Notice Saver Accounts NZ: Higher Interest With Flexibility

Looking to boost your savings without fully committing to a term deposit? Notice Saver accounts in New Zealand offer a smart middle ground—higher interest rates than standard savings accounts paired w...

The Lifetimes NZ editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes NZ readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Looking to boost your savings without fully committing to a term deposit? Notice Saver accounts in New Zealand offer a smart middle ground—higher interest rates than standard savings accounts paired with the flexibility to access your money when you need it, as long as you give the required notice.

These accounts are perfect for Kiwis who want their cash working harder in today's low-rate environment, especially with the Official Cash Rate (OCR) holding steady into 2026. Whether you're building an emergency fund, saving for a house deposit, or parking KiwiSaver-like funds short-term, Notice Savers deliver competitive returns while keeping your options open.

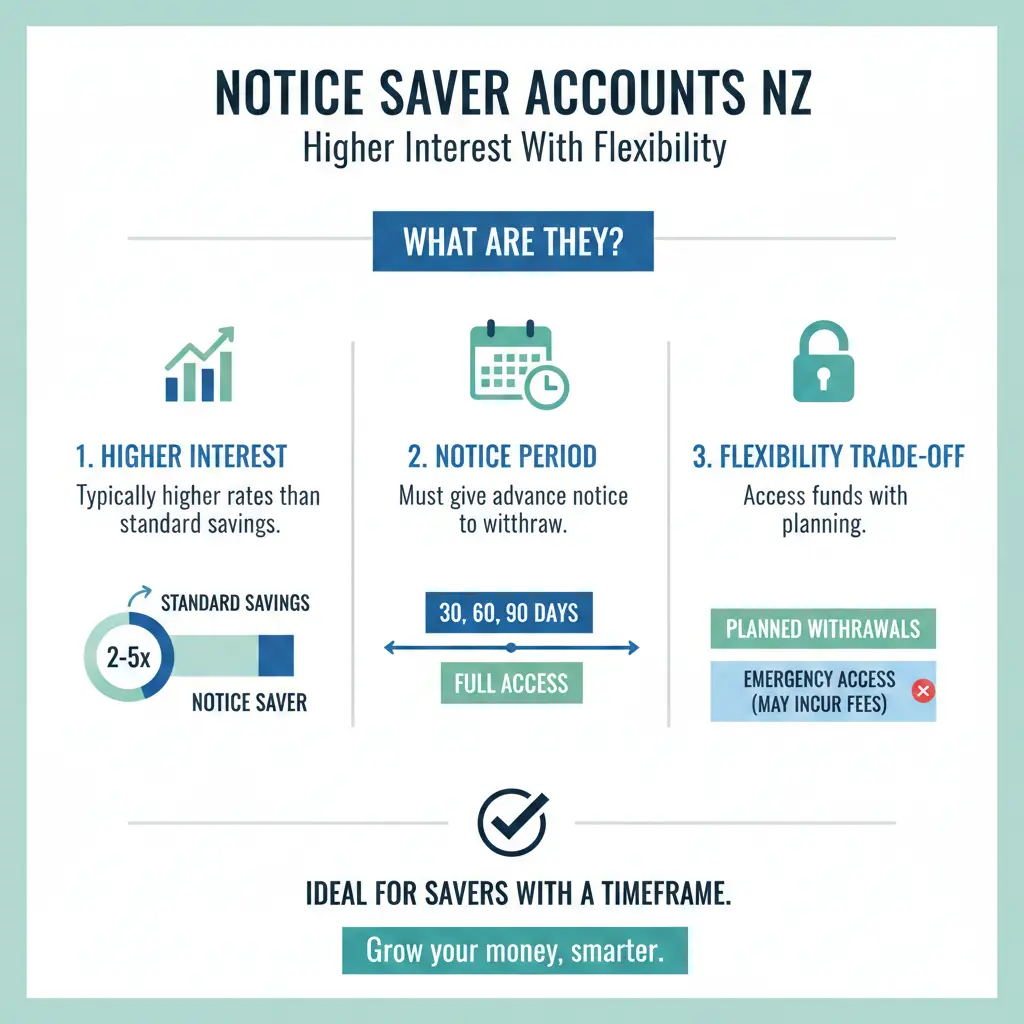

What Are Notice Saver Accounts NZ?

