Budgeting for Beginners: The "50/30/20 Rule" Adjusted for NZ Salaries

Struggling to make your Kiwi paycheck stretch further? You're not alone—many of us feel the pinch from rising rents, grocery bills, and that tempting flat white habit. But what if a simple rule could...

The Lifetimes NZ editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes NZ readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Struggling to make your Kiwi paycheck stretch further? You're not alone—many of us feel the pinch from rising rents, grocery bills, and that tempting flat white habit. But what if a simple rule could help you balance essentials, enjoy life, and still build a nest egg? Enter the 50/30/20 rule, adjusted for New Zealand salaries and our unique costs like KiwiSaver contributions and ACC levies. This beginner-friendly approach can transform your finances without the spreadsheet overwhelm.

In this guide, we'll break down the 50/30/20 rule, tweak it for NZ realities in 2026, and walk you through real examples using average Kiwi incomes. Whether you're on the median wage or just starting out, you'll get practical steps to budget smarter right here at home.

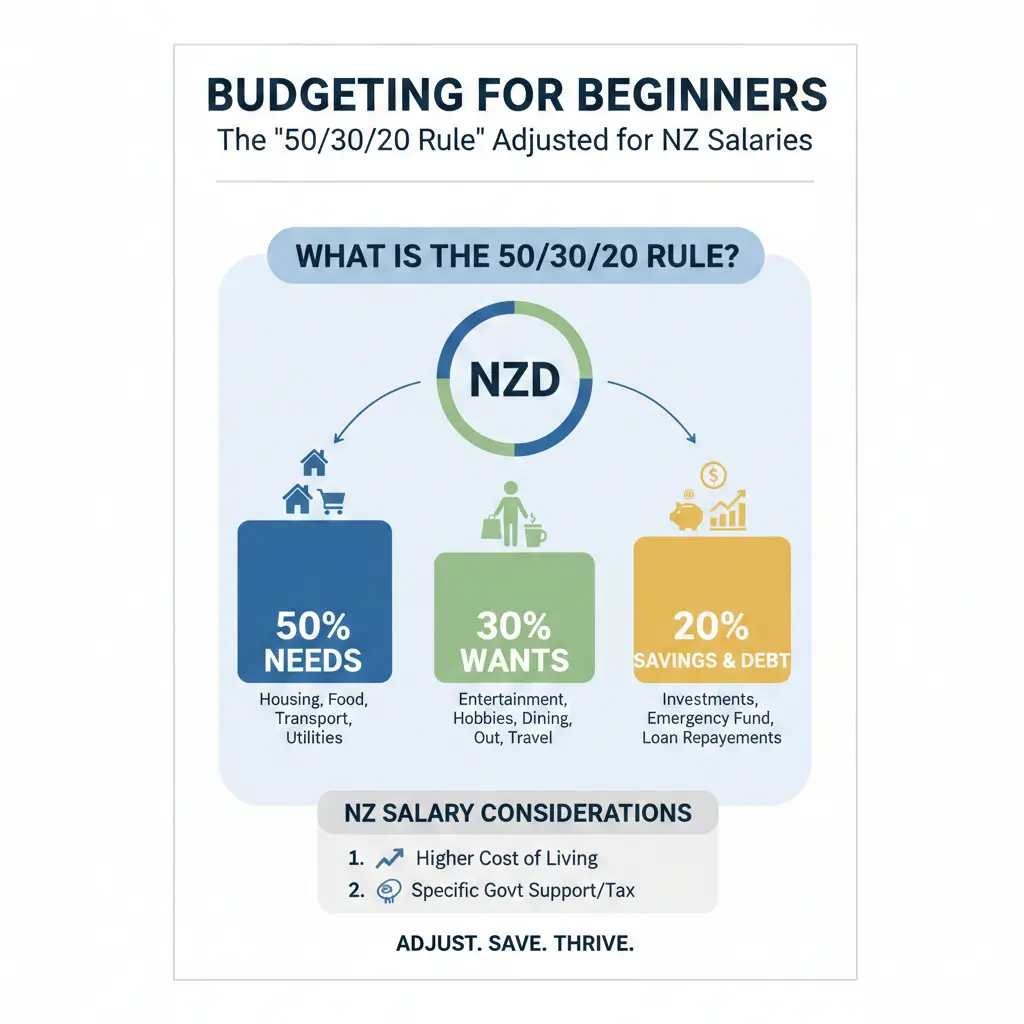

What is the 50/30/20 Rule?

