PIE Funds vs Regular Savings: Tax Advantages Explained

Imagine earning interest on your savings, only to watch a big chunk disappear to tax at your personal income rate of up to 39%. Now picture keeping more of those returns because they're taxed at a cap...

Sarah covers personal finance, tax, and KiwiSaver topics for Lifetimes NZ. She focuses on making money management straightforward and practical for everyday Kiwis.

Imagine earning interest on your savings, only to watch a big chunk disappear to tax at your personal income rate of up to 39%. Now picture keeping more of those returns because they're taxed at a capped rate of just 28%—or even lower. That's the reality for many Kiwis choosing between PIE funds and regular savings accounts, where tax efficiency can make a real difference to your nest egg.PIE Funds vs Regular Savings boils down to smarter tax treatment through the Prescribed Investor Rate (PIR), potentially saving you thousands over time.

In New Zealand's current financial landscape (2026), with inflation lingering and interest rates fluctuating, understanding these options is crucial for everyday savers, families, and those building towards retirement. PIEs, or Portfolio Investment Entities, were designed to encourage long-term saving, including via KiwiSaver, by simplifying tax and capping it below top income rates. This article breaks down the tax advantages, compares real-world scenarios, and gives you actionable steps to maximise your returns.

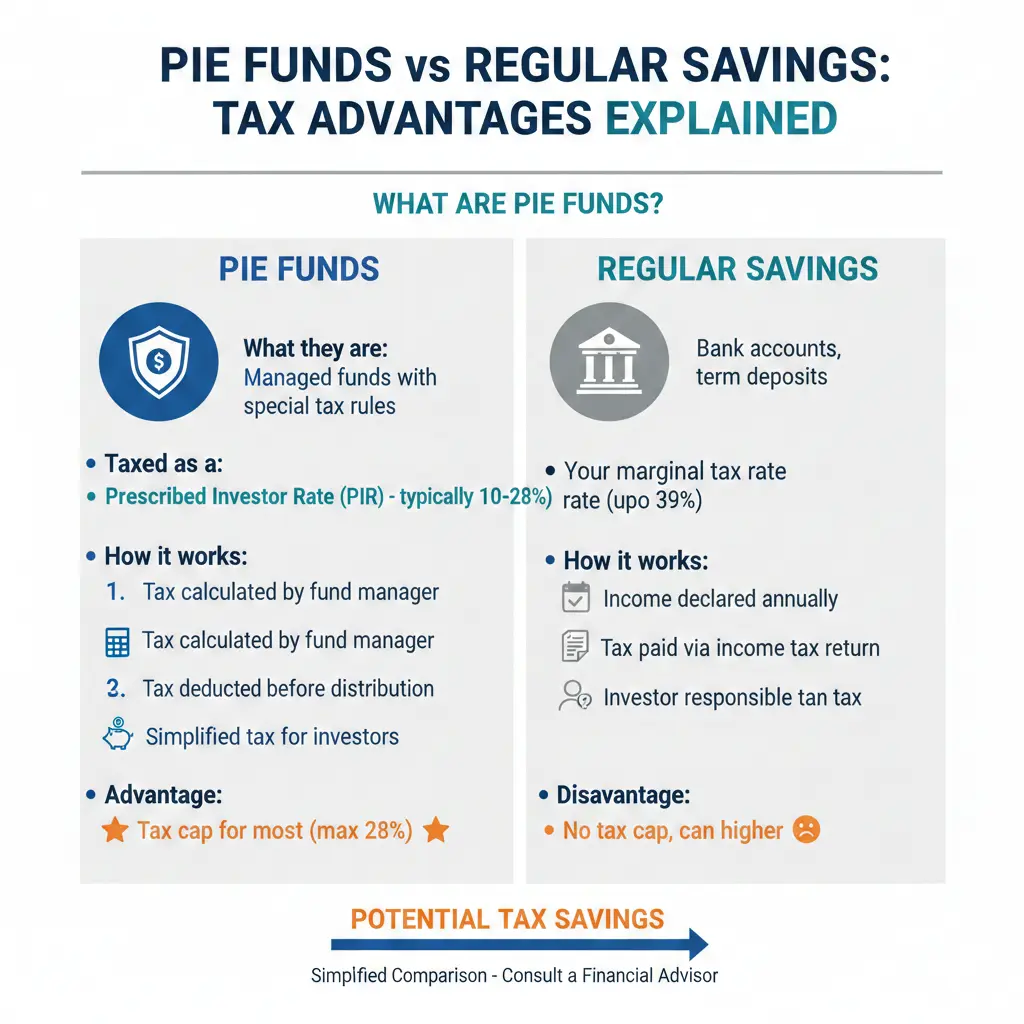

What Are PIE Funds?

PIE funds are managed investment vehicles approved by the IRD, pooling money from multiple investors to buy assets like shares, bonds, or cash equivalents. Unlike traditional bank accounts, PIEs tax returns at your PIR—10.5%, 17.5%, or 28%—based on your income over the last two years, not your current marginal rate.

Your KiwiSaver is almost always a PIE, automatically applying these rules. Standalone PIEs, like term PIEs or cash PIE funds from providers such as Pie Funds or BNZ, offer similar benefits for non-retirement savings. Tax is calculated daily and deducted quarterly, with final liability settled via IRD—no need for manual claims unless your PIR changes.

How PIE Tax Works in Practice

To invest, provide your IRD number and correct PIR within six weeks, or your account closes. Use the IRD's PIR calculator: if your total income (plus PIE returns) was under $53,500 over the past two years, opt for 10.5%; $53,501–$78,100 gets 17.5%; above that, it's 28%. Get it wrong? IRD notifies your provider, and you might owe extra at year-end (April 1–March 31).

