Bonus Saver Accounts NZ: Rules and Best Options 2025

If you're looking to make your savings work harder, a bonus saver account could be the perfect fit. These accounts reward you for growing your balance each month, offering interest rates significantly...

Sarah covers personal finance, tax, and KiwiSaver topics for Lifetimes NZ. She focuses on making money management straightforward and practical for everyday Kiwis.

If you're looking to make your savings work harder, a bonus saver account could be the perfect fit. These accounts reward you for growing your balance each month, offering interest rates significantly higher than standard savings accounts. In New Zealand, several major banks offer bonus saver options with rates up to 1.60% p.a., making them an attractive choice for disciplined savers who want accessible funds without the restrictions of term deposits.

What is a Bonus Saver Account?

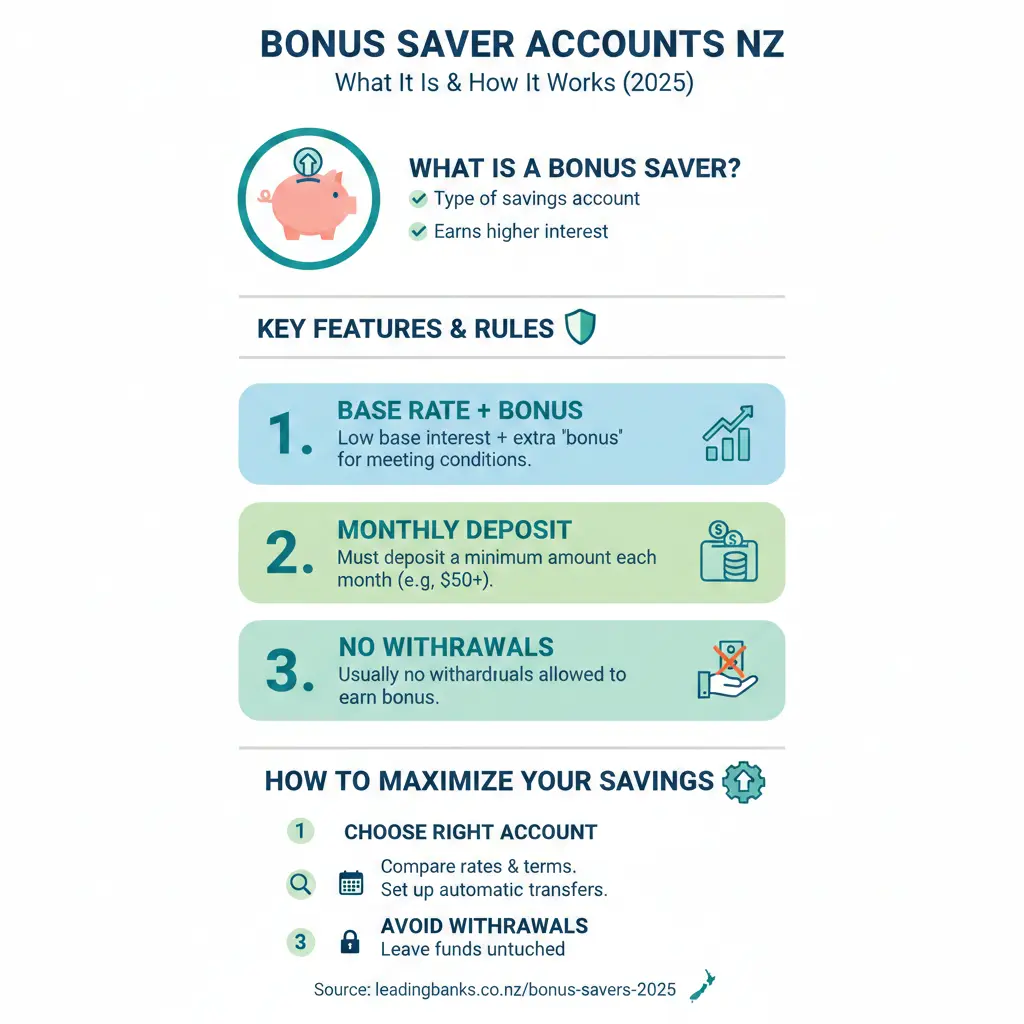

A bonus saver account is a savings product designed to reward committed savers. Unlike standard savings accounts that offer a flat interest rate, bonus savers combine a low base interest rate with a much higher bonus interest rate. The bonus portion kicks in when you meet specific conditions—typically by growing your balance each month or making regular deposits.