The 50/30/20 rule is a straightforward budgeting framework that splits your after-tax income into three buckets: 50% for needs, 30% for wants, and 20% for savings or debt repayment. Popularised by US Senator Elizabeth Warren, it's gained traction worldwide for its simplicity—no need for complex apps or daily tracking.

- 50% Needs: Essentials you can't skip, like rent, groceries, power bills, and transport.

- 30% Wants: Fun stuff that makes life enjoyable, such as dining out, streaming subscriptions, or weekend adventures.

- 20% Savings/Debt: Building your future through KiwiSaver, emergency funds, or paying off credit cards and car loans.

It's not rigid; think of it as a guideline to create balance and awareness. In NZ, where living costs vary wildly from Auckland's sky-high rents to Dunedin's affordability, this rule shines by highlighting where to adjust.

Why Adjust the 50/30/20 Rule for NZ Salaries?

New Zealand's cost of living in 2026 demands tweaks to the classic rule. Median after-tax household income sits around $6,000 monthly, but fixed costs like housing often eat up more than 50% in cities. Factor in KiwiSaver (at least 3% mandatory), ACC levies, and student loans, and your take-home pay needs special consideration.

Common NZ adjustments include:

- 60/20/20: For high-cost areas like Auckland, bump needs to 60%, cut wants to 20%, keep savings at 20%.

- 70/20/10: If you're a single parent or facing unexpected bills, prioritise needs higher.

- 50/20/30: Flip wants and savings if you're debt-free and saving aggressively for a house deposit.

These shifts ensure the rule works for our realities, preventing debt while aligning with Kiwi values like work-life balance and homeownership dreams.

Average NZ Salaries in 2026

The median gross annual salary for full-time Kiwis is about $70,000, translating to roughly $4,500 monthly after tax and deductions (assuming standard KiwiSaver and no student loan). For households, it's closer to $95,000 annually or $6,000 monthly net. Use tools like MoneyHub's 50/30/20 calculator to personalise this—input your exact take-home pay post-IRD tax, KiwiSaver, and ACC.

Step-by-Step: Applying 50/30/20 to NZ Salaries

Ready to dive in? Follow these actionable steps tailored for Kiwis.

Step 1: Calculate Your After-Tax Income

Start with your net pay—the cash hitting your bank after PAYE tax, KiwiSaver (3-10%), ACC levies, and child support or student loans. Check your payslip or use the IRD's tax calculator. Include consistent side hustles like Uber or freelance gigs.

Example: Earning $70,000 gross yearly? Monthly net: ~$4,500 (varies by deductions).

Step 2: Track Your Spending for One Month

Before allocating, see where your money goes. Use free NZ apps like PocketSmith, MoneyHub, or the BNZ or ASB budgeting tools. Categorise everything: is that $15 vege box a need or the $20 Uber Eats a want?

Step 3: Allocate Percentages with NZ Examples

Apply the rule to a median single Kiwi earner ($4,500 monthly net):

| Category | % | Amount | NZ Examples |

|---|---|---|---|

| Needs (50%) | 50% | $2,250 | Rent ($1,800 Auckland 1-bed), groceries ($400), power ($200), bus pass ($100), insurance ($150) |

| Wants (30%) | 30% | $1,350 | Dining out ($300), Netflix/Sky ($50), gym ($80), weekend hikes/activities ($200), clothes ($100) |

| Savings/Debt (20%) | 20% | $900 | KiwiSaver ($200 auto), emergency fund ($300), credit card payoff ($200), house deposit ($200) |

For a household on $6,000 net: Needs $3,000, Wants $1,800, Savings $1,200. If Auckland rents push needs over 50%, switch to 60/20/20 and trim wants like subscriptions.