- 10.5% PIR: Ideal for low/no earners, like students or new parents on leave.

- 17.5% PIR: Suits middle-income Kiwis up to $78,100 total.

- 28% PIR: Caps tax for higher earners, beating 33% or 39% income rates.

PIEs report directly to IRD via MyIR, keeping things simple.

Regular Savings Accounts and Term Deposits: The Traditional Route

Bank savings accounts and term deposits earn interest taxed as income at your marginal rate: 10.5% up to $15,600, 17.5% to $53,500, 30% to $78,100, 33% to $180,000, and 39% above. Resident Withholding Tax (RWT) is deducted upfront, but you reconcile via your tax return.

For trusts, it's even tougher at 33% or 39% over $10,000. No cap means high earners lose more: a 39% taxpayer on 5% interest keeps just 3.05% after tax, versus potentially more in a PIE.

Key Drawbacks for Tax

- Interest pushes you into higher brackets, taxing portions progressively.

- No daily calculation—full amount hits your annual return.

- Less flexibility for retirees or variable incomes.

PIE Funds vs Regular Savings: Head-to-Head Tax Comparison

The core advantage? PIEs cap tax at 28%, often below your income rate, letting returns compound faster. Here's a 2026 comparison assuming $10,000 invested at 5% gross return:

| Income Bracket (Taxable Income) | Regular Savings Tax Rate | PIE PIR | After-Tax Return (Regular) | After-Tax Return (PIE) | Annual Tax Saving |

|---|---|---|---|---|---|

| Under $15,600 | 10.5% | 10.5% | $4,450 | $4,450 | $0 |

| $15,601–$53,500 | 17.5% (effective) | 17.5% | $4,175 | $4,175 | $0 |

| $53,501–$78,100 | 30% | 28% | $3,500 | $3,600 | $100 |

| $78,101–$180,000 | 33% | 28% | $3,350 | $3,600 | $250 |

| $180,001+ | 39% | 28% | $3,050 | $3,600 | $550 |

For trusts: 33%/39% vs 28% saves 5–11%. Over 10 years compounding, that $550 annual saving grows to over $8,000 extra.

Real Kiwi Examples

Take Sarah, earning $60,000: 30% tax on savings interest leaves her with less. Switching to a PIE at 28% saves 2% yearly. Nadia, post-redundancy with no income, uses 10.5% PIR in a BNZ Term PIE, slashing tax from 33%. High-earner Mike ($200,000) caps at 28% in Pie Funds, beating 39% and harnessing diversification.

"If your PIR is lower than your income tax rate, you will pay less tax on your savings in a PIE than in a regular savings account."

Other PIE Advantages Beyond Tax

PIEs offer liquidity (cash PIEs like Kernel Wealth beat term deposits without lock-ins), diversification, and professional management. Many yield competitively: Pie Funds' cash options rival 4–5% term deposits post-tax.

Risks to Consider

- Market risk: Non-cash PIEs fluctuate unlike fixed savings.

- Fees: 0.5–1% management fees erode low returns.

- PIR errors: Overstate and reclaim; understate and pay later.

PIEs suit horizons over 1–3 years; short-term? Stick to savings.

Practical Tips for Kiwis

- Check your PIR: Use IRD's tool annually.

- Start small: Try a term PIE from Westpac or BNZ for easy transition.

- Link to KiwiSaver: Boost contributions for matching and tax perks.

- Monitor via MyIR: Track PIE income automatically.

- Diversify: Mix cash PIEs with growth funds from Pie Funds.

For WINZ recipients or StudyLink borrowers, low PIR keeps more in your pocket without affecting benefits.

Disclaimer: This is general information, not personalised financial advice. Consult a licensed adviser or IRD for your situation. Tax rules can change; rates current as of 2026.

Next Steps to Boost Your Savings

Ready to save on tax? Log into MyIR for your PIR, compare PIE options from Pie Funds, Westpac, or BNZ, and shift $5,000+ from savings today. Track progress quarterly and review annually. Pair with KiwiSaver contributions for government matching. Small changes compound—start now for a richer retirement.

Frequently Asked Questions

Sources & References

-

1

The benefits of Portfolio Investment Entities (PIE) | Westpac NZ — www.westpac.co.nz

- 2

-

3

Tax on Investments and Savings in a Nutshell 2026 - MoneyHub NZ — www.moneyhub.co.nz

-

4

Is a PIE right for you? | Westpac NZ — www.westpac.co.nz

- 5

-

6

Cash Fund, Term Deposit or Saving Account: Which Do I Choose? | Kernel Wealth — kernelwealth.co.nz

- 7

-

8

Care more about your KiwiSaver savings - Pie Funds Guide (PDF) — www.piefunds.co.nz

-

9

Pie Fund vs Term Deposit: What NZ Investors Should Know | News Insights — www.newsinsights.co.nz

-

10

Fund Performance & Fund Types | Pie Funds NZ — www.piefunds.co.nz

Useful Tools

Related Articles

Industry Bodies and Professional Associations NZ

Whether you're launching a business, advancing your career, or navigating financial regulations, industry bodies and professional associations in New Zealand offer invaluable support. These organisati...

Emergency Benefit NZ: When You Have No Other Options

When you're struggling financially and don't qualify for other benefits, the Emergency Benefit might be your lifeline. It's a discretionary payment designed for Kiwis in genuine hardship who've exhaus...

Unpaid Internships NZ: Are They Legal?

Unpaid internships are a common pathway for students and graduates to gain work experience in New Zealand, but there's often confusion about whether they're actually legal. The short answer is: unpaid...

Estate Administration NZ: Managing Someone's Affairs After Death

Losing a loved one is one of life's toughest challenges, and stepping in to manage their estate can feel overwhelming. In New Zealand, estate administration—the process of handling someone's affairs a...