The key advantage is flexibility. You get immediate access to your money with unlimited withdrawals, unlike term deposits where your funds are locked away. This makes bonus savers ideal if you want higher returns but need to keep your money accessible for emergencies.

How Bonus Saver Accounts Work in New Zealand

The mechanics are straightforward. Each month, your bank checks whether you've met the bonus conditions. If you have, you'll earn the bonus interest rate on top of the base rate. If you haven't, you'll only receive the base interest rate—which is typically very low (around 0.05% p.a.).

The most common condition is a minimum balance increase. For example, Westpac's Bonus Saver requires your balance to be at least $20 greater than the previous month's balance to qualify for the full bonus interest. This $20 threshold excludes interest earned and any bank fees charged.

Interest is compounded monthly or paid monthly to another account, depending on your preference. This means your savings grow faster as you earn interest on your interest.

Best Bonus Saver Accounts in New Zealand

Westpac Bonus Saver: Up to 1.25% p.a.

Westpac's Bonus Saver offers a potential rate of return of up to 1.25% p.a.. The account has no monthly maintenance fees, though service fees like clearance fees still apply. You'll get unlimited withdrawals and can set up automatic payments to ensure your monthly deposit is made on time.

To earn the full bonus interest, your balance needs to be $20 greater than the previous month's balance. The bank recommends setting up an automatic payment for the middle of each month to ensure you meet this threshold.

ASB Savings Plus: Up to 1.60% p.a.

ASB's Savings Plus offers the highest advertised rate among major banks at up to 1.60% p.a.. However, it comes with stricter conditions: you can only make one withdrawal on the first day of the month to earn the full reward interest.

The account has a base interest rate of 0.05% and a bonus interest rate of 1.55%. This structure means you need to be disciplined about when you withdraw funds.

Non-Bank Options: Booster Savvy

If you're open to non-traditional options, Booster Savvy offers 2.25% p.a.. However, it's important to note that Booster Savvy is a managed investment scheme, not a standard bank account. It's not covered by the Depositor Compensation Scheme (DCS), so you should read the Product Disclosure Statement before investing.

Important Rules and Conditions

Depositor Compensation Scheme Protection

All savings accounts with New Zealand banks are covered by the Depositor Compensation Scheme (DCS). This protects your deposits up to $100,000 per deposit taker. It's worth checking whether your chosen account is DCS-covered, especially if you're using non-bank providers.

Be aware that some innovative investment products, like Booster Savvy, aren't covered by the DCS due to their investment nature.

Meeting the Bonus Conditions

The critical rule is consistency. You must meet the bonus conditions every single month to earn the higher interest rate. Missing the threshold even once means you'll only earn the base rate for that month.

For accounts requiring a minimum balance increase, remember that the increase is measured by actual deposits, not interest earned. This is why setting up automatic transfers on a regular schedule works so well—it removes the guesswork.

Withdrawal Restrictions

While bonus savers offer unlimited withdrawals, some accounts impose conditions on when you can withdraw without affecting your bonus. ASB's Savings Plus, for example, limits you to one withdrawal on the first day of the month. Always check your account terms before making unexpected withdrawals.

Bonus Saver vs. Other Savings Options

Bonus Saver vs. Term Deposits

Term deposits currently offer higher rates—ranging from 1.80% to 3.05% for 30 to 90-day terms. However, your money is locked away for the entire term. If you need to access funds early, you'll face penalty charges and potentially lose interest. Bonus savers are better if you value flexibility.

Bonus Saver vs. Notice Saver Accounts

Notice saver accounts require you to give advance notice (typically 32, 60, or 90 days) before withdrawing funds. They often offer rates between bonus savers and term deposits. Choose a notice saver if you're comfortable with a waiting period but want better rates than bonus savers offer.

Bonus Saver vs. Standard Savings Accounts

Standard savings accounts offer low, flat interest rates. Bonus savers are significantly better if you can meet the monthly conditions. The difference between a 0.05% base rate and a 1.25% bonus rate is substantial over time.

Tips for Maximising Your Bonus Saver

- Automate your deposits: Set up an automatic transfer on the same day each payday. This ensures you meet the bonus conditions without thinking about it.

