KiwiSaver at 65: Your Withdrawal Options Explained

Turning 65 marks a pivotal moment for Kiwis who've diligently saved through KiwiSaver—it's when those locked-away funds finally become accessible, offering flexibility to shape your retirement just as...

Sarah covers personal finance, tax, and KiwiSaver topics for Lifetimes NZ. She focuses on making money management straightforward and practical for everyday Kiwis.

Turning 65 marks a pivotal moment for Kiwis who've diligently saved through KiwiSaver—it's when those locked-away funds finally become accessible, offering flexibility to shape your retirement just as you've envisioned it. Whether you're dreaming of fortnightly income to cover living expenses, a lump sum for that overdue overseas trip, or keeping your savings invested for the long haul, understanding your options ensures you make choices aligned with your lifestyle and financial goals.

Understanding KiwiSaver Access at Age 65

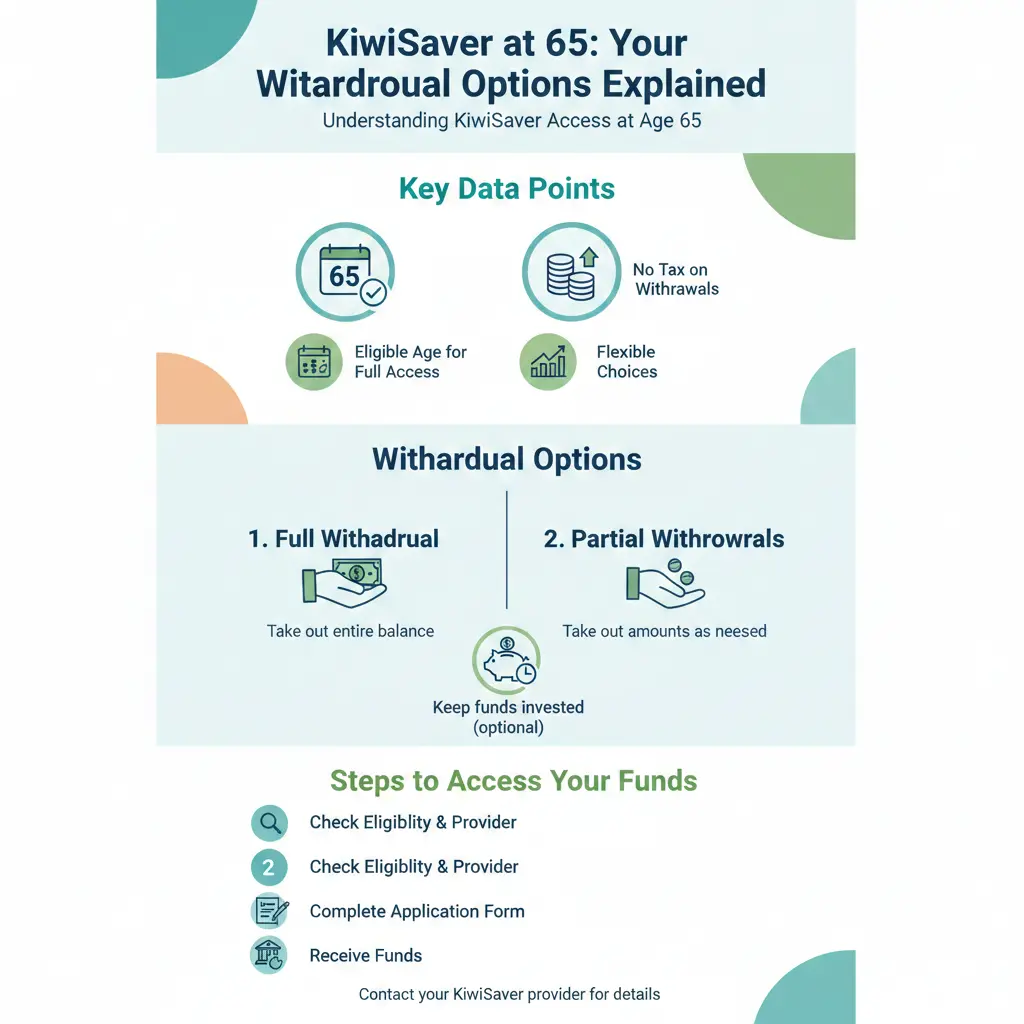

KiwiSaver is designed to support New Zealanders through retirement, with funds generally locked until you qualify for New Zealand Superannuation at age 65. Once you hit this milestone, your account transforms from a savings vehicle into a versatile retirement tool. You gain the freedom to withdraw as needed, but importantly, there's no obligation to cash everything out immediately.

Key changes at 65 include:

- Full access to your balance without restrictions tied to employment or contributions.

- No more Member Tax Credits from the government, as these end after age 65.

- Employers are no longer required to contribute, though some may continue voluntarily if you're still working.

This shift empowers you to decide how best to use your savings alongside New Zealand Super and any pensions like those from ACC or private super schemes. Remember, while KiwiSaver doesn't affect your NZ Super eligibility, how you withdraw can impact your overall tax position—always check with IRD for personalised advice.

Who Qualifies and When?

You become eligible on your 65th birthday, regardless of when you joined KiwiSaver. If you joined before 1 July 2019 and were aged 60-64 at the time, older rules once locked you in for five years—but 2026 legislation allows you to opt out immediately at 65, halting employer and government contributions if you choose. For those joining at or after 65, no statutory declaration is needed for withdrawals.

