Using the NZ Mortgage Calculator to Plan Your House Hunt

Imagine spotting your dream home in Auckland or Christchurch, but wondering if you can actually afford it. That's where the NZ Mortgage Calculator comes in—your essential tool for turning house-huntin...

Sarah covers personal finance, tax, and KiwiSaver topics for Lifetimes NZ. She focuses on making money management straightforward and practical for everyday Kiwis.

Imagine spotting your dream home in Auckland or Christchurch, but wondering if you can actually afford it. That's where the NZ Mortgage Calculator comes in—your essential tool for turning house-hunting dreams into a solid plan. Whether you're a first-home buyer dipping into KiwiSaver or upsizing for the family, these calculators help you crunch the numbers with New Zealand-specific rates and terms.

With house prices stabilising in 2026 and interest rates hovering around 6-7%, planning ahead is crucial. This guide walks you through using the NZ Mortgage Calculator to plan your house hunt, from picking the right tool to interpreting results and avoiding common pitfalls. You'll get practical tips tailored for Kiwis, complete with real-world examples.

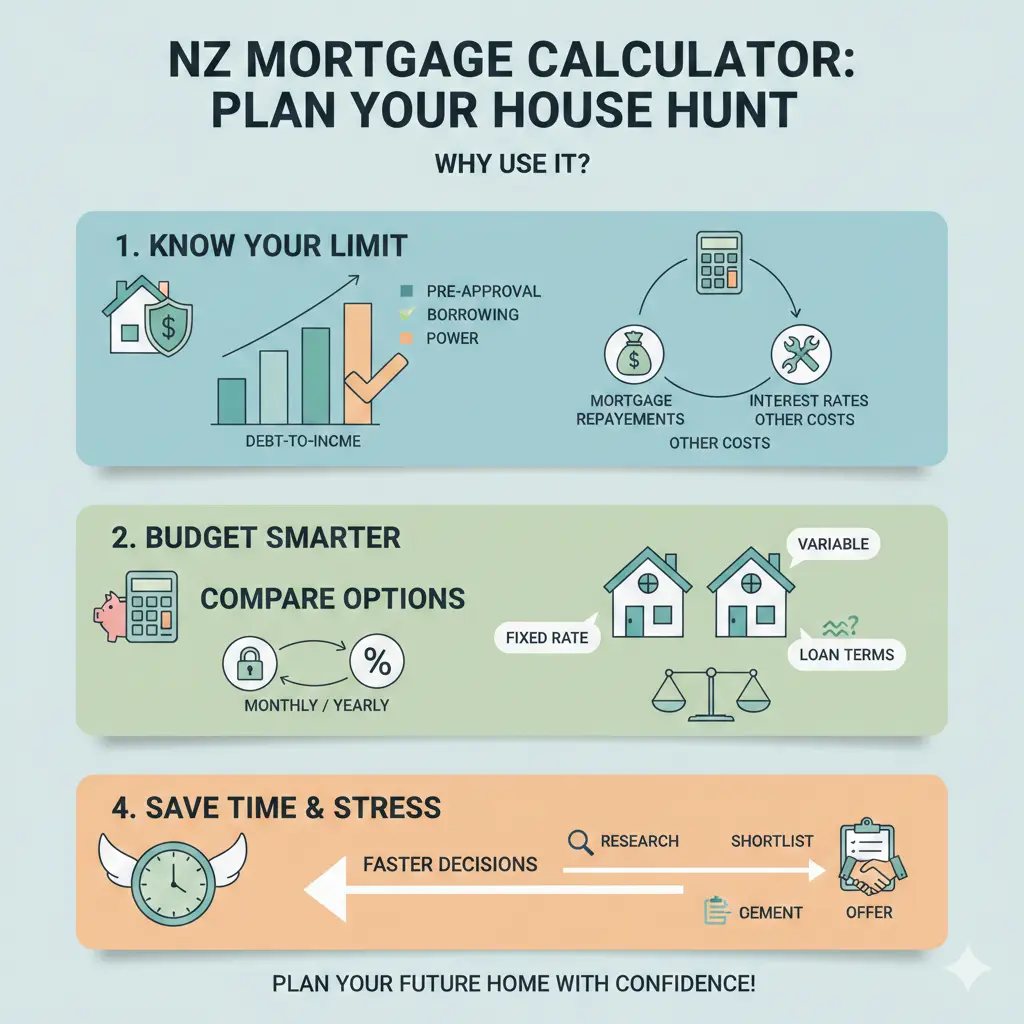

Why Use an NZ Mortgage Calculator for Your House Hunt?

House hunting without a budget is like driving without a map—you might end up lost or broke. An NZ mortgage calculator gives you a clear picture of what you can borrow, your fortnightly or monthly repayments, and the total interest over time. It's especially handy in New Zealand, where lenders like Kiwibank, BNZ, and Westpac offer tools based on local rules such as loan-to-value ratios (LVR) and 20% equity requirements.

These calculators factor in Kiwi realities: variable rates that can shift, KiwiSaver withdrawals for first-home buyers, and options for principal-and-interest or interest-only loans. By inputting your income, deposit, and expenses, you'll see if that $800,000 home in Wellington fits your budget before you fall in love with it.

Key Benefits for Kiwi Home Buyers

- Affordability check: Estimate repayments without committing—vital with average first-home buyer mortgages around $567,782.

- Scenario testing: Compare 30-year vs 20-year terms or 6% vs 7% rates to find the best fit.

- Stress-test your budget: See how rate rises affect payments, helping you prepare for Reserve Bank changes.

- KiwiSaver integration: Many tools let you factor in withdrawals, bringing the ladder closer.