"The 50/30/20 budget is more of a goal than an absolute rule. Even 10% to savings brings big rewards."

Step 4: Automate and Review

Pay yourself first: Set auto-transfers to KiwiSaver, a high-interest savings account (like those from Kiwibank at 4-5% in 2026), or debt repayment. Review monthly—life changes, like a petrol price hike, mean tweaking.

NZ-Specific Tips for Budgeting Success

- Housing Crunch: Rents average $600/week in Auckland—cap at 30% of gross income. Explore flats on Trade Me or shared living to stay under 50% needs.

- Groceries: Shop at Pak'nSave or Countdown specials; aim for $120/person weekly. Use apps like Pricespy for deals.

- KiwiSaver Boost: Contribute extra in the 20% bucket—government matches up to $521/year. Check sorted.org.nz for projections.

- Debt Freedom: Prioritise high-interest credit cards (avg 20% APR) over student loans (12% max). WINZ can help if you're struggling.

- Emergency Fund: Build 3-6 months' expenses in a term deposit—vital with our earthquake risks and job market shifts.

If needs exceed 50%, negotiate bills (power via Powerswitch), downsize, or side hustle via Seek or Facebook Marketplace.

Common Adjustments for Different Kiwi Lifestyles

Solo in the Big Smoke

Auckland renter on $60k? Needs hit 55-60%. Cut wants: swap All Blacks tickets for free beaches.

Family in the Regions

Christchurch family on $90k household? Classic 50/30/20 fits better—more house for less.

Students or Low-Wage Workers

On $25/hour retail? Use 70/20/10, lean on StudyLink, and maximise wants sparingly like free uni events.

Start Budgeting Today: Your Next Steps

Grab your payslip, plug into MoneyHub's calculator, and map your first 50/30/20 budget tonight. Track for 30 days, then refine. Small wins like $900 monthly savings compound— in a year, that's over $10k towards freedom. You're not just budgeting; you're building a secure Kiwi future. Head to sorted.org.nz for free tools, and share your progress in the comments!

Frequently Asked Questions

Sources & References

-

1

50/30/20 Rule Explained: How It Works and Why It Matters - Gotrade — www.heygotrade.com

-

2

50/30/20 Budget Calculator - MoneyHub NZ — www.moneyhub.co.nz

-

3

The 50/30/20 Rule: A Smart Way to Budget, Save, and Spend — www.rbl.bank.in

-

4

The 50/30/20 Budget - PocketSmith — www.pocketsmith.com

-

5

The 2026 money glow-up: build habits that last - Interest.co.nz — www.interest.co.nz

- 6

-

7

10 Things to Do Differently with Money in 2026 - MoneyHub NZ — www.moneyhub.co.nz

Related Articles

The "No-Spend" Month: How One Kiwi Saved $2;000 in 30 Days

Imagine looking at your bank account at the end of the month and seeing an extra $2,000 staring back at you—all because you said "no" to impulse buys, takeaways, and those sneaky coffee runs. That's e...

How to Calculate Your Take-Home Pay with the NZ Salary Calculator

Ever wondered why your bank account doesn't match that shiny new job offer? You're not alone—many Kiwis scratch their heads over the gap between gross salary and actual take-home pay. With New Zealand...

How to Travel the World on a NZ Salary

Ever dreamed of sipping cocktails on a Thai beach or exploring the ancient ruins of Machu Picchu, all while earning a solid Kiwi wage? With New Zealand's average monthly salary hitting 5,666 NZD in 20...

The Hidden Costs of Credit Cards: How to Escape the NZ Debt Trap

Ever swiped your credit card for a quick coffee or online shop, only to watch the balance creep up month after month? You're not alone—many Kiwis are caught in a subtle debt trap fuelled by credit car...