How to Withdraw KiwiSaver for Your First Home (2026 Guide)

Imagine standing in front of your dream home in Auckland or Christchurch, keys in hand, knowing you've just used your KiwiSaver savings to make it yours. For many Kiwis, withdrawing KiwiSaver for your...

The Lifetimes NZ editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes NZ readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Imagine standing in front of your dream home in Auckland or Christchurch, keys in hand, knowing you've just used your KiwiSaver savings to make it yours. For many Kiwis, withdrawing KiwiSaver for your first home is the key to turning that dream into reality—especially with house prices climbing and deposits feeling out of reach. This 2026 guide breaks down everything you need to know, from eligibility to the full application process, so you can navigate it confidently.

Understanding KiwiSaver First Home Withdrawal

KiwiSaver isn't just for retirement—it's a powerful tool for first home buyers. The First Home Withdrawal lets you access your savings (minus a $1,000 minimum balance) to buy or build your first home in New Zealand. This includes your contributions, employer matches, government member tax credits, and investment growth, but not funds transferred from Australian complying superannuation schemes.

Since a 2015 amendment to the KiwiSaver Act 2006, you can even withdraw funds before your purchase agreement goes unconditional—like for a deposit paid to a stakeholder, such as the vendor's solicitor. This flexibility has helped thousands of Kiwis get over the deposit hump.

First Home Withdrawal vs First Home Grant: What's the Difference?

Don't confuse KiwiSaver First Home Withdrawal with Kāinga Ora's First Home Grant. The withdrawal uses your own KiwiSaver savings, while the grant is free government cash (up to $10,000 for an existing home or $15,000 for a new build in 2026, subject to income and deposit thresholds—check Kāinga Ora for latest rates).

| First Home Withdrawal | First Home Grant | |

|---|---|---|

| Source of Funds | Your KiwiSaver balance (less $1,000 min) | Government grant (no repayment) |

| KiwiSaver Membership | At least 3 years | Not required |

| Income Limits (2026) | None | Household income under $95,000 ($130,000 with kids) |

| Use | Deposit, purchase price, or building costs | Deposit on existing/new home |

| Repayment | No, but impacts retirement savings | Never |

You can combine both for maximum firepower—many Kiwis do. Always check with Kāinga Ora for grant eligibility via their website.