How NZ Mortgage Calculators Work

Most NZ mortgage calculators are straightforward: enter loan amount, interest rate, term, and repayment frequency (weekly, fortnightly, or monthly). They calculate principal-and-interest repayments assuming fixed rates and on-time payments—though real life includes rate floats and extras like low-equity fees.

For example, MoneyHub's calculator breaks down principal vs interest over time, showing your monthly total. Sorted's version even models split loans or extra repayments to shave years off your term.

Essential Inputs You'll Need

- Loan amount: Purchase price minus deposit (aim for 20% to dodge LVR restrictions).

- Interest rate: Check current rates—around 6-7% for floating in 2026.

- Loan term: Typically 20-30 years; shorter means higher payments but less interest.

- Repayment frequency: Fortnightly is popular in NZ as it aligns with pay cycles and reduces interest.

- Start date: For precise interest calculations.

Pro tip: Use multiple calculators from banks like ANZ or ASB for a balanced view, as each assumes slightly different scenarios.

Top NZ Mortgage Calculators to Try in 2026

New Zealand has a wealth of free tools from trusted sources. Here's a roundup of the best for house hunters:

| Calculator | Key Features | Best For |

|---|---|---|

| MoneyHub Repayment Calculator | Principal/interest split, video guide, fixed repayment assumptions | Detailed breakdowns |

| Kiwibank Repayments Calculator | Compares structures, equity-based rates (20% min) | Structuring options |

| BNZ Home Loan Calculator | Payoff time estimates, low-equity warnings | First-home buyers |

| Sorted Mortgage Calculator | Extra repayments, KiwiSaver focus, interest-only toggle | Govt-backed budgeting |

| Westpac Repayment Calculator | Simple inputs, low-equity margin info | Quick checks |

Start with Sorted for its neutral, Sorted.org.nz backing—perfect for unbiased planning.

Real-World Examples: Crunching Numbers for Kiwi Homes

Let's apply these to 2026 scenarios. Assume a $800,000 home in Hamilton with a 20% ($160,000) deposit, leaving a $640,000 loan.

Example 1: Standard 30-Year P&I at 6%

Monthly repayments: around $3,830; fortnightly: $1,766. Total interest: over $900,000. At 7%, jumps to $4,260 monthly—showing why shopping rates matters.

Example 2: First-Home Buyer with KiwiSaver

A couple earning $120,000 combined withdraws $100,000 KiwiSaver for deposit on a $600,000 Auckland unit ($480,000 loan). Sorted's tool shows fortnightly payments of $1,400 at 6.5%, payable in 25 years with extras.

Example 3: Stress Testing for Rate Rises

BNZ's calculator reveals a 2% rise adds $500+ fortnightly—use this to build a buffer.

"Increasing your repayments saves you heaps on interest and time!"

Practical Tips for Using Calculators in Your House Hunt

- Factor in all costs: Add rates, insurance, and maintenance (1-2% of home value yearly).

- Test low-equity scenarios: Under 20%? Expect LVR speed bumps and higher rates.

- Incorporate income/deposit: Tools like LifeDirect's show borrowing power based on earnings.

- Plan for extras: Offset accounts or top-ups can cut interest.

- Consult pros: Calculators guide; advisers (via sorted.org.nz) personalise with credit checks.

Track median prices via realestate.co.nz and pair with IRD's income data for realistic inputs.

Common Mistakes to Avoid

Don't just plug in dream numbers—be conservative. Assumptions like fixed rates rarely hold; test hikes. Ignore fees at your peril: establishment up to $150, plus potential low-equity premiums. And remember, these aren't pre-approvals—lenders assess debt-to-income too.

Next Steps: From Calculator to Keys

Grab your payslips, KiwiSaver balance, and hit up a calculator today. Shortlist homes within your range, then book a free adviser chat via sorted.org.nz or your bank. Get pre-approval from lenders like ANZ for serious hunting. With smart planning, your house hunt becomes a house win—happy searching, Kiwis!

Frequently Asked Questions

Sources & References

-

1

MoneyHub Mortgage Repayment Calculator — www.moneyhub.co.nz

-

2

Simon Conn Mortgage Calculator New Zealand — www.simonconn.com

-

3

Mortgages.co.nz Mortgage Repayments Calculator — mortgages.co.nz

-

4

Kiwibank Repayments & Structuring Calculator — www.kiwibank.co.nz

-

5

BNZ Home Loan Repayment Calculator — www.bnz.co.nz

-

6

Westpac Mortgage Repayment Calculator — www.westpac.co.nz

-

7

Sorted Mortgage Calculator — sorted.org.nz

-

8

ASB Mortgage Repayment Calculator — www.asb.co.nz

-

9

ANZ Home Loan Repayment Calculator — tools.anz.co.nz

Useful Tools

Related Articles

Mortgage Refixing Guide: How to Negotiate the Best Rate with Your Bank

Imagine slashing hundreds of dollars off your weekly mortgage payments just by knowing when and how to refix. With interest rates easing in 2026, thousands of Kiwis are facing refix decisions that cou...

Mortgage Refinancing: When Does It Make Sense?

Imagine shaving thousands off your mortgage interest while unlocking cash for that home reno or debt consolidation you've been dreaming about. For Kiwis with home loans, mortgage refinancing can be a...

How to Pay Off Your Mortgage Faster (NZ Strategies)

Imagine owning your home outright years earlier than planned, freeing up thousands in interest payments and giving you financial freedom sooner. For Kiwis with mortgages, paying off your home loan fas...

Mortgage Break Fees NZ: How Much Will It Cost to Switch?

Ever stared at your mortgage statement, dreaming of switching to a lower rate but frozen by the dreaded words "break fee"? You're not alone—thousands of Kiwis face this dilemma every year as interest...