Emergency Funds 101: How Much Cash Should a Kiwi Family Have?

Picture this: a sudden storm hits your neighbourhood in Auckland, just like the severe weather event in January 2026, leaving your home flooded and power out for days. Without an emergency fund, you'r...

Sarah covers personal finance, tax, and KiwiSaver topics for Lifetimes NZ. She focuses on making money management straightforward and practical for everyday Kiwis.

Picture this: a sudden storm hits your neighbourhood in Auckland, just like the severe weather event in January 2026, leaving your home flooded and power out for days. Without an emergency fund, you're scrambling for cash to cover repairs, food, and temporary accommodation while waiting on insurance. An emergency fund is your financial lifeline, giving Kiwi families peace of mind amid rising costs and unpredictable events.

In 2026, with bills squeezing household budgets tighter than ever, building this safety net is more crucial. How much cash should a Kiwi family have? Experts recommend 3-6 months of essential expenses, but let's break it down for New Zealand realities like KiwiSaver, WINZ support, and local emergencies.

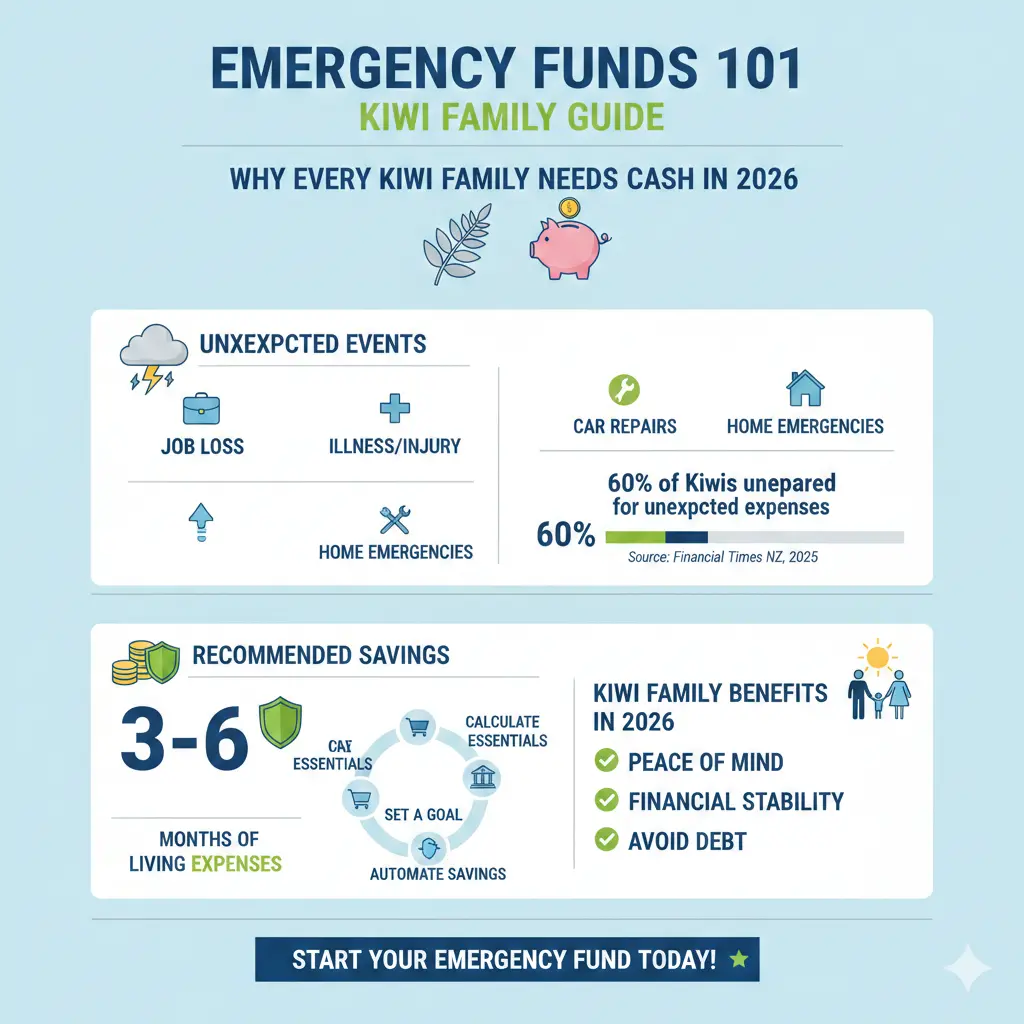

Why Every Kiwi Family Needs an Emergency Fund in 2026

Life in Aotearoa throws curveballs—think cyclones, job loss, or medical surprises. Recent events like the January 2026 severe weather remind us that preparation beats panic. Emergency funds cover essentials without racking up debt or dipping into retirement savings like KiwiSaver.

According to financial guides updated for 2026, around half of Kiwis worry about money due to rising costs, subscriptions, and living expenses. An emergency fund reduces that stress, acting as a buffer against inflation and unexpected hits like the new Fire and Emergency levy starting July 2026.

New Zealand-Specific Risks to Plan For

- Natural disasters: Floods, earthquakes, or storms. The Insurance Council offers recovery guidance post-2026 events, but cash upfront bridges the gap.

- Health emergencies: ACC covers injuries, but gaps in private insurance or wait times mean out-of-pocket costs.

- Job loss: With WINZ benefits taking weeks, 3 months' expenses keep you afloat.

- Cost-of-living spikes: Higher power bills, groceries, and the $25 motor vehicle levy from July 2026 add pressure.

Communities can tap funds like Auckland's $1m Climate and Emergency Ready Fund for preparedness projects, but personal savings remain key.

