How to Pay Off Your Mortgage Faster (NZ Strategies)

Imagine owning your home outright years earlier than planned, freeing up thousands in interest payments and giving you financial freedom sooner. For Kiwis with mortgages, paying off your home loan fas...

Sarah covers personal finance, tax, and KiwiSaver topics for Lifetimes NZ. She focuses on making money management straightforward and practical for everyday Kiwis.

Imagine owning your home outright years earlier than planned, freeing up thousands in interest payments and giving you financial freedom sooner. For Kiwis with mortgages, paying off your home loan faster isn't just a dream—it's achievable with smart, practical strategies tailored to New Zealand's 2026 market.

In today's environment, with interest rates stabilising and many fixed terms rolling over, 2026 is an ideal time to accelerate your mortgage payoff. Whether you're dealing with a $700,000 loan or more, small changes like extra repayments can save over $87,000 in interest and cut 3.5 years off your term. We'll walk you through proven NZ-specific tactics, from optimising your structure to leveraging equity, so you can take control today.

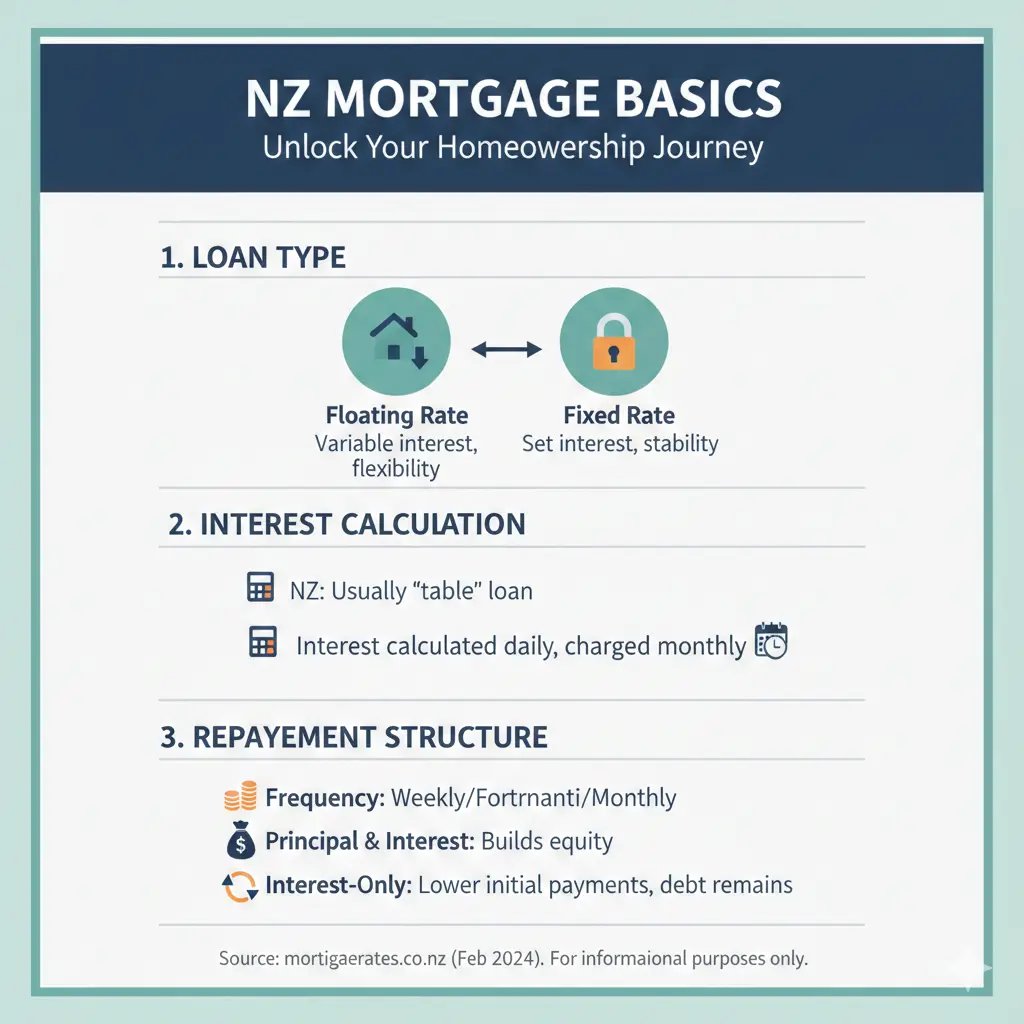

Understand Your Mortgage Basics in NZ

Before diving into strategies, know your setup. Most Kiwi home loans are either fixed (locked rate for 6 months to 5 years) or floating (variable rate with flexibility). Many have a mix, plus features like offset accounts or redraw facilities. Banks like BNZ offer tools to review these.

Check your loan-to-value ratio (LVR)—it's key for refinancing. In 2026, owner-occupiers can borrow up to 80% LVR more easily (25% of loans), while investors get 70% LVR for 10% of loans. Use the Reserve Bank's Loan-to-Value Restrictions page for details: rbnz.govt.nz.

Why Pay Off Faster? The Numbers Add Up

Extra payments reduce principal, slashing interest over time. On a $700,000 mortgage at 5%, adding $50 weekly saves $87,000 and 3.5 years. With OCR easing into 2026, floating rates may drop further, amplifying these gains.

Strategy 1: Optimise Your Mortgage Structure

Don't just refix blindly—review your entire setup. 2026 sees many 2023-2025 fixed loans expiring at higher rates (e.g., rolling off 2.99% specials is tough, but most get relief). A blended structure—part fixed, part floating—offers protection and flexibility.

Fixed vs Floating: What's Best for 2026?

