Natural Disaster Insurance in NZ: What EQC Covers

Imagine waking up to the ground shaking violently beneath your Kiwi home, or watching floodwaters rise after a fierce storm—scenarios all too familiar in our beautiful but geologically active country....

Sarah covers personal finance, tax, and KiwiSaver topics for Lifetimes NZ. She focuses on making money management straightforward and practical for everyday Kiwis.

Imagine waking up to the ground shaking violently beneath your Kiwi home, or watching floodwaters rise after a fierce storm—scenarios all too familiar in our beautiful but geologically active country. As homeowners, we all want peace of mind knowing we're protected against these unpredictable events. That's where natural disaster insurance in New Zealand steps in, with the Natural Hazards Commission (NHC)—formerly the Earthquake Commission (EQC)—providing that essential first layer of cover.

But what exactly does NHC cover? In this guide, we'll break it down clearly, so you know precisely what's included, what's not, and how it fits with your private insurance. Whether you're buying your first home or reviewing your policy, understanding natural disaster insurance in NZ: what EQC covers (now under NHC) is crucial for safeguarding your biggest asset.

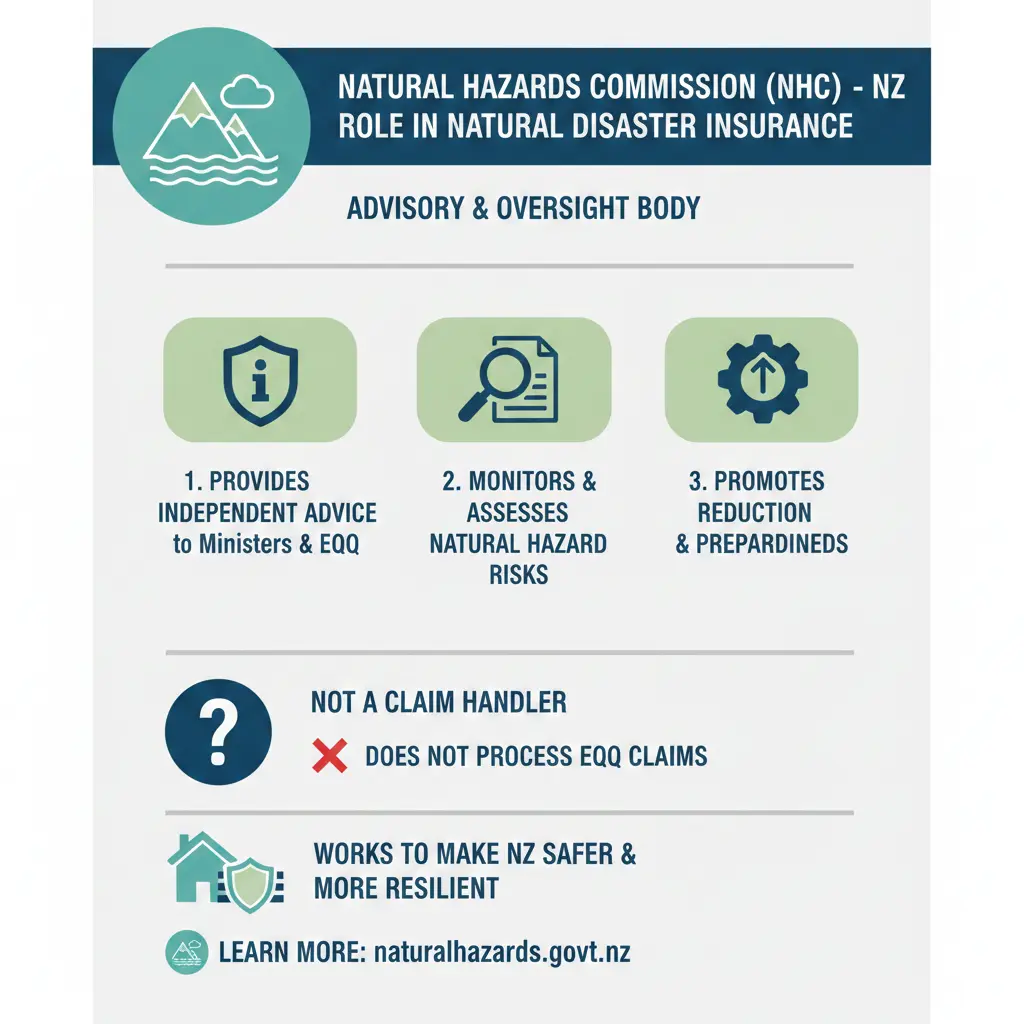

What is the Natural Hazards Commission (NHC)?

Established decades ago to tackle our nation's high risk of earthquakes, the NHC has evolved significantly. Originally known as the Earthquake Commission (EQC), it rebranded to the Natural Hazards Commission Toka Tū Ake in 2024, reflecting a broader mandate to cover various natural disasters beyond just earthquakes.

The shift came through the Natural Hazards Insurance Act 2023, effective from 1 July 2024, replacing the outdated Earthquake Commission Act 1993. This legislation incorporates lessons from events like the Canterbury earthquakes and the 2020 Public Inquiry into the EQC, expanding protection to more hazards while modernising operations.

Every Kiwi homeowner with private home insurance that includes fire cover automatically gets NHC cover—no extra application needed. It's funded via an annual levy, typically around $552 (including GST) baked into your insurance premium, costing about $46 a month for most.

