Resident Withholding Tax: Understanding RWT on Savings

Ever wondered why your bank statement shows a chunk of your hard-earned interest vanishing before it hits your account? That's Resident Withholding Tax (RWT) at work, automatically deducting tax on yo...

The Lifetimes NZ editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes NZ readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Ever wondered why your bank statement shows a chunk of your hard-earned interest vanishing before it hits your account? That's Resident Withholding Tax (RWT) at work, automatically deducting tax on your savings interest and dividends as a New Zealand tax resident. Understanding RWT helps you avoid nasty end-of-year surprises from IRD and ensures you're not overpaying on your KiwiSaver, term deposits, or savings accounts.

In this guide, we'll break down how RWT applies to your savings, the current 2026 rates, and practical steps to get it right—tailored for Kiwis managing everyday finances.

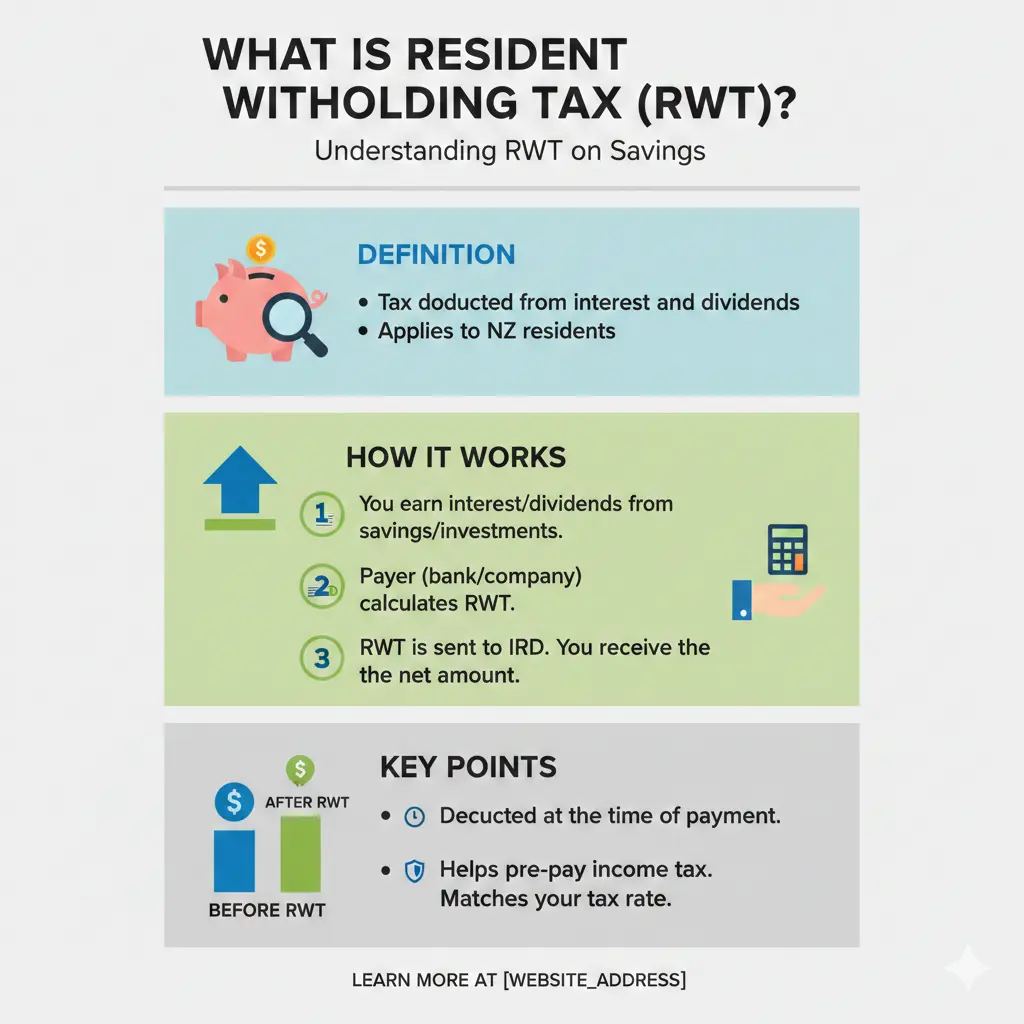

What is Resident Withholding Tax (RWT)?

RWT is a tax deducted at source on interest and dividends earned by New Zealand tax residents from local bank accounts and investments. Your bank or investment provider (the 'payer') withholds the tax before paying you, simplifying things for IRD while ensuring you pay tax on investment income as it arises.

Unlike PAYE on wages, RWT targets passive income like savings interest. It's your responsibility to provide the correct rate to avoid under- or over-withholding, which could lead to a tax bill or refund come filing time.

Why Does RWT Matter for Your Savings?

For many Kiwis, savings in term deposits or high-interest accounts form a key part of financial security. But without the right RWT setup, you might lose more to tax than necessary—or face an IRD adjustment. In 2026, with inflation and rising rates, getting this right maximises your returns.

- Interest from savings accounts, term deposits, and bonds.

- Dividends from shares or unit trusts (at a flat 33%).

- Excludes Portfolio Investment Entities (PIEs), which use Prescribed Investor Rates (PIR).

Current RWT Rates for 2026

RWT rates align with your total taxable income brackets, updated from 31 July 2024 to reflect new thresholds. Choose the rate matching your expected income for the tax year (1 April to 31 March). If you don't specify, the default is 33%—or 45% without an IRD number.

