Mortgage Refixing Guide: How to Negotiate the Best Rate with Your Bank

Imagine slashing hundreds of dollars off your weekly mortgage payments just by knowing when and how to refix. With interest rates easing in 2026, thousands of Kiwis are facing refix decisions that cou...

Sarah covers personal finance, tax, and KiwiSaver topics for Lifetimes NZ. She focuses on making money management straightforward and practical for everyday Kiwis.

Imagine slashing hundreds of dollars off your weekly mortgage payments just by knowing when and how to refix. With interest rates easing in 2026, thousands of Kiwis are facing refix decisions that could save them thousands over the coming years—don't let yours slip by on autopilot.

Refixing your mortgage isn't just a routine bank notice; it's your golden opportunity to negotiate better terms, lower your rate, and accelerate paying off your home. In this guide, we'll walk you through everything you need to know about mortgage refixing in New Zealand, from timing your move to arming yourself with negotiation tactics that banks can't ignore. Whether you're with ANZ, ASB, BNZ, Kiwibank, or Westpac, these strategies apply nationwide.

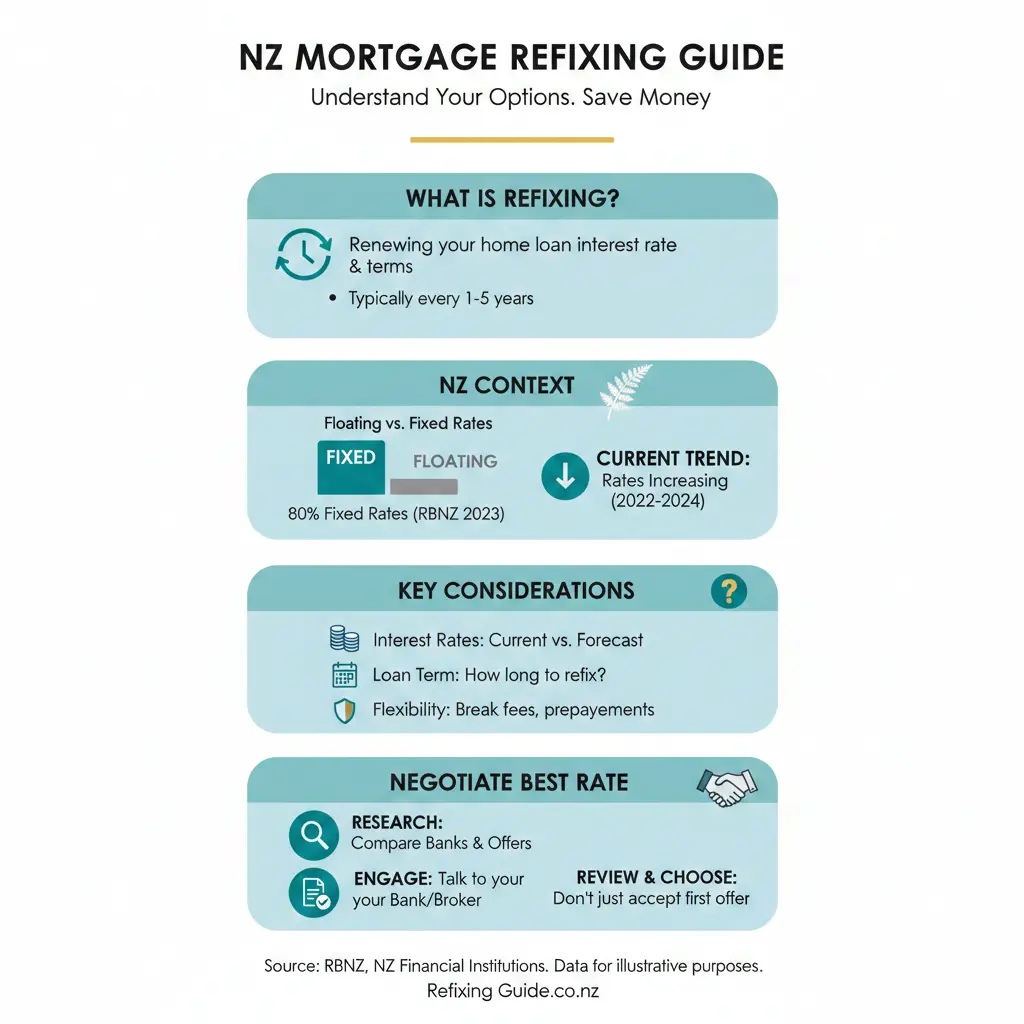

Understanding Mortgage Refixing in New Zealand

When your fixed-rate term ends—typically after 6 months, 1 year, 2 years, or longer—your mortgage doesn't vanish. It rolls onto a default rate, often floating or short-term fixed, which could be higher than what you had. Refixing means choosing a new fixed term and rate before that happens, locking in certainty for your budget.

In 2026, with the Official Cash Rate (OCR) stabilising after cuts, mortgage rates have dropped from 2023 peaks around 7.5%. For instance, a $500,000 loan over 30 years at 7.5% costs $807 weekly, but refixing at 4.59% drops it to $585—a whopping $222 less per week or $11,544 annually. That's real money back in your pocket for KiwiSaver contributions, family holidays, or renovations.

Fixed vs Floating vs Split Terms: What's Best for You?

- Fixed rates offer payment predictability, ideal if rates might rise. Short-term (1-2 years) fixes are popular in 2026 as experts predict gradual drops.

- Floating rates give flexibility for extra repayments but expose you to hikes. They're softening early 2026 but could edge up later.

