Financial Goals: How to Plan for 2025-2026

As we step into 2025, many Kiwis are feeling the pinch from lingering high interest rates and cost-of-living pressures, but there's never been a better time to take control of your financial planning...

The Lifetimes NZ editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes NZ readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

As we step into 2025, many Kiwis are feeling the pinch from lingering high interest rates and cost-of-living pressures, but there's never been a better time to take control of your financial planning NZ 2025 strategy. Whether you're building towards buying a home, boosting your KiwiSaver, or aiming for retirement comfort, a solid plan for 2025-2026 can turn uncertainty into opportunity.

With Budget 2025 outlining government priorities and KiwiSaver tweaks on the horizon, now's the moment to align your personal finances with real-world changes. This guide breaks down practical steps tailored for New Zealanders, drawing on proven strategies to help you set goals, budget smartly, and invest wisely.

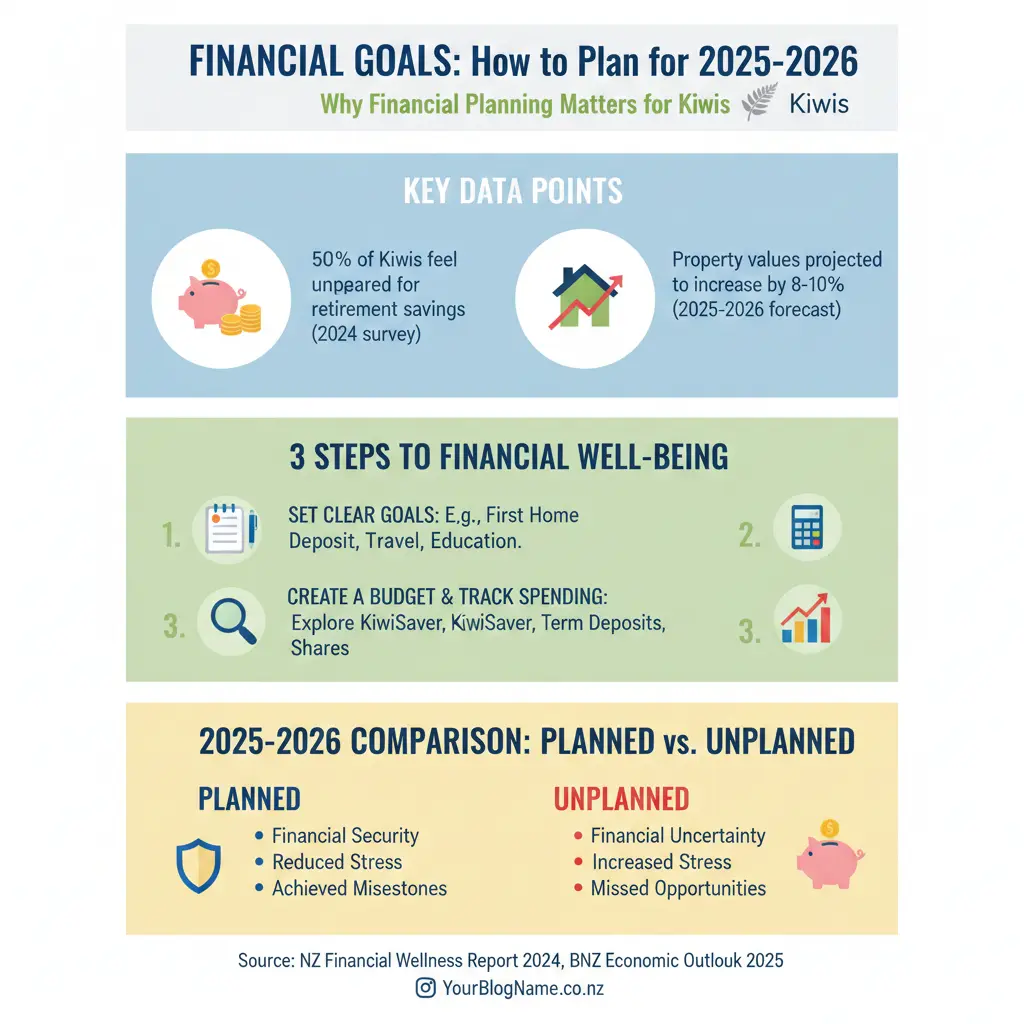

Why Financial Planning Matters for Kiwis in 2025-2026

Financial planning isn't just about numbers—it's about securing your future amid economic shifts. High inflation and interest rates have made saving tougher, but tools like KiwiSaver and the 50/30/20 budget rule can help you navigate it all. For instance, with mortgage rates still elevated, prioritising debt reduction and emergency funds is crucial before investing aggressively.

In New Zealand, our unique superannuation system means KiwiSaver plays a starring role in long-term planning. Recent guidelines suggest couples need to top up New Zealand Super by around $980 a week for a comfortable retirement in major cities, equating to a lump sum over $1 million. Starting now ensures you're not caught short.

Key Economic Factors Shaping 2025

- Interest rates: Expect OCR decisions from the Reserve Bank to influence mortgage refinancing—aim to lock in the lowest rates possible.

- Inflation: Budget 2025 focuses on fiscal stability, but household costs remain high, making budgeting essential.

- KiwiSaver changes: Contribution rates and fund options evolve—review yours annually.

Step 1: Set Clear, Achievable Financial Goals

Begin with goals that match your values, whether it's debt freedom by 50 or a family holiday fund. Categorise them as short-term (under 1 year), medium-term (1-5 years), or long-term (5+ years).

Examples of NZ-Specific Goals for 2025-2026

- Emergency fund: Build 3-6 months' expenses (or 6-12 for families) in a high-interest savings account. Target $10,000 initially.