RWT Rates Based on Total Taxable Income (From 31 July 2024)

| Total Taxable Income | RWT Rate |

|---|---|

| Up to $15,600 | 10.5% |

| $15,601 to $53,500 | 17.5% |

| $53,501 to $78,100 | 30% |

| $78,101 to $180,000 | 33% |

| $180,001 and over | 39% |

Note: These apply to individuals. Companies use 28%, 33%, or 39%; trustees and Māori authorities have options like 10.5% to 39%. Always match your rate to your actual income tax bracket to avoid adjustments.

Dividend-Specific Rules

Dividends are withheld at a flat 33% RWT, but imputation credits from company tax paid can offset this—potentially reducing your net tax. For example, if a company attaches credits, they act like pre-paid tax, claimable in your IR3 return.

How to Set Your RWT Rate When Opening a Savings Account

Provide your IRD number and selected RWT rate to your bank (e.g., BNZ, ANZ) when opening any account. Without an IRD number, expect 45% withholding—far higher than most need.

- Estimate your total taxable income (wages + investments + other).

- Match it to the table above.

- Notify your payer in writing or via their app/online banking.

- Update if your income changes (e.g., new job or retirement).

Practical tip: Use myIR to check your income details and past RWT—payers report monthly. For joint accounts, pick the highest earner's rate to cover both (income splits equally).

Joint Accounts and Special Cases

In joint accounts, RWT applies to all interest, split equally if IRD numbers are provided. Example: If one partner earns over $78,100 and the other under $15,600, choose 33% to avoid a bill for the higher earner.

Mixed resident/non-resident joints? Full RWT deducts; non-residents claim refunds via IR3NR or IR386.

Common Mistakes and How to Avoid End-of-Year Tax Bills

Using the wrong rate is the top pitfalls—too low means an IRD bill; too high means a refund wait. IRD tracks all via myIR, so discrepancies show up fast.

- No IRD number: 45% flat rate—provide it ASAP.

- Outdated rate: Notify changes immediately (e.g., salary rise).

- Joint mismatches: Default to the highest income bracket.

- Forgetting dividends: Always 33%, but check credits.

Actionable advice: Review annually before 31 March. Tools like IRD's RWT calculator (via myIR) help.

RWT Exemptions: Who Qualifies?

Exemptions are rare for individuals but possible if you'll earn over $2 million or expect a $500+ refund due to losses. Apply via IR451 form; if approved, get a certificate for your payer.

Trustees or high earners might qualify conditionally—check IRD's exemption register. Note: No blanket exemptions for most Kiwis.

RWT and KiwiSaver or Other Investments

KiwiSaver uses PIR (10.5%, 17.5%, 28%), not standard RWT—update your PIR with providers like your KiwiSaver fund. From 1 April 2026, default contributions rise to 3.5%, but ESCT (employer tax) bands stay aligned with RWT rates.

For term deposits or savings outside PIEs, stick to RWT rules. Overseas interest? Report on IR3, no auto-withholding.

Steps to Manage RWT Effectively in 2026

- Log into myIR: Verify income and past RWT.

- Contact your bank: Update IRD and rate today.

- Estimate income: Include wages, benefits (WINZ), and investments.

- File accurately: Reconcile in your 2026 IR3 (due July 2026).

- Seek advice: Chat with a tax advisor for complex setups like trusts.

Pro tip: Bundle savings with KiwiSaver for PIR efficiency if eligible.

Next Steps to Optimise Your Savings Tax

Don't let RWT catch you out—log into myIR today, confirm your rate with banks, and align it to 2026 brackets. Track via monthly updates, and consult a professional for personalised advice (this isn't it—seek an accountant or IRD).

Maximise returns by choosing high-interest accounts with correct withholding. For WINZ recipients or StudyLink borrowers, factor in all income. Stay compliant, save smarter.

Disclaimer: This is general info based on 2026 rules. Tax laws change; get tailored advice from a qualified advisor or IRD.

Frequently Asked Questions

Sources & References

-

1

Using the right resident withholding tax (RWT) rate — ird.govt.nz — www.ird.govt.nz

-

2

New Zealand - Individual - Other tax credits and incentives — taxsummaries.pwc.com — taxsummaries.pwc.com

-

3

Resident withholding tax (RWT) — ird.govt.nz — www.ird.govt.nz

-

4

Understanding resident withholding tax (RWT) — bnz.co.nz — www.bnz.co.nz

-

5

Tax on investments and savings — govt.nz — www.govt.nz

-

6

New Zealand taxes: guide for US expats — taxesforexpats.com — www.taxesforexpats.com

Related Articles

Working Multiple Jobs NZ: Tax and Legal Considerations

Juggling multiple jobs can boost your income, but it's crucial to understand the tax implications and legal requirements that come with working more than one role in Aotearoa. Whether you're a contrac...

Name Changes NZ: Legal Process and Costs

Considering a fresh start with a new name? Whether it's after marriage, divorce, or simply embracing a personal transformation, changing your name in New Zealand is straightforward but requires follow...

Holiday Home Tax Rules NZ: Private Use and Rental

Own a bach in Coromandel or a holiday home in Queenstown? You're not alone—many Kiwis cherish these escapes, but renting them out while enjoying personal use can trip you up on tax rules. Getting the...

Industry Bodies and Professional Associations NZ

Whether you're launching a business, advancing your career, or navigating financial regulations, industry bodies and professional associations in New Zealand offer invaluable support. These organisati...