Your KiwiSaver Withdrawal Options at 65

Flexibility is the hallmark of KiwiSaver at 65. Providers like ASB, Aurora, and Westpac offer straightforward methods to access your funds, typically processed within 5-10 business days. Here's a breakdown of the main options:

1. Regular Retirement Withdrawals

Set up systematic payments to mimic a salary—fortnightly, monthly, or quarterly. A minimum of $100 per withdrawal applies with many providers, making it ideal for covering bills, groceries, or hobbies without depleting your nest egg too quickly.

- Practical tip: Align payments with your NZ Super schedule (paid fortnightly) for steady cash flow.

- Continue investing the remainder to combat inflation and potentially grow your savings further.

2. Lump Sum Withdrawals

Need cash for a new caravan, home renovations, or unexpected medical costs? Request a partial lump sum via your provider's retirement withdrawal form. This keeps the bulk of your KiwiSaver invested while giving you immediate access.

Example: If your balance is $300,000, you could withdraw $50,000 for a family wedding, leaving the rest to generate returns.

3. Full Account Closure

Withdraw everything in one go if you prefer to roll funds into a term deposit, buy an annuity, or manage investments elsewhere. Be aware: closing means starting fresh if you want KiwiSaver-like benefits later, and you'll forgo ongoing investment growth within the scheme.

Caution: This option suits those with alternative income streams but risks outliving your savings in a long retirement.

4. Keep It Invested and Withdraw as Needed

Many Kiwis opt to leave funds in KiwiSaver post-65, drawing down gradually. Your account continues earning returns, and you can contribute voluntarily if desired—perfect if you're semi-retired or supporting whānau. Providers recommend this to ensure funds last your lifetime.

Smart Drawdown Strategies: Rules of Thumb

Deciding how much to withdraw requires balancing enjoyment today with security tomorrow. ASB outlines practical heuristics tailored for Kiwis, though these are general guides—not personalised advice.

| Strategy | How It Works | Best For | Example ($200,000 Balance) |

|---|---|---|---|

| 6% Rule | Withdraw 6% of initial balance annually. | Higher early income, no inheritance focus. | $12,000/year. |

| Fixed Date Rule | Divide balance by years to a target date (e.g., 20 years). | Maximise early, other income later. | $10,000/year for 20 years. |

| Life Expectancy Rule | Annual withdrawal = balance / remaining life expectancy. | Lifetime income maximisation. | Adjust yearly (e.g., ~$13,000 at 65 assuming 15 years). |

These strategies ignore taxes, fees, and market volatility—factor in your full financial picture, including KiwiSaver growth assumptions of 4-7% annually (net of fees, based on historical averages).

How to Make Your First KiwiSaver Withdrawal

The process is straightforward and provider-agnostic:

- Contact your provider: Download the retirement withdrawal form from their website or app (e.g., ASB's form at asb.co.nz).

- Complete requirements: First-timers need a statutory declaration witnessed by a JP, lawyer, or similar. Scan and email, post, or visit a branch.

- Specify details: Choose amount, frequency, and bank account. Minimums apply (e.g., $100).

- Wait for processing: 5-7 days for partials, 8-10 for closures.

- Tax considerations: Withdrawals are taxed at your PIR (Prescribed Investor Rate)—check yours via IRD.govt.nz. No tax on the withdrawal itself, but subsequent investments may be.

Pro tip: Use Sorted.org.nz's retirement planner to model scenarios before applying.

Tax Implications and Other Considerations

Post-65 withdrawals use your existing PIR for PIE tax (10.5%, 17.5%, or 28% bands). Update it if your income changes to avoid overpaying—log into myIR. KiwiSaver growth remains tax-advantaged inside the scheme.

Other factors:

- NZ Super integration: ~$500/week (2026 rates, after tax) for couples; KiwiSaver supplements this without clawback.

- Inflation and fees: Aim for growth funds if healthy; conservative if risk-averse. Average fees ~0.5% p.a.

- Inheritance: Funds pass to your estate tax-free if undrawn.

- Disclaimer: This isn't financial advice. Consult a licensed adviser or use free services like Sorted.org.nz for your situation.

Common Pitfalls to Avoid

- Rushing full withdrawal—many outlive lump sums.

- Ignoring fees on transfers to banks or other schemes.

- Forgetting to notify your employer if opting out pre-65 lock-in.

- Not reviewing your fund's performance annually via canstar.co.nz or provider statements.

Frequently Asked Questions

Related Articles

Industry Bodies and Professional Associations NZ

Whether you're launching a business, advancing your career, or navigating financial regulations, industry bodies and professional associations in New Zealand offer invaluable support. These organisati...

Emergency Benefit NZ: When You Have No Other Options

When you're struggling financially and don't qualify for other benefits, the Emergency Benefit might be your lifeline. It's a discretionary payment designed for Kiwis in genuine hardship who've exhaus...

Unpaid Internships NZ: Are They Legal?

Unpaid internships are a common pathway for students and graduates to gain work experience in New Zealand, but there's often confusion about whether they're actually legal. The short answer is: unpaid...

Estate Administration NZ: Managing Someone's Affairs After Death

Losing a loved one is one of life's toughest challenges, and stepping in to manage their estate can feel overwhelming. In New Zealand, estate administration—the process of handling someone's affairs a...