- Pay yourself first: Before spending anything, transfer a set amount to your savings account. This builds discipline and ensures consistent growth.

- Track your balance: Know exactly what you need to deposit each month to meet the threshold. For Westpac, it's just $20.

- Avoid unnecessary withdrawals: The fewer withdrawals you make, the easier it is to grow your balance and maintain the bonus conditions.

- Compare rates regularly: Interest rates change, so review your account annually to ensure you're getting the best deal.

- Consider the full picture: Look at base rates, bonus rates, fees, and withdrawal conditions together. The highest advertised rate isn't always the best option for your situation.

Common Questions About Bonus Saver Accounts

Can I withdraw money from a bonus saver account anytime?

Yes, most bonus saver accounts offer unlimited withdrawals. However, some accounts (like ASB's Savings Plus) have conditions on when you can withdraw without affecting your bonus interest. Always check your specific account terms.

What happens if I don't meet the bonus conditions one month?

You'll only earn the base interest rate (typically 0.05%) for that month. You can earn the bonus again the following month if you meet the conditions.

How is interest calculated on a bonus saver account?

Interest is compounded monthly, meaning you earn interest on your interest. The interest can either be added to your account or paid monthly to another account, depending on your preference.

Are bonus saver accounts covered by the Depositor Compensation Scheme?

Yes, bonus saver accounts with New Zealand banks are covered by the DCS, protecting deposits up to $100,000. However, non-bank investment products may not be covered, so verify with your provider.

Which bonus saver account is best for me?

It depends on your priorities. If you want the highest rate and can commit to one withdrawal per month, ASB's Savings Plus offers 1.60% p.a.. If you prefer simplicity and flexibility, Westpac's Bonus Saver at 1.25% p.a. requires minimal effort—just a $20 monthly increase.

Should I choose a bonus saver or a term deposit?

Choose a bonus saver if you need access to your money. Choose a term deposit if you can lock your funds away for the full term and want higher interest rates (currently 1.80% to 3.05%).

Getting Started with a Bonus Saver Account

Opening a bonus saver account takes just minutes with most banks. You can apply online through your bank's website. Most major New Zealand banks—including Westpac, ASB, BNZ, ANZ, Kiwibank, and TSB—offer bonus saver options.

Before committing, check upfront with your financial institution and read the applicable documentation to confirm whether the account terms meet your needs. Pay particular attention to the bonus conditions, withdrawal limits, and any fees that might apply.

Disclaimer: This article is for informational purposes only and shouldn't be considered financial advice. Interest rates and account features change regularly. Always verify current rates and terms directly with your bank before opening an account. For personalised financial advice, consult a qualified financial adviser.

Sources & References

-

1

Revision of Bonus$aver Account — www.sc.com

-

2

Westpac Bonus Saver Account — www.westpac.co.nz

-

3

Best High Interest Savings Accounts in New Zealand — www.canstar.co.nz

-

4

Ranking New Zealand's Best and Worst Savings Accounts — www.squirrel.co.nz

-

5

NZ Super Recipients to Receive One-Off January Bonus — www.artbeat.org.nz

-

6

Compare Bonus Savings Accounts — finance.co.nz

-

7

Best Savings Options in New Zealand — kernelwealth.co.nz

-

8

Rapid Save — www.bnz.co.nz

-

9

Changes to Westpac Terms & Conditions & Notices — www.westpac.co.nz

-

10

Best Bank Accounts – February 2026 — www.moneyhub.co.nz

Related Articles

Industry Bodies and Professional Associations NZ

Whether you're launching a business, advancing your career, or navigating financial regulations, industry bodies and professional associations in New Zealand offer invaluable support. These organisati...

Emergency Benefit NZ: When You Have No Other Options

When you're struggling financially and don't qualify for other benefits, the Emergency Benefit might be your lifeline. It's a discretionary payment designed for Kiwis in genuine hardship who've exhaus...

Unpaid Internships NZ: Are They Legal?

Unpaid internships are a common pathway for students and graduates to gain work experience in New Zealand, but there's often confusion about whether they're actually legal. The short answer is: unpaid...

Estate Administration NZ: Managing Someone's Affairs After Death

Losing a loved one is one of life's toughest challenges, and stepping in to manage their estate can feel overwhelming. In New Zealand, estate administration—the process of handling someone's affairs a...