- Fix short-term (6-12 months): Common choice, but 6-month rates are 0.27% higher than 1-year (4.99% vs lower). Fix 1-year unless expecting big drops.

- Float for flexibility: Pay extras anytime, grab rate cuts early. Ideal if bonuses or windfalls are coming.

- Split your loan: 50% fixed 1-year, 50% floating. Adapts to rate forecasts—experts predict slight drops but no return to 2-3%.

Action step: Contact your bank or broker 3-6 months before expiry. Tools like Canstar's comparison site help: canstar.co.nz.

Refinance or Restructure

Shop around—banks compete fiercely. If property values rise in 2026, unlock equity for extras without new borrowing. Consolidate high-interest debt (credit cards at 20%+) into your mortgage at ~5%. Watch CCCFA rules: lenders must ensure affordability.

Strategy 2: Boost Your Repayments

The simplest win: pay more principal. Even small increases compound hugely.

Make Regular Extra Payments

Increase by $50/week on that $700k loan? Massive savings. Keep repayments steady when rates drop—extra goes to principal. Most fixed loans allow one annual lump sum (e.g., $10,000) fee-free.

| Loan Amount | Extra Weekly | Interest Saved | Time Shaved |

|---|---|---|---|

| $500,000 @5% | $50 | $62,000 | 3 years |

| $700,000 @5% | $50 | $87,000 | 3.5 years |

| $1,000,000 @5% | $50 | $124,000 | 3.5 years |

Estimates based on standard calculators; use your bank's tool for precision.

Use Windfalls Wisely

Tax refunds, KiwiSaver withdrawals (first home), or bonuses? Lump sum them in. Pay rises? Uplift repayments immediately. Floating portions make this easy—no penalties.

Strategy 3: Leverage KiwiSaver and Government Perks

KiwiSaver isn't just retirement—first-home buyers can withdraw for deposits, building equity faster. For existing owners, boost contributions for compound growth, indirectly aiding mortgage payoff via savings.

Check StudyLink or WINZ for family support if eligible, freeing cash for extras. IRD's mortgage interest deduction changes phased out by 2026 for investors, but owner-occupiers focus on principal reduction.

Strategy 4: Budget and Lifestyle Hacks

Trim expenses to fund extras. Track with apps like PocketSmith (NZ-based). Common wins:

- Switch energy providers—save $200/year via powerswitch.org.nz.

- Meal prep—cut grocery bills 20%.

- Review insurance—bundle for discounts via sortedsmart.org.nz.

- Side hustle: Drive for Uber or freelance on SEEK—extra $200/month pays off fast.

Reassess annually: pay rise? Increase repayments 10%.

Strategy 5: Advanced Tactics for 2026

Offset Accounts and Redraw

Park savings in an offset account—reduces interest-calculating balance. E.g., $20k savings on $500k loan saves as if paying $20k principal. Popular with ANZ, ASB.

Equity Release for Investments

With rising values, top-up for renovations boosting value (e.g., insulation qualifies for Warmer Kiwi Homes grant). But avoid over-borrowing—stick to LVR limits.

Watch Macro Trends

International risks like tariffs could nudge rates up—hedge with splits. RBNZ's site tracks OCR: rbnz.govt.nz.

Potential Pitfalls to Avoid

- Early repayment fees on fixed loans (beyond the one lump sum).

- Overcommitting—ensure 3-6 months emergency fund.

- Ignoring fees: Compare total costs, not just rates.

- Forgetting advice: Free brokers via mortgageadvisers.org.nz.

Next Steps to Pay Off Your Mortgage Faster

Start today: Log into internet banking, note your expiry date, and calculate extras with a tool like BNZ's calculator. Book a free chat with a mortgage adviser, review your budget, and commit to one extra payment this month. Track progress quarterly— you'll be mortgage-free sooner, with more for family, travel, or retirement. In 2026, these moves position you strongest.

Frequently Asked Questions

Sources & References

-

1

Top tips for building wealth through property in 2026 - Moneybox — moneybox.co.nz

-

2

Planning your 2026 mortgage strategy - Threefold — threefold.co.nz

-

3

Fixed vs Floating: Your Mortgage Strategy for 2025-2026 — www.velocityfinancial.co.nz

-

4

Why 2026 Could Be the Best Year to Restructure Your Mortgage — www.taxprofessionals.co.nz

-

5

End-of-Year Mortgage & Money Check-Up: 7 Smart Moves — www.eurekafinancial.co.nz

-

6

Refixing in 2026: A Decision Framework — www.newzealandmortgages.co.nz

-

7

Six ways to pay off your home loan faster - BNZ — www.bnz.co.nz

Related Articles

Using the NZ Mortgage Calculator to Plan Your House Hunt

Imagine spotting your dream home in Auckland or Christchurch, but wondering if you can actually afford it. That's where the NZ Mortgage Calculator comes in—your essential tool for turning house-huntin...

Mortgage Refixing Guide: How to Negotiate the Best Rate with Your Bank

Imagine slashing hundreds of dollars off your weekly mortgage payments just by knowing when and how to refix. With interest rates easing in 2026, thousands of Kiwis are facing refix decisions that cou...

Mortgage Refinancing: When Does It Make Sense?

Imagine shaving thousands off your mortgage interest while unlocking cash for that home reno or debt consolidation you've been dreaming about. For Kiwis with home loans, mortgage refinancing can be a...

Mortgage Break Fees NZ: How Much Will It Cost to Switch?

Ever stared at your mortgage statement, dreaming of switching to a lower rate but frozen by the dreaded words "break fee"? You're not alone—thousands of Kiwis face this dilemma every year as interest...