How Much Should Your Kiwi Family Save? The 3-6 Months Rule

The golden rule for how much cash a Kiwi family should have in an emergency fund is 3-6 months of essential living expenses. Start with 3 months if you're building from scratch; aim for 6 if you have dependents or unstable income.

Calculate Your Target Amount Step-by-Step

- List essentials: Rent/mortgage, groceries, utilities, transport, insurance, minimum debt payments. Exclude luxuries like takeaways or streaming.

- Monthly total: Add up. Average Kiwi household essentials: $5,000-$7,000/month in 2026, per cost-of-living updates.

- Multiply: 3 months = $15,000-$21,000; 6 months = $30,000-$42,000.

- Adjust for family size: Singles: 3 months. Families with kids: 6+ months, factoring school costs or childcare.

Example: A family of four in Wellington with $6,000 monthly essentials needs $18,000-$36,000. Homeowners factor the new $107.40 max Fire and Emergency levy.

| Family Type | Monthly Essentials (2026 est.) | 3 Months Target | 6 Months Target |

|---|---|---|---|

| Single, renter | $3,500 | $10,500 | $21,000 |

| Couple, no kids | $5,000 | $15,000 | $30,000 |

| Family of 4, mortgage | $7,000 | $21,000 | $42,000 |

This table uses 2026 cost estimates; tweak for your region—higher in Auckland, lower in smaller towns.

Where to Keep Your Emergency Fund: Best Options for Kiwis

Keep it accessible, safe, and earning interest. Avoid shares or property—stick to cash equivalents.

Top New Zealand Accounts for 2026

- High-interest savings accounts: Banks like ANZ, BNZ offer 4-5% rates (check current promos). No fees, easy access.

- Term deposits: 3-6 month terms for part of the fund, yielding 4.5-5.5%.

- KiwiSaver notice savers: Some providers allow 90-day notice withdrawals for emergencies (not ideal for true liquidity).

- Offset accounts: Linked to mortgages, reducing interest without locking funds.

Prioritise FSCS-like protection via the Financial Markets Authority (FMA). Aim for at least 20% in instant access.

Step-by-Step Guide to Building Your Emergency Fund

Don't aim for the full amount overnight. Consistency wins in 2026's tough economy.

Practical Tips Tailored for Kiwis

- Track spending: Use apps like PocketSmith or bank tools. Cut subscriptions—many families waste $50+/month.

- Save 10-20% of income: Post-bills, auto-transfer to savings. Build KiwiSaver alongside (aim 10-15% total for retirement).

- Windfalls first: Tax refunds, bonuses, or IRD payments go straight in.

- Side hustles: TradeMe sales, Uber, or local gigs. Families report trimming wants frees $200/week.

- Debt strategy: Pay high-interest debt (credit cards >15%) before maxing the fund, but keep 1 month's buffer.

- Review quarterly: Adjust for Budget 2026 changes or levy hikes.

Start small: $1,000 buffer, then one month's expenses. Momentum builds.

Common Mistakes Kiwis Make with Emergency Funds

- "I'll start next month": Procrastination leaves you exposed. Automate now.

- Mingling with other savings: Label it "Emergency Only" mentally.

- Too aggressive investing: Term deposits beat shares for liquidity.

- Ignoring family needs: Kids' extras like uniforms push targets higher.

- Not updating post-events: Rebuild after using it for 2026 weather damage.

Your Next Steps to Financial Security

Grab a coffee, list your essentials tonight, and set up an auto-save of $50/week. In 6 months, you'll have a solid start. Review post-July 2026 levies and Budget updates. You're not alone—thousands of Kiwi families are building resilience one dollar at a time. Check bank rates today and protect your whānau.

Frequently Asked Questions

Sources & References

-

1

Insurance-based levy to fund Fire and Emergency New Zealand — www.dia.govt.nz

-

2

Fire and Emergency levy for 2026-2029 — www.fireandemergency.nz

-

3

Apply now for Auckland's new $1m Climate and Emergency Readiness Fund — ourauckland.aucklandcouncil.govt.nz

-

4

How much of my paycheck should I be saving? (NZ Guide for 2026) — www.kourawealth.co.nz

-

5

How to Start Planning for 2026 | NZ Financial Guide — www.provincialwealth.co.nz

-

6

Severe Weather Event January 2026: Insurance Recovery Guidance — www.civildefence.govt.nz

-

7

10 Things to Do Differently with Money in 2026 - MoneyHub NZ — www.moneyhub.co.nz

-

8

Budget 2026 | The Treasury New Zealand — www.treasury.govt.nz

-

9

Goodbye Extra Savings — NZ Families Say Bills Are Out of Control — www.artbeat.org.nz

Related Articles

Currency Conversion Hacks for NZ Travelers

Heading overseas? Nothing kills the buzz of a Kiwi holiday faster than getting slugged with hefty currency conversion fees or snagging a lousy exchange rate. With the New Zealand dollar hovering aroun...

Best NZ Banks for Small Business Owners

Running a small business in New Zealand means juggling cash flow, customers, and endless admin—choosing the right bank shouldn't add to the stress. With the Big Four banks—BNZ, ASB, ANZ, and Westpac—d...

Best Savings Accounts in NZ 2025 (Highest Interest Rates)

Want to make your money work harder in 2026? With inflation still biting and everyday costs rising, Kiwis are turning to high-interest savings accounts to beat the squeeze. In this guide, we round up...

Best Term Deposit Rates NZ 2025: Where to Lock In

Looking to secure your savings with the best term deposit rates NZ 2025 – or rather, lock in top returns for 2026? With the Reserve Bank of New Zealand (RBNZ) keeping the Official Cash Rate (OCR) stea...