- Debt payoff: Eliminate high-interest consumer debt like credit cards first—aim for under 10% debt-to-income ratio.

- Home deposit: Save for 20% to avoid LVR restrictions under Reserve Bank rules.

- Retirement boost: Increase KiwiSaver to 8% contributions and switch to growth funds if suitable.

- Investment milestone: Hit $100,000 in shares/funds by year 3 of a 10-year plan.

Calculate your net worth first: assets (KiwiSaver, savings, property equity) minus liabilities (mortgage, loans). Use free tools from sorted.org.nz for this snapshot.

Step 2: Master Your Budget with the 50/30/20 Rule

The 50/30/20 rule—50% needs, 30% wants, 20% savings—forms a solid foundation, adjustable to 70/20/10 if you're in a high-cost area like Auckland. Track income and expenses via apps like PocketSmith or a simple spreadsheet.

Practical Budgeting Tips for Kiwis

- Create dedicated accounts: emergency fund, short-term savings (holidays), long-term (retirement), even fun ones like takeaways.

- Automate everything: Set up auto-transfers to KiwiSaver and investments on payday.

- Review quarterly: Adjust for Budget 2025 changes, like any Working for Families tweaks.

- Lifestyle optimisation: Cut non-essentials to free up $1,000-$3,000 monthly for investments.

For a family of four, needs might include rent ($600/week), groceries ($250/week), and utilities—cap at 50% of after-tax income.

Step 3: Build Your Emergency Fund and Tackle Debt

Prioritise an "Oh Shit" fund covering 3-6 months' essentials in a separate, high-interest account—don't dip into it for Uber Eats. High-interest debt kills wealth; pay off credit cards (often 20%+ APR) before extra mortgage payments.

Debt Management Strategies

Consolidate loans for lower rates and refinance your mortgage when OCR drops—check canstar.co.nz for comparisons. Aim for debt elimination in Year 1 of your plan.

Step 4: Optimise KiwiSaver and Start Investing

KiwiSaver is your retirement powerhouse—health-check it now: increase to 8%, add voluntary contributions, and dollar-cost average into growth funds. For broader investing, diversify: 80% international shares by Year 7.

Investment Roadmap for 2025-2026

| Year | Focus | Milestones |

|---|---|---|

| 2025 (Year 1) | Foundation | $10k emergency fund, debt-free (non-mortgage), KiwiSaver at 8% |

| 2026 (Year 2) | Acceleration | $2k/month investments, side hustle launch |

| 2027+ (Years 3-5) | Growth | $100k portfolio, mortgage refinance, net worth tracking |

Property? Proceed cautiously—research risks thoroughly. Use platforms like Sharesies or Hatch for easy share access.

Step 5: Plan for Retirement and Protection

Aim for $1m+ lump sum to supplement NZ Super for comfort. Update wills, enduring powers of attorney, and insurance—especially health and life cover. Stress-test your portfolio quarterly.

Health and Legacy Planning

- Medical fund: Separate pot for dental/medical.

- Estate planning: By Year 7, review trusts via a adviser.

- Income streams: Build passive ones like dividends by Year 8.

Staying on Track: Reviews and Adjustments

Schedule annual reviews—end of financial year (March 31) aligns with IRD filings. Track net worth visually with charts. Life changes? Reassess goals immediately.

Your Next Steps for Financial Success

Grab a coffee, calculate your net worth today, and set one goal—like automating $500 to savings. Consult a financial adviser via fma.govt.nz's register for personalised advice. Revisit this plan quarterly, and by 2026, you'll be ahead of the curve. You've got this—kiwis thrive when we plan smart.

Frequently Asked Questions

Sources & References

-

1

How To Build Your 2025 Financial Plan — lighthousefinancial.co.nz

-

2

Financial Freedom by 50 - The 10-Year Plan That Actually Works — www.moneyhub.co.nz

-

3

Money & You - How to get ahead in 2025 — www.quantumgroup.nz

-

4

Step-by-Step Guide to Creating a Personal Financial Plan — www.accountantsplus.co.nz

-

5

2025 Retirement Expenditure Guidelines — www.unisaver.co.nz

-

6

Year-End To-Dos: 2025 Financial Planning Guide — www.manning-napier.com

-

7

Your 2025 Financial Planning Checklist — creativeplanning.com

-

8

A Guide to Investing in New Zealand - 2025 — www.russellmcveagh.com

-

9

Budget 2025 — www.treasury.govt.nz

-

10

Financial Planning Guide — www.fahb.co.nz

Related Articles

The "No-Spend" Month: How One Kiwi Saved $2;000 in 30 Days

Imagine looking at your bank account at the end of the month and seeing an extra $2,000 staring back at you—all because you said "no" to impulse buys, takeaways, and those sneaky coffee runs. That's e...

How to Calculate Your Take-Home Pay with the NZ Salary Calculator

Ever wondered why your bank account doesn't match that shiny new job offer? You're not alone—many Kiwis scratch their heads over the gap between gross salary and actual take-home pay. With New Zealand...

Budgeting for Beginners: The "50/30/20 Rule" Adjusted for NZ Salaries

Struggling to make your Kiwi paycheck stretch further? You're not alone—many of us feel the pinch from rising rents, grocery bills, and that tempting flat white habit. But what if a simple rule could...

How to Travel the World on a NZ Salary

Ever dreamed of sipping cocktails on a Thai beach or exploring the ancient ruins of Machu Picchu, all while earning a solid Kiwi wage? With New Zealand's average monthly salary hitting 5,666 NZD in 20...