revolving credits act like overdrafts for irregular incomes.

Best for:

- Offsets: High earners/savers with $20k+ buffers, investors, or families pooling funds.

- Fixed: Budget-focused owner-occupiers locking in lows.

- Revolving: Renovators or self-employed with lumpy cashflow.

Run the numbers: if your average offset exceeds the rate premium (e.g., $30k+ on a $500k loan), it's a winner.

Are Offset Mortgages Worth It? Real NZ Examples

Take John with a $300k mortgage fully offset by savings – zero interest paid, full access retained. Or Jill offsetting $20k on $50k owed: interest only on $30k.

For a Kiwi family: Dad's salary ($8k/month) sits in offset pre-bills, averaging $15k buffer on $600k loan. At 5.5%, that's ~$10k annual savings vs a standard floating loan.

Investors love them too – offset rental income to deduct less interest come tax time (chat to your accountant). But if your buffer dips below 10-20% of the loan, fixed might edge it.

2026 Rate Snapshot (Approximate – Check Current)

- Kiwibank Offset: Floating ~5.49%

- Westpac Choices Offset: ~5.59%

- BNZ TotalMoney: ~5.69%, up to 50 accounts

Compare to 2-year fixed ~4.99%. Offset wins if your average balance covers the gap.

Practical Tips to Maximise Offset Mortgages NZ

Here's how Kiwis make offsets pay off:

- Direct salary: Set it as your pay account for max daily offset.

Pro tip: Model scenarios with bank calculators or a broker – TAG or Opes Partners offer free tools.

Who Should Get an Offset Mortgage?

Ideal for:

- High-income households ($150k+ combined) with savings habits.

- Families channelling kids'/parents' balances.

- Property investors juggling cashflow.

- Anyone planning extras/lump sums.

Skip if: Low savings, prefer fixed budgets, or irregular income better suits revolving credit.

Next Steps: Is an Offset Mortgage Right for You?

Offset mortgages NZ can be a game-changer, potentially saving tens of thousands if you maintain solid buffers. But crunch your numbers – if your savings habits align, they're worth it.

Grab your latest statements, hit up a bank calculator, or book a free broker chat. Compare rates at interest.co.nz, then apply. With floating rates steady in 2026, now's prime time to offset and accelerate freedom from the bank.

Frequently Asked Questions

Sources & References

-

1

Kiwibank Offset Home Loan — www.kiwibank.co.nz

-

2

Your Guide to Understanding Offset Mortgage Options — thetagteam.co.nz

-

3

Westpac Choices Offset Floating Home Loan — www.westpac.co.nz

-

4

Offset Mortgages Explained: Are They Right for You? — www.opespartners.co.nz

-

5

Best Offset Mortgages Explained and Reviewed — www.moneyhub.co.nz

-

6

BNZ TotalMoney Home Loans - Offset Mortgages — www.bnz.co.nz

-

7

Offset Mortgages Explained: Save on Your Home Loan — www.cent.capital

-

8

Offset Mortgages: A Family-Friendly Way to Reduce Interest Costs — www.nzherald.co.nz

Related Articles

Using the NZ Mortgage Calculator to Plan Your House Hunt

Imagine spotting your dream home in Auckland or Christchurch, but wondering if you can actually afford it. That's where the NZ Mortgage Calculator comes in—your essential tool for turning house-huntin...

Mortgage Refixing Guide: How to Negotiate the Best Rate with Your Bank

Imagine slashing hundreds of dollars off your weekly mortgage payments just by knowing when and how to refix. With interest rates easing in 2026, thousands of Kiwis are facing refix decisions that cou...

Mortgage Refinancing: When Does It Make Sense?

Imagine shaving thousands off your mortgage interest while unlocking cash for that home reno or debt consolidation you've been dreaming about. For Kiwis with home loans, mortgage refinancing can be a...

How to Pay Off Your Mortgage Faster (NZ Strategies)

Imagine owning your home outright years earlier than planned, freeing up thousands in interest payments and giving you financial freedom sooner. For Kiwis with mortgages, paying off your home loan fas...