Key Changes Since 2022

- Cap Increase: From 1 October 2022, the residential building cap rose from $150,000 to $300,000 (excluding GST), now at $345,000 including GST for events post-1 October 2022.

- Broader Hazards: Now includes storms, floods (land only), landslides, tsunamis, and volcanic activity.

- Claims Window: Extended to two years from the event, giving you more time to lodge.

- No Contents Cover: Phased out since 2019; rely on private contents insurance.

These updates ensure better financial resilience, backed by a Crown guarantee on the Natural Hazard Fund and expanded reinsurance to $10.3 billion as of 2026.

What Does NHC Cover Exactly?

NHC provides natural disaster insurance in NZ as the first $345,000 (inc. GST) layer for your dwelling and limited land damage. Your private insurer covers anything above that cap, plus other elements like contents and temporary accommodation.

Covered Natural Hazards

NHC steps in for damage from:

- Earthquakes

- Volcanic activity

- Tsunamis

- Landslides and landslips

- Storm-related land damage

- Hydrothermal activity

- Fire following any of these events

Specific Coverage Details

Dwelling (Home): Up to $345,000 (inc. GST) for repairs or rebuilding the residential building itself. This applies to damage from eligible events like earthquakes or landslips.

Land: Covers damage within your property boundary, including:

- Debris, silt, or loosened soil from flooding or storms

- Landslips affecting land or structures

- Up to 8m around the house

- Main driveway/accessway up to 60m from the house

- Bridges, culverts, retaining walls supporting land or access

Urgent Repairs: You can make immediate safety fixes post-event, with NHC contributing as part of your settlement.

"Our natural hazards cover provides the first layer of insurance cover for your home, and limited cover for your land."

What NHC Does NOT Cover

Knowing the gaps is vital—NHC isn't a full replacement for private insurance. It excludes:

- Flood damage to buildings (private insurance covers this)

- Contents inside your home

- Vehicles, plants, crops, livestock

- Non-main access paths

- Theft post-disaster

- Temporary accommodation costs

- Damage from poor maintenance or non-natural causes

For example, after Auckland's 2023 floods, NHC helped with land cleanup like silt removal, but building repairs fell to private policies.

Imminent Damage and Exceptions

NHC covers "imminent damage" if instability from an event (e.g., landslip) likely causes issues within a year under normal conditions.

However, no cover if you bought land with a known risk flagged by a section 36 or 72 notice on the title for the same hazard. Check your LIM report or title via Land Information New Zealand (LINZ).

How NHC Fits with Your Private Insurance

Think of it as a layered system: NHC handles the first $345,000 for eligible damage, then your insurer covers the excess. This eases the load on private providers, as seen post-Canterbury where reinsurers paid $5 billion.

| Aspect | NHC Cover | Private Insurance |

|---|---|---|

| Building Damage | First $345k (inc. GST) | Above cap + flood to buildings |

| Land Damage | Property boundary limits | Often limited or excluded |

| Contents | None | Full cover if insured |

| Temporary Accommodation | None | Usually 10-12 months |

Always confirm your policy includes NHC levy—most do automatically.

How to Make an NHC Claim in 2026

- Lodge Promptly: Within two years of the event via naturalhazards.govt.nz or 0800 800 242.

- Provide Details: Photos, damage description, cause, repair quotes.

- Assessment: NHC inspects to confirm event, damage, and costs—repair or replace value.

- Settlement: Pays first layer; notifies your private insurer if over cap.

- Urgent Repairs: Proceed if safe, claim reimbursement.

Pro tip: Document everything with timestamps and geolocations. If disputed, seek free advice from Community Law or Insurance & Financial Services Ombudsman.

Real-Life Examples from New Zealand

During the 2010-2011 Canterbury sequence, original $100,000 caps led to overcap reassessments years later, highlighting the need for clear communication.

In 2023's North Island weather bombs, NHC covered landslips and storm debris, while private insurers handled flooded homes—saving claimants time.

Auckland Anniversary floods showed land-only flood cover in action: silt cleanup funded, but building fixes via private policies.

Practical Tips for Kiwi Homeowners

- Review Annually: Ensure your sum insured matches rebuild costs via BRANZ tools.

- Mitigate Risks: Install retaining walls or drains; NHC may fund if event-triggered.

- Bundle Policies: Get comprehensive private cover for floods, contents.

- Check Title: Search LINZ for s36/s72 notices before buying.

- Stay Informed: Sign up for GeoNet alerts and NHC updates.

Frequently Asked Questions

Related Articles

Life Insurance NZ: Are You Overpaying for Cover You Don't Need?

Ever signed up for life insurance without a second thought, only to watch your premiums climb year after year? You're not alone—many Kiwis are paying for life insurance NZ cover they don't actually ne...

Health Insurance NZ: Complete Guide to Going Private

Imagine facing a sudden health scare in New Zealand—long public hospital waits could stretch weeks or months, but with private health insurance, you could access top specialists and private rooms swif...

Travel Insurance NZ: What to Look For Before You Go

Picture this: you're hiking the Tongariro Crossing, the mist rolling off the emerald lakes, when a sudden twist of ankle leaves you stranded. No worries if you've got the right travel insurance NZ—but...

Pet Insurance NZ 2025: Is It Worth the Cost?

Imagine coming home to your loyal labrador, only to find them limping after a sudden accident. A trip to the vet reveals surgery costs over $5,000—money you hadn't budgeted for. This scenario plays ou...