- Split terms (e.g., half 1-year fixed, half floating) balance risk—perfect if part of your loan matures soon and you want to wait for better deals.

Review your loan structure annually. Life changes—like a new job, kids' school fees, or home equity growth—mean your ideal mix evolves.

Timing Your Refix: Capitalise on 2026 Rate Trends

2026 brings relief for most mortgage holders as fixed terms from high-rate periods mature. Short-term rates have eased, with floating expected to soften further early in the year, though longer terms might stabilise or tick up by mid-year.

Key Rate Predictions for 2026

Experts forecast no return to 2-3% rates, but slight drops through 2025 into 2026. Watch for inflation data from Stats NZ or global events like tariffs that could reverse trends. If your loan's from a low 2.99% five-year fix, brace for pain—many are rolling off now.

| Fix Term | Expected 2026 Trend | Best For |

|---|---|---|

| 6 months | 0.27% higher than 1-year currently; needs big drop to beat it | Aggressive rate chasers |

| 1-2 years | Most attractive for anticipated drops | Balanced homeowners |

| 3+ years | Stable but less competitive short-term | Budget certainty seekers |

Pro tip: If half your loan refixes soon and the rest later, fix the maturing portion short-term to align maturities for a full refinance.

How to Negotiate the Best Refix Rate with Your Bank

Banks compete fiercely in 2026 with cash-back offers and specials. Don't accept the first quote—negotiate like a pro.

Step-by-Step Negotiation Tactics

- Get quotes from competitors: Use a mortgage broker for free market comparisons. Mention rival offers—banks often match or beat them.

- Leverage your equity: If your home's value has risen (check via QV or CoreLogic), demand removal of low-equity margins (extra 0.5-1% for deposits under 20%). High equity means lower risk, so push for unadvertised specials.

- Ask for cash back: Switching can net $3,000-$5,000, covering legal fees ($1,500-$2,000).

- Time it right: Approach 4-6 weeks before expiry to avoid clawback periods (where switching too early costs break fees).

- Bundle services: Offer to park savings, KiwiSaver, or insurance with them for rate discounts.

"Using a mortgage adviser helps people find the most suitable loan and rate – and manage the application process with the lender."

Brokers are free (paid by banks) and access wholesale rates. Find one via the NZ Mortgage Brokers Association.

Common Bank Pitfalls to Avoid

- Auto-refixing to floating without shopping around.

- Ignoring full applications for refinances—prepare paperwork early.

- Missing equity reassessments post-property booms, like Canterbury's 2026 uptick.

Boost Your Refix with Smart Repayment Strategies

Refixing is prime time to supercharge repayments. Increase by 5% annually (matching wage growth) to shave ~14 years off a 30-year loan.

Actionable Repayment Hacks

- Bump payments at refix: Banks allow choices without penalty; do it every maturity.

- Extra repayments: Up to 20% yearly on most loans, fee-free. One-off lumps before refixing hit principal hard.

- Keep old payments post-rate drop: Overpays principal, shortening the loan.

- Offset accounts: Park savings to reduce interest—great for variable incomes.

Adjust for 2026 realities: If pay rises or expenses drop, ramp up; if tough, ensure sustainability.

Refixing vs Refinancing: Know the Difference

Refixing stays with your bank on new terms. Refinancing switches lenders for better rates or features, but involves full credit checks and fees. Ideal if out of clawback and rates align across your loans.

Next Steps: Take Control of Your Mortgage Today

Grab your latest statement, check your refix date, and contact a broker or your bank. Run numbers with online calculators from Canstar or Interest.co.nz, then negotiate armed with market intel. Small actions now mean a debt-free future sooner—your whānau will thank you. Review annually, especially with 2026's shifting rates, and celebrate the savings.

Frequently Asked Questions

Sources & References

-

1

The ultimate guide to refixing & refinancing | Squirrel — www.squirrel.co.nz

- 2

-

3

The good news for mortgage holders - NZ Herald — www.nzherald.co.nz

-

4

Interest Rate Predictions 2026 & 2027 - MoneyHub NZ — www.moneyhub.co.nz

-

5

Fixed vs Floating: Your Mortgage Strategy for 2025-2026 — www.velocityfinancial.co.nz

-

6

Planning your 2026 mortgage strategy - Threefold — threefold.co.nz

-

7

2026 Mortgage Rate Outlook: Scenarios, No Certainties! - New Zealand Mortgages — www.newzealandmortgages.co.nz

-

8

Refixing in 2026: A Decision Framework - New Zealand Mortgages — www.newzealandmortgages.co.nz

- 9

Related Articles

Using the NZ Mortgage Calculator to Plan Your House Hunt

Imagine spotting your dream home in Auckland or Christchurch, but wondering if you can actually afford it. That's where the NZ Mortgage Calculator comes in—your essential tool for turning house-huntin...

Mortgage Refinancing: When Does It Make Sense?

Imagine shaving thousands off your mortgage interest while unlocking cash for that home reno or debt consolidation you've been dreaming about. For Kiwis with home loans, mortgage refinancing can be a...

How to Pay Off Your Mortgage Faster (NZ Strategies)

Imagine owning your home outright years earlier than planned, freeing up thousands in interest payments and giving you financial freedom sooner. For Kiwis with mortgages, paying off your home loan fas...

Mortgage Break Fees NZ: How Much Will It Cost to Switch?

Ever stared at your mortgage statement, dreaming of switching to a lower rate but frozen by the dreaded words "break fee"? You're not alone—thousands of Kiwis face this dilemma every year as interest...