5% Deposit Home Loans in NZ: Government First Home Loan

Imagine finally stepping onto the property ladder without needing to save for years on end. For many Kiwis dreaming of their first home, the First Home Loan with 5% deposit NZ backed by Kāinga Ora mak...

The Lifetimes NZ editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes NZ readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Imagine finally stepping onto the property ladder without needing to save for years on end. For many Kiwis dreaming of their first home, the First Home Loan with 5% deposit NZ backed by Kāinga Ora makes this a reality, slashing the usual 20% deposit barrier to just 5%.

With house prices still high but interest rates stabilising in 2026, this government-supported scheme is a game-changer for first-home buyers. Whether you're eyeing a modest home in Christchurch or something in Wellington, understanding how this works could fast-track your journey to ownership. Let's break it down step by step, with practical tips tailored for New Zealanders.

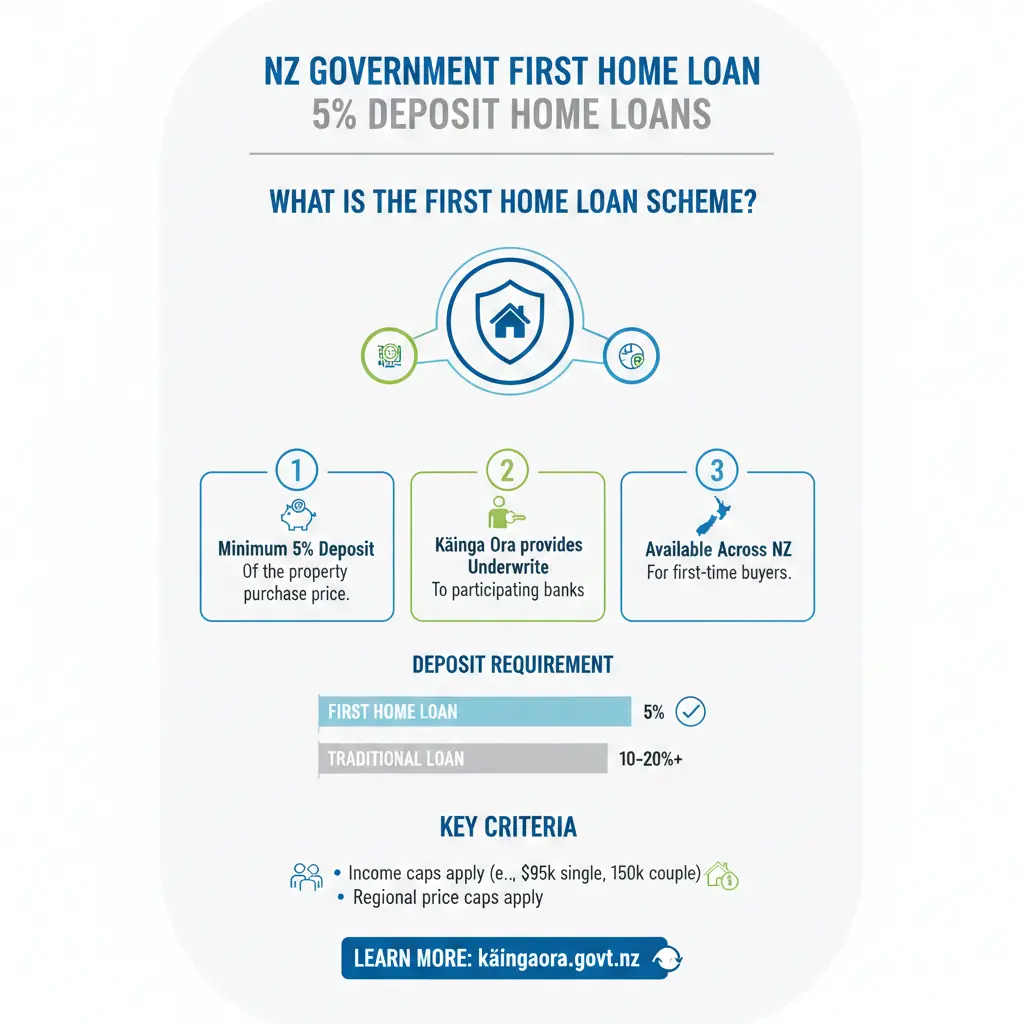

What is the First Home Loan Scheme?

The First Home Loan (previously known as Kāinga Whenua or Welcome Home Loan) is a government-backed programme underwritten by Kāinga Ora – Homes and Communities. It lets eligible first-home buyers secure a mortgage with just a 5% deposit, something most banks won't do on their own due to strict lending rules post-2008 financial crisis.

Participating lenders like Unity Money, Kiwibank, Westpac, BNZ, and SBS Bank issue the loans, but Kāinga Ora covers the risk for the extra 15% deposit portion. This means you borrow up to 95% of the property value, paying a one-off 1.2% Lender’s Mortgage Insurance (LMI) premium.