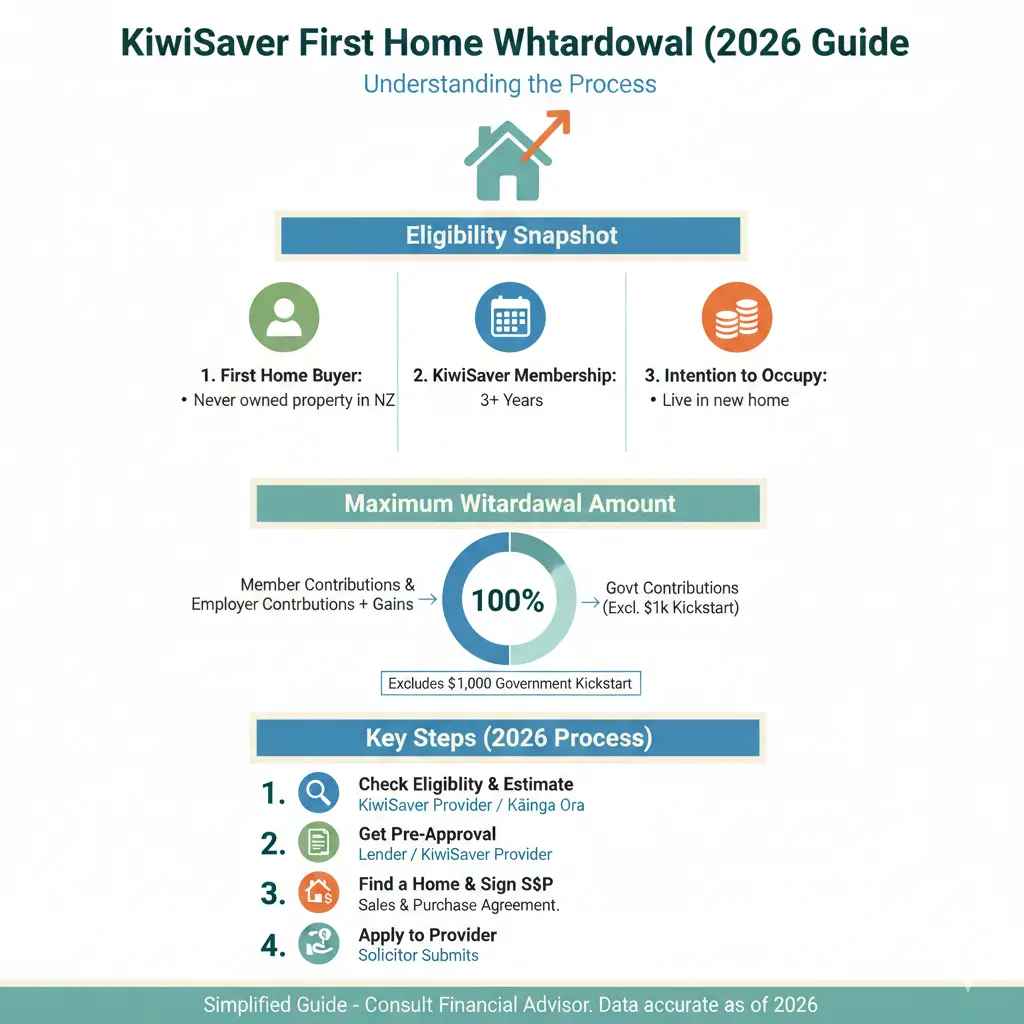

Eligibility Requirements for Withdrawing KiwiSaver for Your First Home

To qualify in 2026, you must tick these boxes:

- Be at least 18 years old.

- Have been a KiwiSaver member for a minimum of 3 years (from your first contribution).

- Not have owned a home anywhere in the world before (exceptions for certain family home transfers or if you sold due to hardship—check with your provider).

- Plan to live in the home as your primary residence within 12 months of purchase.

- Leave at least $1,000 in your KiwiSaver account.

- The property must be in New Zealand and valued under any applicable caps (align with Kāinga Ora limits if combining with grant).

Pro Tip: If you've dipped into KiwiSaver before (e.g., for hardship), you might still qualify, but confirm with your provider like AMP, BNZ, or Westpac.

How Much Can You Withdraw?

You can withdraw almost everything—your contributions, employer contributions, government tax credits (up to $521.43 per year you've claimed), growth, and fee subsidies—leaving just $1,000 behind. For example:

- If your balance is $50,000, you could withdraw up to $49,000.

- Average withdrawal in 2025 was around $40,000, per recent stats, helping cover 20-25% deposits on median homes.

But think long-term: Withdrawing reduces compound growth. A $40,000 withdrawal at age 25 could cost $200,000+ by 65 (assuming 5% annual returns). Use online calculators from your provider to model this.

Step-by-Step Application Process

Here's the complete 2026 process, tailored for Kiwis. Start early—processing takes 8-15 business days.

- Confirm Eligibility: Log into your KiwiSaver account or call your provider (e.g., AMP at 0800 267 5494). Get a balance statement.

- Find Your Home: Sign a sale and purchase agreement. Note if it's conditional (e.g., finance approval).

- Gather Documents:

- Completed withdrawal form from your provider.

- ID (passport/driver's licence).

- Sale and purchase agreement.

- Solicitor's contact details and undertaking (mandatory).

- Proof you've never owned property (statutory declaration).

- Get Solicitor's Undertaking: Your lawyer provides this to your provider. For conditional agreements, it confirms funds go to a stakeholder and are repaid if the deal falls through (not due to your default).