Notice Saver accounts are a type of savings account where you agree to provide the bank with advance notice—typically 32, 60, or 90 days—before withdrawing funds. This notice period lets banks offer higher interest rates than everyday call accounts, as they can plan their lending more reliably.

Unlike term deposits, which lock your money away for a fixed period with penalties for early access, Notice Savers give you flexibility. You can give notice online anytime, and once the period ends, your money is available without fuss. No minimum deposits or monthly fees in most cases, making them accessible for everyday Kiwis.

How Notice Saver Accounts Work

- Give notice digitally: Log into your online banking and request a withdrawal. The bank processes it after the notice period.

- Earn interest daily: Rates apply to your full balance, calculated daily and paid monthly.

- Early withdrawal options: Possible but with adjustments—often the difference between your Notice Saver rate and a lower call rate, plus a fee (e.g., Heartland's minimum $12).

- Balance limits: Up to $5-10 million, ideal for larger savers.

This setup suits those who can plan ahead, like retirees drawing income or families saving for school fees.

Current Notice Saver Interest Rates in NZ (2026)

As of early 2026, Notice Saver rates hover between 1.55% and 3.00% p.a., outpacing standard high-interest savings (often under 2%) but below short-term deposits (up to 3.05% for 30-90 days).

Here's a comparison of top providers:

| Bank | Interest Rate (p.a.) | Notice Period | Min Balance | Balance Limit | PIE? |

|---|---|---|---|---|---|

| Heartland Bank | 2.95% (90 days) / 2.70% (32 days) | 32 or 90 days | $0 | $5m | No |

| Rabobank | 2.55% | 60 days | $0 | $5m | No |

| Kiwibank | 2.10% (90 days) / 1.55% (32 days) | 32 or 90 days | $0 | None | Yes |

| Westpac | 3.00% | 32 days | $0 | $10m | Yes |

Rates are variable and tied to OCR movements—check providers directly for the latest, as they can shift weekly.

Why Choose Notice Savers for Higher Interest with Flexibility?

Top Benefits for Kiwis

- Higher returns: Beat call accounts (e.g., RaboSaver at 1.30%) by 1-2%, helping your savings grow faster against inflation.

- Flexibility over term deposits: No breakage fees if you stick to notice; term deposits charge heavily for early access.

- No fees or mins: Open with $0, no account charges—great for testing the waters.

- Scalable: High limits suit big balances, unlike some savings caps.

PIE Tax Advantages

Portfolio Investment Entities (PIEs) cap tax on interest at your Prescribed Investor Rate (PIR)—28% max for most, vs. your income tax rate (up to 39%). Ideal if you're on 33% or 39% brackets.

Example ($10,000 at 5.50% p.a. for 1 year):

- PIE (28% tax): Gross $550 → Tax $154 → Net $396

- Non-PIE (39% tax): Gross $550 → Tax $214.50 → Net $335.50

- Non-PIE (33% tax): Net $368.50

Kiwibank and Westpac PIEs shine for higher earners; set your PIR via IRD myIR.

Notice Saver vs Other Savings Options in NZ

| Account Type | Interest Rate Range | Access | Best For |

|---|---|---|---|

| Notice Saver | 1.55-3.00% | 32-90 days notice | Planners wanting higher rates |

| High-Interest Savings (e.g., ANZ Serious Saver) | Up to 1.50-2.00% | Instant (with conditions) | Easy access, bonuses for discipline |

| Term Deposits | 1.80-3.05% (30-90 days) | Locked term, penalties | Short-term certainty |

Notice Savers win for balance of rate and access—only four banks offer them: Heartland, Rabobank, Kiwibank, Westpac.