For example, on a $500,000 home – a realistic price in many NZ regions outside Auckland – you'd need only $25,000 deposit instead of $100,000. That's a huge relief when median incomes hover around $52,500.

| Property Value | 5% Deposit (First Home Loan) | 20% Deposit (Standard) |

|---|---|---|

| $500,000 | $25,000 (Loan: $475,000) | $100,000 (Loan: $400,000) |

| $900,000 | $45,000 (Loan: $855,000) | $180,000 (Loan: $720,000) |

This scheme isn't a free lunch – you'll pay LMI and potentially higher interest initially – but it gets you in the door faster.

Eligibility Criteria for First Home Loan 5% Deposit NZ

To qualify, you must tick all these boxes set by Kāinga Ora. Lenders also apply their own credit checks.

- Age and Residency: At least 18 years old and a New Zealand citizen, permanent resident, or resident visa holder 'ordinarily resident' in NZ.

- Income Limits (last 12 months, before tax):

- $95,000 or less for an individual without dependants.

- $150,000 or less for an individual with dependants.

- $150,000 combined for two or more buyers.

- Deposit: At least 5% of purchase price, from savings, KiwiSaver withdrawals (all but $1,000), gifts, or First Home Grants. No maximum deposit – more is better for rates.

- First-Home Status: First buyer, or previous owner in similar financial position. Can't own other property (except Māori land).

- Property Rules: Under 1 hectare, for your primary residence.

- Other: Pay 1.2% LMI; meet lender's affordability and credit criteria.

Can You Use Gifts or KiwiSaver?

Absolutely. Family gifts count towards your 5%, and KiwiSaver members can withdraw nearly all their balance (leaving $1,000) for the deposit or purchase costs. Combine with the First Home Grant (up to $10,000 for existing homes or $5,000 for new builds) if eligible.

Pro Tip: Get gifts documented with a lawyer's letter to satisfy lenders – it's standard practice in NZ.

How to Apply for a First Home Loan in NZ

It's a team effort between you, a participating lender, and Kāinga Ora. Here's your actionable roadmap:

- Check Eligibility: Use Kāinga Ora's online tool or chat with a lender.

- Boost Your Deposit: Save, withdraw KiwiSaver, apply for grants via Housing NZ.

- Shop Lenders: Compare rates from approved banks like Co-operative Bank, Westpac, or Unity. Some offer cashbacks, e.g., BNZ's $5,000 for loans $250,000+.

- Get Pre-Approval: Submit income proof, credit history. Lenders assess affordability – debt-to-income ratios matter.

- Find Your Home: Properties must pass Kāinga Ora valuation. Aim for under $900k average to fit income caps.

- Sign and Settle: Pay LMI upfront (add to loan if needed). Choose fixed, floating, or split rates.

In 2026, with lenders approving more low-deposit loans amid stable markets, it's a 'Goldilocks year' for first-home buyers – don't sleep on it.

Participating Lenders List

- Unity Money (0800 229 943)

- Kiwibank

- Westpac

- BNZ

- SBS Bank

- Co-operative Bank

Visit Kāinga Ora's site for the full, updated list.

Pros and Cons of 5% Deposit Home Loans

Like any tool, it has trade-offs. Weigh them carefully.

Pros

- Faster Entry: Save $75,000+ on a $500k home vs 20%.

- Flexible Funds: Gifts, KiwiSaver, grants stack up.

- Custom Structures: Fixed (e.g., 12 months at Unity), floating, or offsets.

- Equity Build: Own sooner, benefit from price rises.

Cons

- LMI Cost: 1.2% of loan (e.g., $5,700 on $475k) – non-refundable.

- Higher Risk: Negative equity if prices dip; harder to refinance.

- Income Caps: Excludes higher earners.

- No 100% Loans: Unless parent guarantee (risky for families).

Practical Tips for First-Home Buyers in 2026

Make your application bulletproof:

- Crunch Numbers: Use Canstar or MoneyHub calculators for repayments. At 6% interest, a $475k loan is ~$2,860/month over 30 years.

- Clean Credit: Pay debts; check your Equifax score free via banks.

- Regional Focus: Easier in South Island; Auckland options limited by price/income.

- Extra Help: Pair with KiwiBuild new builds or First Home Grant.

- Timing: 2026's lender leniency means more approvals – act now.

- Seek Advice: Free sessions from Sorted.org.nz or mortgage brokers.

Next Steps to Secure Your First Home Loan

Ready to move? Start today: check eligibility on Kāinga Ora's site, gather docs (payslips, bank statements), and contact 2-3 lenders for quotes. Track 2026 market shifts – with more approvals flowing, your dream home awaits. Chat to a broker for personalised advice, and you'll be unpacking boxes sooner than you think.

Frequently Asked Questions

Sources & References

-

1

First Home Loans - 5% Deposit, Kāinga Ora, NZ — unitymoney.co.nz

-

2

Low-Deposit Home Loans — www.moneyhub.co.nz

-

3

First Home Loan — kaingaora.govt.nz

-

4

Financial help for first-home buyers — www.govt.nz

-

5

Kāinga Ora First Home Loan | First home buyer hub — www.co-operativebank.co.nz

-

6

First Home Loan — www.kiwibank.co.nz

-

7

First Home Loan — www.westpac.co.nz

-

8

Home loans for first home buyers — www.sbsbank.co.nz

-

9

Low deposit home lending — www.bnz.co.nz

-

10

Why 2026 is a 'Goldilocks year' for first-home buyers — www.1news.co.nz