- Submit Application: Email or upload to your provider (e.g., [email protected]). Use myIR for income proof if needed.

- Approval and Payout: Funds go straight to your solicitor's trust account before settlement. Can't withdraw post-settlement.

- Settle and Move In: Use funds for deposit, balance, or building. Live there within 12 months.

Auckland Example: Buying a $900,000 unit? Withdraw $45,000 KiwiSaver + $10,000 grant for a 10% deposit with Westpac KiwiSaver.

Timeline: Plan Backwards from Settlement

- Auction win: Pay deposit from savings, withdraw KiwiSaver later for settlement (10% usually due immediately).

- Processing: 8-15 days—submit 3 weeks before needing funds.

- Conditional deals: Withdraw for deposit via stakeholder.

What If the Deal Falls Through?

No stress—funds return to your KiwiSaver account via your solicitor (unless you defaulted). Reapply for the next property.

Practical Tips for Kiwi First Home Buyers

Make it smoother:

- Combine Schemes: Pair with KiwiSaver + First Home Grant + Welcome Home Loan (up to 5% deposit).

- Choose Growth Funds: Higher risk early for bigger withdrawals—switch closer to withdrawal.

- Chat Providers: No withdrawal fees from most (AMP, Mercer), but confirm lawyer costs.

- Tax Free: Withdrawals are tax-free, but growth is taxed in KiwiSaver first.

- Regional Help: Check WINZ for extras if low-income; StudyLink if studying.

Disclaimer: This isn't personalised financial advice. Consult a licensed adviser, your provider, and lawyer. Rules can change—verify with IRD/Kāinga Ora.

Next Steps to Withdraw KiwiSaver for Your First Home

Ready? 1) Check your balance and eligibility today via your provider app. 2) Talk to a mortgage broker for pre-approval. 3) Engage a conveyancing solicitor experienced in KiwiSaver withdrawals. 4) Visit Kāinga Ora for grant combo. 5) House hunt with confidence—your KiwiSaver is waiting. Track progress with myIR and provider portals. Sweet homeownership awaits!

Frequently Asked Questions

Sources & References

-

1

KiwiSaver withdrawals for first home buyers - Tax Technical — www.taxtechnical.ird.govt.nz

-

2

Getting my KiwiSaver savings for my first home - Inland Revenue — www.ird.govt.nz

-

3

KiwiSaver and your first home | AMP New Zealand — www.amp.co.nz

-

4

KiwiSaver First Home Withdrawal | Mercer Financial Services NZ — www.mercerfinancialservices.co.nz

-

5

KiwiSaver for first home buyers - BNZ — www.bnz.co.nz

-

6

Using KiwiSaver for your first home | Westpac NZ — www.westpac.co.nz

-

7

KiwiSaver First Home Withdrawal Guide - MoneyHub NZ — www.moneyhub.co.nz

-

8

KiwiSaver first-home withdrawal - Kainga Ora — kaingaora.govt.nz

Related Articles

Working Multiple Jobs NZ: Tax and Legal Considerations

Juggling multiple jobs can boost your income, but it's crucial to understand the tax implications and legal requirements that come with working more than one role in Aotearoa. Whether you're a contrac...

Name Changes NZ: Legal Process and Costs

Considering a fresh start with a new name? Whether it's after marriage, divorce, or simply embracing a personal transformation, changing your name in New Zealand is straightforward but requires follow...

Holiday Home Tax Rules NZ: Private Use and Rental

Own a bach in Coromandel or a holiday home in Queenstown? You're not alone—many Kiwis cherish these escapes, but renting them out while enjoying personal use can trip you up on tax rules. Getting the...

Industry Bodies and Professional Associations NZ

Whether you're launching a business, advancing your career, or navigating financial regulations, industry bodies and professional associations in New Zealand offer invaluable support. These organisati...