Are Notice Saver Accounts Safe? Regulations and Protections

Yes—deposits up to $100,000 per depositor per bank are protected under the Financial Markets Authority (FMA) and Reserve Bank oversight. KiwiSaver providers often use similar structures, but always check FSCS-like coverage (NZ Deposit Guarantee scheme ended 2011, now it's open bank resolution).

Interest is RWT-taxed automatically (or PIR for PIEs)—report via IRD for compliance.

How to Open a Notice Saver Account in NZ

- Compare rates: Use sites like MoneyHub or Canstar for latest.

- Check eligibility: NZ resident, 18+, ID required (passport/driver's licence).

- Apply online: 5-10 mins via bank sites—e.g., Heartland or Westpac.

- Fund it: Transfer from another account; set up auto-payments for growth.

- Give notice wisely: Plan withdrawals around notice to avoid adjustments.

Pro tip: Ladder accounts across banks for diversification and max rates.

Practical Tips to Maximise Your Notice Saver

- Match notice to needs: 32 days for frequent access (Westpac 3.00%), 90 for max rate (Heartland 2.95%).

- Automate deposits: From salary or KiwiSaver windfalls.

- Monitor OCR: Rates may rise if Reserve Bank hikes in 2026.

- Combine with budgets: Use alongside WINZ or StudyLink savings goals.

- Review annually: Switch if better deals emerge—no exit fees.

Ready to Grow Your Savings?

Notice Saver accounts deliver the higher interest with flexibility Kiwis crave in 2026's steady-rate world. Pick Westpac for quick 32-day access at 3.00% or Heartland for top 90-day yields—calculate your net returns using PIE perks if applicable.

Next steps:

- Compare live rates on bank sites today.

- Confirm your PIR on ird.govt.nz.

- Open an account and shift spare cash—watch it compound monthly.

- Track via apps like PocketSmith for full financial control.

Your gateway to smarter saving starts now—flexible growth awaits!

Frequently Asked Questions

Sources & References

-

1

Compare Notice Saver Accounts in New Zealand - MoneyHub NZ — www.moneyhub.co.nz

-

2

Online Savings Interest Rates - Rabobank — www.rabobank.co.nz

-

3

Ranking New Zealand's best and worst savings accounts - Squirrel — www.squirrel.co.nz

-

4

Best High Interest Savings Accounts in New Zealand - Canstar — www.canstar.co.nz

-

5

Notice Saver | Heartland Bank — www.heartland.co.nz

-

6

Notice Saver | Westpac NZ — www.westpac.co.nz

-

7

Notice Saver | Savings & investments - Kiwibank — www.kiwibank.co.nz

-

8

Interest Rate Predictions 2026 & 2027 - MoneyHub NZ — www.moneyhub.co.nz

-

9

ANZ Term Deposits | PIE funds — www.anz.co.nz

Related Articles

Term Deposits vs. Index Funds: Where to Park Your Cash in 2026

I appreciate the detailed request, but I need to be transparent about a limitation: the search results provided contain information about term deposit rates in New Zealand for 2026, but they don't inc...

Currency Conversion Hacks for NZ Travelers

Heading overseas? Nothing kills the buzz of a Kiwi holiday faster than getting slugged with hefty currency conversion fees or snagging a lousy exchange rate. With the New Zealand dollar hovering aroun...

Best NZ Banks for Small Business Owners

Running a small business in New Zealand means juggling cash flow, customers, and endless admin—choosing the right bank shouldn't add to the stress. With the Big Four banks—BNZ, ASB, ANZ, and Westpac—d...

Emergency Funds 101: How Much Cash Should a Kiwi Family Have?

Picture this: a sudden storm hits your neighbourhood in Auckland, just like the severe weather event in January 2026, leaving your home flooded and power out for days. Without an emergency fund, you'r...